Marketplaces have become a relatively simple channel to start an online business. Special no-code apps and payment gateways enable merchants to almost effortlessly set up a fully working system for consumers from all around the world. The issue is that with this sort of level of convenience, there are consequences, especially if you’re not properly dealing with the risk of fraud. Marketplaces need to ensure that payments are secure, buyers’ info is protected, and there are no fraudulent transactions or fraudulent merchants.

For that, merchant fraud prevention measures and proper risk assessment tools are required. Otherwise, you open a door for criminals to exploit, putting your business at risk. So, what exactly is merchant fraud, and how can you deal with it? We dive into this topic below.

What is Merchant Fraud?

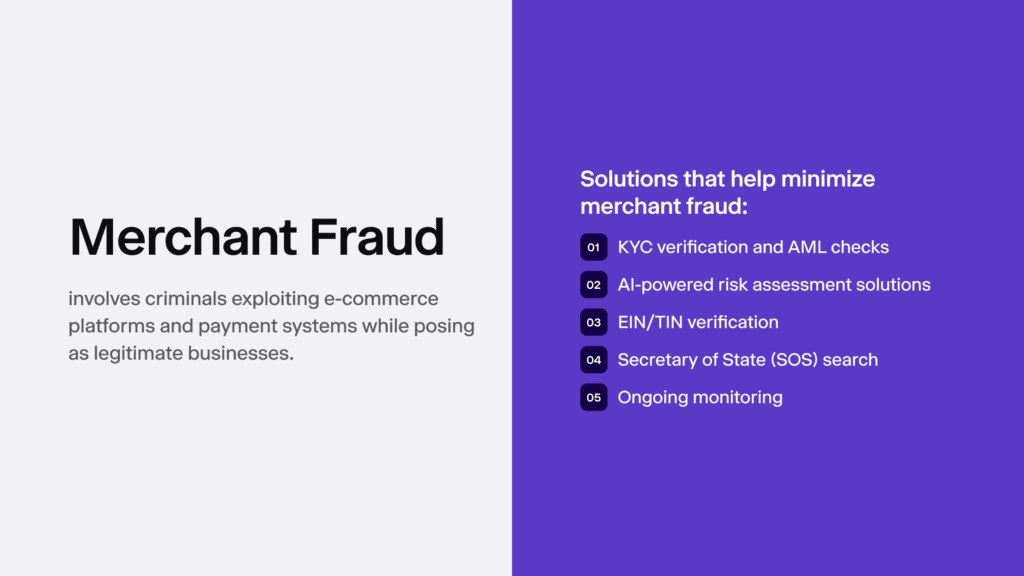

Merchant fraud is a fraudulent process that occurs when a person or a company poses as a legitimate business to generate illegal profits. Merchant fraud deceives everyone involved: consumers, other businesses, and payment systems.

Some scenarios of merchant fraud include:

- Merchants who misrepresent their services and charge customers for non-existent subscriptions.

- Fake sellers who accept payments for products or services they are not planning on delivering.

This form of fraud happens alongside other criminal activities, such as identity fraud or bust-out fraud, and is designed to steal from unsuspecting parties.

How Does Merchant Fraud Work?

To make merchant fraud look believable, criminals can work in groups, creating fake business websites, illicit payment processing, and take it even further, for example, by processing stolen card information or using synthetic identities for fake sales. So, in other words, criminals do everything in their power to make the store look authentic.

After the buyer is tricked and buys the item, criminals can:

- Deliver low-quality items or replicas

- Ghost the buyer and do not send anything

- Use the customer’s credit card information to make new, unauthorized charges

They can create fake social media accounts and put up lower prices than usual to lure their victims. Fraudsters can also conduct merchant fraud by uploading fake listings of rare, hard-to-find items that are in high demand by collectors. Due to AI and ChatGPT, creating realistic listing photos that appear genuine is much easier. Some criminals can actually deliver items, but they can be poorly made, with unsafe materials from unregulated countries.

Negative Effects Linked to Merchant Fraud for Businesses

While merchant fraud is obviously an unwanted guest for a business, it’s important to know the exact risks it comes with.

Without effective fraud prevention, businesses risk:

- Financial losses. Merchants can lose money due to direct theft, chargebacks, and other penalties associated with fraudulent transactions.

- Reputational damage. Merchants can harm their relationship with the customers, affecting their trust in the brand and making future plans for scaling less achievable.

- Legal risks. Non-compliance fines for not sticking to Anti-Money Laundering (AML) or Know Your Business (KYB) laws, especially for regulated merchants that operate in industries like online pharmacies, can result in non-compliance fines.

- Operational disruption. If certain thresholds are reached, payment providers can freeze or even terminate accounts that have very high fraud rates.

- Higher costs. If you receive many high-risk orders or you have a high chargeback rate, payment processors can raise fees for their services.

Related: Merchant Onboarding: Steps, Required Documents & More

How Does Merchant Fraud Differ From Buyer Fraud?

The main difference between the two is related to the individual who is conducting the fraudulent act. Buyer fraud involves someone using deceptive practices when purchasing from a merchant (a business) and scamming the business or individual merchant.

In the meantime, merchant fraud involves someone illegitimately selling goods or services, often linked either to fraudsters posing as legitimate merchants or legitimate merchants acting illegally. In other words, it’s someone posing as a merchant to gain funds illegally.

Who Covers Losses From Merchant Fraud?

The issuing bank covers the fraud losses linked to merchant fraud, but only with one condition: the merchant needs to meet security requirements. Otherwise, this could result in a chargeback, which, in this case, merchants can try to reduce the losses via chargeback insurance. However, banks often charge a fee for every chargeback, which increases costs.

In similar cases, like card-not-present fraud, merchants remain liable for the transaction value and the lost revenue unless they have specific tools or protections with offered guarantees. If a merchant processes too many fraudulent transactions, the bank can raise card processing fees. In even more serious cases, the bank can shut down the merchant’s account or freeze it for a certain period.

The Main Types of Merchant Fraud

Since criminals can abuse the system using all sorts of fraudulent practices, there are different types of merchant fraud.

Here are the most common ones:

1. Merchant Identity Theft

Also known as business identity theft, it happens when criminals use fake storefronts and don’t deliver any actual products or legitimate services, but still accept payments that generate illegitimate revenue.

Merchant identity theft’s goal is to impersonate a legitimate, existing business. Sometimes, criminals steal sensitive information, such as an entity’s or its owners’ bank account information or EIN, and fraudulently gain credit or even get loans for a fake business. Customers’ accounts can also be drained in this sort of scam.

2. Merchant Identity Swap

Merchant identity swap is a form of fraud where bad actors open a merchant account using fake or stolen identities. This is done to avoid getting caught via real credentials and as a way to bypass KYC/AML and KYB compliance checks and standard marketplace security requirements.

Once that’s out of the way, criminals can process illicit transactions, launder money, and exploit credit. Often, criminals are experienced and know how due diligence is done. For this reason, it’s extremely important to carefully examine businesses and future partners before starting a business relationship with them. For that, KYB checks and automated onboarding processes are used.

3. Bust-Out Fraud

A bust-out scam happens when a bad actor creates a seemingly legitimate business facade, sometimes using real or fake/synthetic business information to build credit and trust with the payment processor. This takes normal business activity, but the twist is that criminals suddenly max out the credit lines or take too many orders without actually sending out items, then completely disappear. Afterwards, financial companies are left to deal with losses linked to unfulfilled orders and their chargebacks.

Sometimes, fraudsters lure investors and their money to build the business and take out as much credit as possible. This is a calculated fraud scheme that takes time, often being difficult to detect. As a result, monitoring is vital, not just standard checks at the initial onboarding stage, as a way to detect AML red flags or inconsistencies during credit checks.

4. Transaction Laundering

Transaction laundering is a type of merchant fraud that criminals use to have an approved merchant account that they use as a money laundering channel or for processing payments like drug money. It can be a small online shop that hides dirty money.

Sometimes, fake merchant accounts are used, but sometimes criminals partner with genuine businesses that already built a trusted payment ecosystem, giving them a cut of their profits. They use such accounts to route transactions and bypass fraud prevention controls that would instantly detect suspicious behavior if they used their own, real identities.

Related: The 3 Stages of Money Laundering [Simple Explanation]

5. Business Model Swap

A business model swap is a form of fraud where criminals set up a low-risk merchant account, such as a small kiosk selling candy and newspapers, get approved, then quickly change the whole model into a high-risk business or a model that goes against all policies, like selling counterfeit items. Such business format changes are also done to evade detection, and, depending on the business model, can be straight-up illegal or simply unethical due to hidden original intentions.

How to Detect Merchant Fraud?

There are a few fraud prevention measures that can’t be missed or taken lightly, especially since some merchant fraud forms evolve and can be hard to detect at first.

For example, you should:

Conduct a Risk Assessment

The exact steps depend on the services and products you sell. However, a risk assessment is a process that all parties use, including payment processors, banks and merchants. This helps identify the exact dangers linked to your business, determining if a certain potential risk is worth bringing into consideration. Risk assessments are designed to prioritize risks and the likelihood of threats that need to be assessed and managed on a regular basis. So, if there’s a warning sign, a risk assessment points it out and helps avoid onboarding risky B2B clients.

Related: A Guide to Risk Scoring in 2026

Check Standard Business Details

Even if you’re not a regulated entity, verifying basic information, such as a company’s name and address from an official government registry and simple online means, is vital. If there are slight mismatches, such as Google Images showing not an office building, but a strange house that doesn’t match the business’s description, there’s a risk of a false business.

This can be a good start for your due diligence processes, helping check if the entity provided proper information, like its formation state. All licensed businesses need to be properly registered. Automated solutions, like iDenfy’s KYB service, have built-in tools, like business address verification and other options for certain markets, like the Secretary of State (SOS) search, which help determine if the business is legitimate without having to manually type and look up different databases. It extracts all information about a business with AI tips and suggestions for further assessment.

Related: How to Do a Business Registration Lookup [Guide]

Conduct an EIN/TIN Verification

EIN, or Employer Identification Number, is a form of Tax Identification Number (TIN) issued by the IRS in the US specifically for businesses. EINs are required for basic business activities, such as opening a bank account or managing investments. If a potential partner lacks a valid EIN, it can be viewed as a significant risk across these areas.

EIN verification confirms that a business is registered with US tax authorities and uses a valid EIN. This check helps ensure the EIN is real and not fraudulent, similar to verifying a business’s good standing. If a business doesn’t have an EIN, or the details fail to match verification results, you should look into this case more carefully.

Monitor Transactions

For transaction monitoring, a software or an automated system is required as a way to compare current transaction data against a customer’s historical behavior. Since fraudsters know how to avoid reporting thresholds and blend into “typical” behavior, monitoring helps better inspect suspicious transactions, like sudden purchases of high-value items, large amounts of payments within a short time period, transactions from high-risk countries, etc. This sort of transaction often needs to be assessed before shining a green light on it.

There are separate solutions, for example, like applications for Shopify merchants that need to deal with high-risk orders. Once such an alert is received, the plugin triggers an automated KYC check, and the buyer needs to verify their identity before checkout. This stops fraud in its tracks while identifying anomalies. Ongoing monitoring is also important for reporting suspicious transactions via a Suspicious Activity Report (SAR), which is filed with regulatory authorities like the Financial Crimes Enforcement Network (FinCEN).

Final Thoughts

Partnering with another entity that’s facilitating money laundering might sound completely insane, but the more you know about the evolving tactics and third-party risks, the more you tend to care about your fraud prevention strategy. For merchant fraud, it’s vital to protect everyone involved in a transaction, and that starts with assessing and verifying all B2B clients that are linked to your business.

For that, we recommend using automated solutions, like iDenfy’s Business Verification API. It enabled you to:

- Access up-to-date business registration data from official sources, including Secretary of State filings. You can also request required documents directly from clients using automated workflows and the KYB Questionnaire.

- Search across multiple states at once using unified keyword-based queries. Filter results and download structured PDF reports that align with your onboarding workflows.

- Scale KYB onboarding and improve efficiency when verifying clients or partners. The API reduces manual work and helps internal teams manage data and document requests more effectively.

Book a free demo and get a live dashboard walkthrough.