While some e-commerce platforms or marketplaces seem to be thriving and multiplying their revenue by the minute, it’s not all fun and games, especially when we’re talking about fraud. Around 10% of returned items from online shopping sites are linked to some sort of fraud. For example, using stolen credit cards, taking over accounts, or engaging in return fraud are very common.

What’s worse is that, unlike illicit practices like phishing or friendly fraud, return policy scams happen after the customer makes a purchase, making them harder for online merchants to detect and manage. So, to this day, some companies find it challenging to eliminate refund fraud in real-time, especially since certain mandatory factors – such as return policies – need to be in place to keep customers happy and engaged. This is vital to scale and maintain sustainable business practices. But is there really a way to stop this?

RegTech service providers argue that the anonymous nature of online shopping has left a huge loophole, which can be easily managed with a single process: identity verification during checkout or before confirming a customer’s refund to prevent multiple fraudulent accounts, false identities, and repeated offenders.

To minimize financial losses to refund fraud and maintain trust among customers, purchasing goods shouldn’t only be a simple and frictionless experience for the customer. Businesses should have a clear strategy for fraud prevention, including transparent internal policies.

What else? We break it down for you below.

What is Refund Fraud?

Refund fraud, also known as refund abuse, is a fraudulent act when a person or a group of bad actors exploit an online shop’s return policy and falsely claim a refund. The goal is to trick the business into issuing them compensation for expenses that the fraudster never incurred. This way, criminals can keep the money and the products. Often, criminals lie that their purchase wasn’t “as described” or that it was “incomplete/unsatisfactory.”

Criminals succeed with this type of fraud by:

- Falsely reporting an issue with a received product or service.

- Deceiving a marketplace into refunding money for a product or service that wasn’t even purchased.

An example of refund fraud is when someone buys an item, breaks it, and returns it for a refund, falsely stating that it was already damaged when it arrived. Another standard scenario in a traditional retail world is when a customer shoplifts an item and then returns it to the store, claiming that they simply changed their mind and want to return the item and get their money back.

The Difference Between Refund Fraud and Return Fraud

Both are two types of fraud that are common in e-commerce as a way to exploit store policies. However, the main difference between refund fraud and return fraud is what happens to the items. Return fraud often involves physically returning the products, while refund fraud is designed to manipulate and defraud the merchant without necessarily returning any goods (including other alternatives, such as the box being empty).

However, keep in mind that sometimes, both terms are used interchangeably.

Is Refund Fraud Illegal?

Yes. Refund fraud is illegal and shouldn’t be treated as a victimless crime. Criminals and specially skilled bad actor groups defraud e-commerce platforms and traditional retail stores on a larger scale, resulting in losses for businesses. In general, crimes like refund fraud are prosecuted similarly to various crimes like theft, which can result in both jail time or fines, including punishments like house arrest or community service.

Related: What is a Transaction Dispute? [Challenges for Merchants]

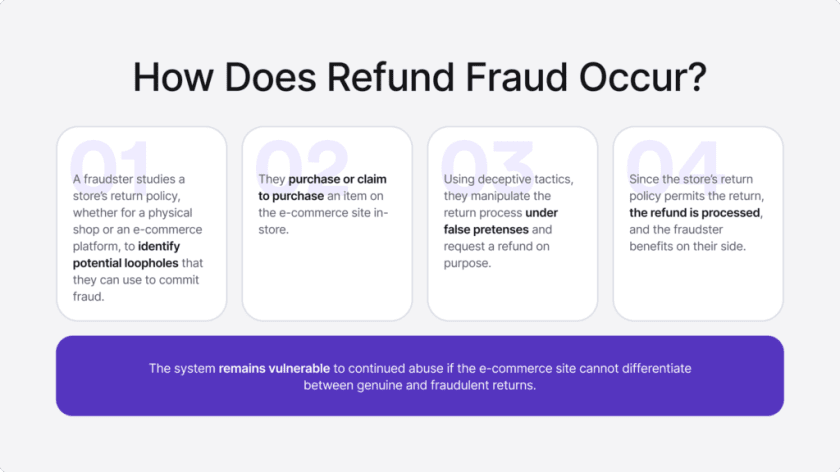

How Does Refund Fraud Work?

The typical flow for refund fraud to work on the criminal’s side consists of several steps, such as:

- Finding an e-commerce platform or on-site store and reviewing their refund policy.

- Purchasing an item with one goal – to abuse the refund process.

- Either returning or pretending to return the item while providing some sort of “valid” return explanation.

The company is then forced to process the refund if the request seems to be legitimate and fits the e-commerce platform’s policy.

For the fraudster, this means that they profited by tampering with the item, didn’t return it, or didn’t pay for it originally. In the meantime, the business is left with losses of revenue, inventory, or, worse, both. In the long run, refund fraud can also harm any company’s reputation with customers.

What are Some Typical Types of Refund Fraud?

Fraudsters use a variety of tactics and strategies to successfully exploit merchants. Consequently, it’s important to be aware of their techniques and detect malicious behavior in real-time before it spreads and results in even more financial losses for the business.

Here are some of the most common refund fraud techniques right now:

- Tax return fraud. It involves forging and submitting fake tax returns as a way to claim a refund that isn’t actually meant for the fraudster. Often, bad actors use stolen personal data to manipulate the system.

- Fake refund request. It happens when a criminal claims they never received their goods or that they arrived damaged. If it’s a low-cost item, many e-commerce platforms do not require the customer to return it, so they keep the product and the refund.

- Chargeback fraud. It occurs when a buyer opens a dispute on a legitimate credit card transaction, providing false claims, such as the item was not received or that the charge was unauthorized. Here, the goal is to receive a refund as well and keep using the item or service. Sometimes, chargeback fraud is referred to as double dipping.

- Price arbitrage. It happens when the fraudster buys two similar items and returns the cheaper item, keeping the more expensive product while still receiving a refund.

- Stolen card refund. It involves a fraudster stealing a credit card and purchasing an item. Then, they return the item to receive a refund to their own bank account.

- Tender liquidation. It happens when a criminal uses a stolen credit card, but after they purchase the item, they return it for store credit.

- Insurance refund fraud. It occurs when a criminal submits a fake or exaggerated insurance claim to secure a refund from an insurance company, often claiming that an accident happened, which resulted in damaged goods.

- Price switching. It is when a fraudster replaces the barcode or price tag with a cheaper one, purchasing the expensive item for a lower price and then using the original (higher-priced) receipt to return the item for a full refund.

Sometimes, fraudsters even use money laundering techniques to score high-end, luxury items with dirty cash or use refunds to enable money laundering and clean the illicit funds by receiving reimbursements with seemingly legitimate money.

On a bigger scale, fraud rings offer their services for less skilled bad actors and offer step-by-step guides where there are instructions on how to conduct refund fraud, listing share percentages and conditions on how to share the profits of the refund payment.

Related: AML Fraud – Types and Detection Measures

What’s the Difference Between Refund Fraud and Return Fraud?

Refund fraud and return target different areas of the refund process; however, both are similar, since they are designed to trick businesses and forward all of the benefits to fraudsters, which are gained in an illicit manner.

In a more detailed way, the scope of the fraud type also differs, for example:

- Refund fraud aims to exploit a bunch of refund mechanisms, like false insurance claims or chargeback abuse, for personal gain across various sectors, from banks to government institutions.

- Return fraud aims to manipulate return policies, specifically by using online and traditional retailers only. This involves claiming the item arrived not as described or defective, among other tactics, such as using stolen goods, to access the refund and earn money.

So, in this case, return fraud can be merged into the refund fraud category; however, it doesn’t have to necessarily involve product returns. Both types are known to be harmful for businesses due to lost revenue and trust among genuine customers.

Why is Refund Fraud So Common?

While a refund is a right that most customers use legitimately, abusing the policy has become a standard practice for less skilled bad actors due to the seemingly simple way to shop online these days. So, while not all returns are fraudulent, this sort of abuse has resulted in millions of losses for merchants, reaching a new height of $101 billion in damages in the US alone in a single year. Most of this comes from the fact that buyers don’t have to provide their IDs during checkout or before a refund, making this highly automated transaction process a relatively anonymous channel to commit fraud.

The same principle applies to brick-and-mortar stores, where buyers are required to show physical receipts before the refund. That said, they can be forged, especially when the customer isn’t required to provide additional documentation, such as their personal ID document. Additionally, in the online space, other criminal acts like multi-accounting, providing fake personal information (including the name or date of birth, or hiding the true address by submitting PO box data), and using proxies and VPNs to hide the true IPs take e-commerce and marketplace fraud to the next level.

That’s why companies need stricter security measures to monitor the customer journey even after an account is created or a purchase is made. User behavior can change, and a previously trustworthy customer may suddenly begin making fraudulent refund claims.

Measures to Prevent Refund Fraud

A single measure won’t stop refund fraud and it won’t prevent bad actors from using your business for their own benefit and illicit activities. Despite that, combining multi-layered tactics and different solutions, both of which require your manual input (like training) and implementing software (such as AI-powered third-party fraud prevention solutions) and automated tools can help identify red flags.

We look into each step below.

Implement Clear Refund Policies

If you want to reduce the chances of refund fraud to strive in your e-commerce business, you need to have clear refund policies that are strict and detailed. They should inform the buyer about the consequences of abusing the system and how and when exactly the items can be returned. Keep in mind that refunds and returns are allowed, which means that you won’t be able to push fraud out the door completely (fraudsters are here for a reason, and they want to take advantage of any refund system), but you’ll minimize the rate of fraudulent refunds.

So, to put it simply, your goal is not to stop legitimate returns and refunds, as this often leads to an increased chargeback rate and loss of funds, but to achieve a balance by detecting those who abuse the system on purpose.

Related: Chargeback Fraud Prevention – Key Strategies for Businesses

Train Your Team to Identify Fraud

The ugly truth is that once the refund fraud happens, you have limited options: report the customer to the police, inform the delivery service, or flag them in your marketplace. However, if they do this for a living and are part of a professional fraud ring, such methods are often ineffective, costly, and labor-intensive, especially if you don’t have in-house Trust and Safety teams that dedicate their time to detect suspicious users and their transactions on the marketplace.

That is why it’s very important to have a well-trained staff that knows how to spot potential fraud signals. For this to work, you need to manage in-house training and provide guidelines on how to handle various risk signals and suspicious transactions, or refund requests.

Enable Blocking and Use Automation for Fraud Prevention

Some online marketplaces offer tools like blocking other buyers from risky locations or those who have many negative comments. On Vinted, one of the largest second-hand item marketplaces, Counterfeit and Safety teams block users that sell replicas, demand both keeping the items and the refunds and create multiple accounts to conduct fraud, like account takeovers, etc.

Other alternatives include using automated fraud prevention tools like Proxy Detection (to see the user’s IP, if they’re using the TOR browser, etc) or Phone Verification (to duplicate accounts and check the legitimacy of one’s number).

Monitor User Transactions

Some countries have stricter compliance regulations for e-commerce businesses, which require implementing mandatory Know Your Customer (KYC) or identity verification measures on customers, as well as other Anti-Money Laundering (AML) processes, including transaction monitoring. Screening and keeping an eye on users’ transactions helps platforms detect suspicious behaviors, especially those linked to their transactions that show anomalies and deviations from their typical activity.

Paired with other fraud prevention tools that are based on behavioral biometrics, it helps merchants detect potential fraudsters trying to exploit the refund policy (for example, automatically spotting suspicious users who request multiple refunds within a short timeframe). This also helps stop unauthorized charges before they happen, even if there is a potential account takeover on the platform. From a legal standpoint, transaction monitoring helps ensure compliance by detecting fraudulent activities while preventing legal penalties.

Related: What is a Transaction Dispute? [Challenges for Merchants]

iDenfy’s Identity Verification as a Measure to Prevent Refund Fraud

Verifying the customer’s email address or checking the IP address linked to the requested refund might not always be enough. Even if your business isn’t regulated (required to implement ID verification checks), you can automatically ask your buyers to provide a government-issued ID before checkout or before requesting a refund for an item as a second layer of security.

iDenfy’s software has various KYC tools where you can combine such checks with selfie verification or customer reauthentication for risky scenarios (like before they purchase a large, high-value item or show atypical signs of behavior, like changing their email address, which can lead to an account takeover). Gathering and verifying multiple data points and then cross-referencing them with previous purchases or onboarding data in the system helps prevent refund fraud and reduce chargebacks.

Verifying users helps your marketplace or any e-commerce project save costs while building a fully automated fraud mitigation system that doesn’t result in a negative experience for the end user.

For example:

- Customize the IDV flow only for risky users to reduce drop-offs (instead of allowing guest purchases or applying the same verification process for everyone, including low-risk customers).

- Add extra checks, such as IP address detection or address verification, to track different risk signals (to ensure that the customer isn’t using a duplicate account and they aren’t linked to an already blocked, fraudulent user).

- Maintain accurate records and access history logs (including transaction records if needed through solutions like Bank Verification).

Want to learn more? Check out our success story with The Everset, a premium furniture rental platform. By implementing our ID verification solution, they reduced fraudulent accounts by 83%, leading to inventory cost savings and increased recurring revenue.

Want to get a more hands-on experience? Talk to us, and we’ll show you around our dashboard.