Creating accounts is convenient and simple online. Whether it’s a standard email account or a new profile on a marketplace, without stricter security measures like identity verification, it takes less than a minute. Some users create multiple accounts accidentally when they forget their original credentials — others get involved in multi-accounting on purpose to access new user benefits, such as promotional bonuses and discounts.

Multi-accounting isn’t necessarily fraud unless it’s later used as a way to commit crimes. However, it’s often against the company’s rules outlined in the Terms and Conditions, which prohibit using multiple accounts. This practice has been a popular tactic for bonus abuse in iGaming and other industries, raising security concerns for businesses.

What is Multi-Accounting?

Multi-accounting is the practice of creating different accounts within the same service under different identities. This approach helps the user to evade detection and engage in prohibited activities, such as avoiding being banned on the original account or accessing first-time-only account bonuses. Even though it might appear a harmless act, in the context of online platforms, multi-accounting is tightly linked to fraud.

This practice is also popular on social media sites when users have at least two accounts (for example, one public and one private account). Multiple accounts are also used when running ads. However, when it comes to fraud and multi-accounting, users often exploit this practice to access free trials or discount codes repeatedly. In sports betting, multi-accounting is extremely popular nowadays as a way to claim welcome bonuses.

The issue is that with guided YouTube videos, ChatGPT, or detailed tips in forums, users circumvent the rules and can create multiple accounts more easily. Companies that prohibit multi-accounting often have in-house Trust and Safety teams or use special software to monitor user behavior and spot red flags. Multiple accounts (profiles accessed from the same device or those that share the same IP, etc.) should be treated as one as well.

Stop fraud before it starts

From deepfakes to document forgery — iDenfy catches fraud attempts with AI-powered liveness detection and document checks.

Explore Fraud PreventionWhat is Multi-Accounting Used For?

There are various use cases for multi-accounting. For example, people use multiple accounts for:

- Bypassing regional restrictions. If some age-restricted services, such as adult content platforms or gambling sites, are illegal in a certain country, the user can create multiple accounts using VPNs and try to bypass such a ban.

- Bonus hunting. Popular on platforms like online casinos and betting, users create multiple accounts and digital personas to bypass checks and access new-user benefits without getting banned.

- Arbitrage betting. This involves creating multiple accounts to place bets simultaneously, calculating the outcomes, and winning no matter if the odds change. In case the primary account gets blocked, another one is used.

- Matched betting. This is a similar process in iGaming but involves using free bets to beat the odds. The winnings can be boosted when the user creates multiple accounts.

Users create such fake accounts using synthetic identities, or in less severe cases, they use another friend’s or family member’s identity. Creating another account using stolen or fake information is illegal and is considered fraud.

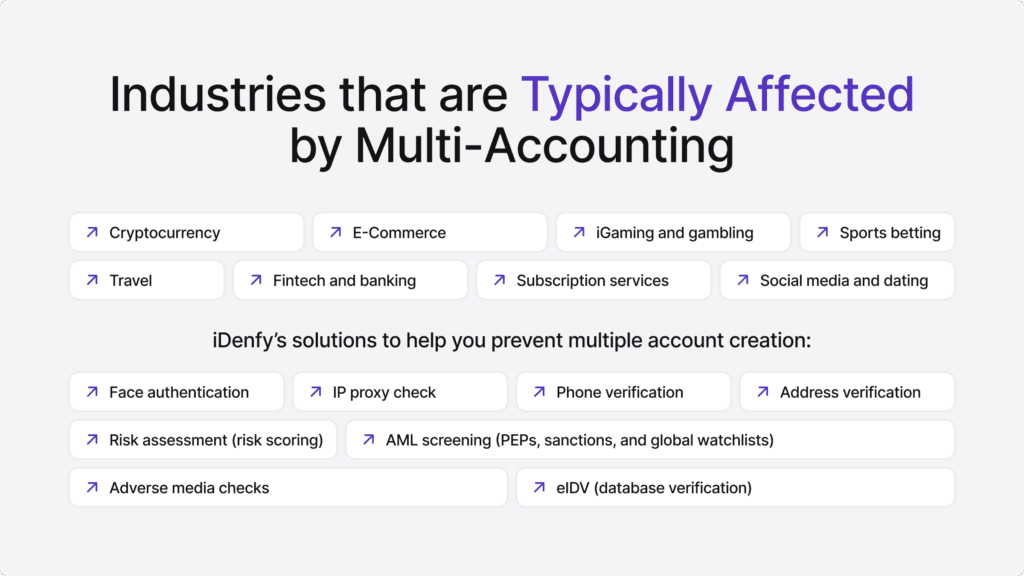

Which Businesses are Targeted Most By Fraudsters and Multi-Accounting?

Some industries are more prone to multi-accounting and fraudsters tend to find more ways to bypass security measures there. For example:

- E-commerce. This is related to issues like users exploiting bonuses and discounts, which are a popular method to acquire new users in e-commerce via subscriptions or referrals across multiple accounts.

- Travel and hospitality. Multi-accounting is used for false reviews or even fraudulent bookings.

- Betting and iGaming. Multi-accounting is used here for arbitrage betting and collecting in-game awards.

- Social networks and dating platforms. Romance scams are widely used to deceive users and phish out money by using multiple identities and fake personas.

Examples of Multi-Accounting Fraud

There are a lot of times when multi-accounting is used on purpose by fraudsters. In these cases, multiple fake accounts are used to manipulate systems and gain some sort of benefits or bonuses.

For example:

- Promo abuse. Also known as bonus abuse, it happens when fraudsters create multiple accounts to repeatedly claim one-time offers, free trials, or discounts using bots, VPNs and fake email addresses.

- Affiliate fraud. Fraudsters abuse affiliate marketing programs by creating several accounts to simulate fake transactions and referrals as a way to collect illegal commissions. This leads to wasted resources and distorted performance metrics.

- Fake reviews. In this case, fraudsters use and buy fake accounts or hire people to post deceptive reviews that mimic genuine customer language. This can be done both to boost the brand or harm its reputation.

Related: New Account Fraud — Alarming Red Flags and Ways to Fight Back

Why is Multi-Accounting Problematic?

When a user creates more than one account, they abuse the rules, which amplifies their capacity to scam and defraud the platform. Fraudsters use multi-accounting to bypass platform restrictions. They are often banned already for abusing the rules, which leads to them creating more and more accounts as a tactic to circumvent account-specific penalties. From a business perspective, this can lead to financial losses or operational disruptions, such as making it harder to catch such accounts and maintain the same level of security.

Sometimes, fraud rings use multi-accounting for phishing and other scams, which lead to further crimes, like account takeover (ATO) fraud and unauthorized purchases. Once this level is reached, the victim disputes the transactions, which then turn into chargebacks and losses for the online platform. Fraudsters also use proxies or virtual machines to create convincing user profiles that appear legitimate, shining a negative light on the business, which is used as a channel for fraud.

Related: Account Takeover (ATO) — Meaning, Examples, and Fraud Prevention Tactics

Three Methods Fraudsters Use to Exploit Multi-Accounting

When used in softer scenarios and not necessarily for fraud, multi-accounting can be achieved by creating more than one account from the same IP address. That means the person uses the same device and the same network, but uses another made-up name and a new email. Sometimes, more skilled users turn to VPNs to amplify their chances of staying hidden.

Other more severe tactics for multi-accounting include:

- Using deepfake technology. While sometimes used for good causes, deepfakes have become a sophisticated generative AI fraud mechanism created to bypass Know Your Customer (KYC) checks and, in this case, new identities for multi-accounting.

- Stealing personal information. This includes the use of deceptive practices, such as using phishing email campaigns, fake company websites, or combining stolen information with forged ID documents if needed to create a more convincing persona.

- Using gnoming. This is a commonly used practice in betting, also called “gubbing”, often used by professional players who are already banned by bookmakers and are trying to overcome this limitation. Sometimes, gnomers register under a family member’s identity; other times, they use emulators or virtual IPs to avoid getting caught.

So, while multi-accounting as a process alone isn’t illegal, it becomes unlawful when it’s used for fraudulent purposes like these. Apart from iGaming and sports betting, it also heavily affects banks, fintechs and other financial institutions, leading to an increased probability of non-compliance with KYC and Anti-Money Laundering (AML) standards.

For example, if during an AML audit, violations like an account with a stolen identity are detected, the company can be fined. What’s worse is that fraudulent accounts lead to increased fraud rates, such as attracting more accounts that apply for loans without the intention to pay, negatively impacting the company’s financials.

Related: Get Ready for Your AML Audit [Best Practice Guide]

Sanctions Imposed for Multi-Accounting

If the user is identified and found to have multiple accounts, they are notified about the platform’s policy. For example, in an e-commerce marketplace, they could be asked to delete the account and keep only one profile active; otherwise, they would stay blocked on all accounts.

Other actions that platforms use after detecting multi-accounting include:

- Requesting to complete the reverification process (and provide KYC data again).

- Reducing odds (this applies to the betting industry).

- Freezing or blocking the account temporarily.

In iGaming, this violation is treated more strictly and can result in a complete ban (which prevents access and fund withdrawals). The same principle applies to crypto platforms or social media networks where users get caught managing multiple illegal ad campaigns.

What is Money Muling?

Money muling is the process of using a “money mule”, or a person who either knowingly or unknowingly provides their personal details to receive illicit transfers (where laundered funds are used). Some money mules might not be fully aware of their involvement or at least not fully understand the scale of such a scheme or its consequences. Criminals often recruit money mules by promising quick and easy cash (a percentage for their “work”).

However, money mules must have a clean banking record. In the context of multi-accounting, criminals use money mules and their personal details to open multiple bank accounts for money laundering. “Herders” (which can be a single person or an organization) manage the multiple accounts and help conceal their true origins. That said, money muling is illegal, and money mules are accomplices in this crime.

Related: Smurfing in Money Laundering Explained

Red Flags Indicating Potential Multi-Accounting

Like in any type of fraud, criminals aim to exploit the system and access benefits, whether it’s sensitive data, money, or other benefits.

With multi-accounting, the same principle applies. For this reason, industries like e-commerce, crypto, fintech and other regulated entities use AI and other automated fraud prevention systems to spot suspicious user behavior and prevent fraud before it scales into serious issues, such as money laundering. If left undetected, multi-accounting can lead to fines and a damaged reputation.

Common warning signals and potential red flags indicating that the user has more than one account include:

- Suspicious purchasing behavior, such as making unusually large purchases or using the same discount code.

- Multiple accounts that are created from the same IP address or device.

- Frequent switching between these accounts.

- Accounts with similar names or other details, such as payment cards, address information, emails, etc.

- Anomalies in transactions, such as irregularities in selling or buying activities.

- Refusal to complete the identity verification process or provide an ID document during security checkups.

- Attempt to conceal the identity by using proxies or VPNs.

- Involvement in other suspicious activities, such as logging in from different locations at odd hours.

- Guiltripping the support team by creating multiple tickets claiming to have a single account when multiple signals show otherwise.

From a compliance standpoint, using automated RegTech tools and behavioral monitoring systems helps detect suspicious activity and such warning signs in real-time. That means you can prevent fraud first-hand, protecting your user base and your business from being involved in criminal activity. This is crucial because partnering with the wrong entity (both individual and corporate clients) can make you a target for money laundering, such as through money muling — a type of multi-accounting fraud.

Solutions to Prevent Multi-Accounting & Fraud in General

The number one prevention method to stop multi-accounting on any online platform is to conduct identity verification checks. They are also known as Know Your Customer (KYC) checks for users and Know Your Business (KYB) verification for other companies (an equivalent measure to prevent partnering with companies with hidden corporate structures or shell corporations used for money laundering).

Other AI-powered solutions that can help you mitigate risks and identify multi-accounting in real-time include:

- Phone verification (asking the user to provide their phone number or assessing their number info and detecting risk signals, such as their risk score based on the roaming country and more).

- Document verification (asking the user to upload their government-issued ID document to confirm their personal details. This automatically helps detect multiple accounts and helps prove when assessing cases when it’s hard to determine if the user is linked to some sort of account or not).

- Selfie verification (asking the user to record a selfie video presenting their biometric features or their face and then matching this data to their ID document. This is a second layer of defense next to the document check during KYC).

- Proxy detection (screening the user’s IP address to detect fraudulent IPs and proxies, which are often indicators of fraud or multi-accounting).

- Risk scoring (analyzing the user’s personal information based on different risk factors, such as their geographical location, and then determining their overall risk score to determine if they need extra verification steps).

- Address verification (asking the user to provide a Proof of Address (PoA) document, such as a utility bill, to check if the address information is legitimate. This also helps stop multi-accounting, as users try to register with the same address).

The best part is that iDenfy has all of the mentioned solutions and features in one place. We provide complete software for KYC, AML and KYB compliance, along with custom-tailored fraud prevention tools, which can be white-labeled, depending on your industry and specific use case.

Let’s talk so you can get a free tour.