Financial institutions must follow these guidelines to prevent fraud attacks, safeguard customer data, and avoid penalties. These institutions use KYC as a measure to meet those guidelines. Through KYC, institutions verify a customer’s identity using their identity documents.

The phrase “know your customer” has become increasingly prominent in today’s business landscape, particularly in sectors such as banking, finance, and e-commerce. But what exactly does it mean, and why is it so important?

Let’s jump right in and find out more about KYC.

Fraud detection and prevention service from market leaders. Schedule a free demo here.

What is Know Your Customer (KYC)?

Know Your Customer (KYC) is a process that financial institutions and businesses implement to verify the identity of their customers and assess their potential risks. It involves gathering information about individuals or entities, such as their name, address, date of birth, and other relevant details.

This information is then used to establish the customer’s identity, evaluate their suitability for certain products or services, and ensure compliance with legal and regulatory requirements.

In other words, KYC involves running background checks when a customer signs up for the onboarding process. Businesses conduct a risk assessment procedure to verify a client’s identity and meet regulatory compliance.

There is a corporate KYC as well that is an extension of standard KYC policies. Companies use corporate KYC to verify businesses during the deal signing. Like standard KYC, corporate KYC helps identify fake companies and acts as a shield against terrorist financing and money laundering. Sometimes, businesses also refer to corporate KYC as Know Your Business (KYB).

KYC Meaning in Business

The primary goal of KYC is to prevent financial crimes, such as money laundering, terrorist financing, fraud, and identity theft.

By verifying the identity of customers and understanding their financial activities, organizations can detect and deter any suspicious or illicit transactions. KYC also serves as a means to protect customers’ interests, as it helps prevent unauthorized access to their accounts and safeguards their personal information.

Below, we go into more detail about the importance of KYC:

For companies

Financial institutions or companies create KYC procedures containing all the vital actions to verify their clients. On top of it, KYC helps banks assess, monitor, and resolve any risks. Once a business can verify that their customer is genuinely who they claim to be, they can prevent a cyberattack. It also helps them prevent terrorist funding, money laundering, or any other illegal financial racket.

Generally, a KYC process involves ID, facial, document, and biometric verification. All banks must fulfill anti-money laundering and KYC regulations as the KYC compliance responsibility rests with them. The KYC process also helps companies avoid financial penalties that regulators impose as well as reputational damage. Since the financial sector is always at risk of financial fraud, crimes, and attacks, background checks help mitigate fraudulent activities.

For clients

For clients and customers, trust is a vital part of doing business with someone. When banks and businesses conduct a thorough KYC process, it assures the customers that banks value security and safety. The KYC process aims to protect sensitive customer data, funds, etc., from a cyberattack. The KYC process is a sort of quality assurance about the respective bank for the client that their funds and personal information are safe.

Also, by providing the necessary document for KYC, a client helps the bank or a company ascertain that they are who they claim to be. This way, the bank can clear the onboarding process and serve the client faster. It means there is less delay in getting loans or finances or opening an account.

Ensure your customers are real. Schedule a free demo here.

KYC Process Requirements for Banks

The process of KYC typically involves multiple steps. Initially, customers must provide basic identification documents, such as a government-issued ID, passport, or driver’s license. In some cases, additional documents may be requested to establish the source of funds or verify the customer’s address. These documents are carefully reviewed and authenticated by the institution’s compliance teams.

For banks and companies to conduct a proper KYC process, they need two primary components:

1. Customer Identification Program (CIP)

The initial KYC process involves acquiring and verifying a customer’s Personally Identifiable Information (PII). This initial phase is known as the Customer Identification Program (CIP). CIP aims to limit corruption, terrorist funding, money laundering, and other illegal activities. Improper or incorrect ID verification can lead to serious issues; hence, CIP is vital for a thorough KYC process.

But since there are no concrete KYC guidelines, there is no single CIP process that every financial institution can use. The CIP gives general instructions, but the companies need to decide which PII they would ask for according to their policy.

Companies generally ask their clients for PII that includes:

- Client’s full name

- Their date of birth

- Their address

Once the client provides these details, they might have to produce official documents like a driver’s license, ID card, passport, etc.

2. Customer Due Diligence (CDD)

Banks and companies must determine if they trust a probable client. Customer Due Diligence (CDD) plays a crucial part in risk management and safeguarding the bank against potential attacks.

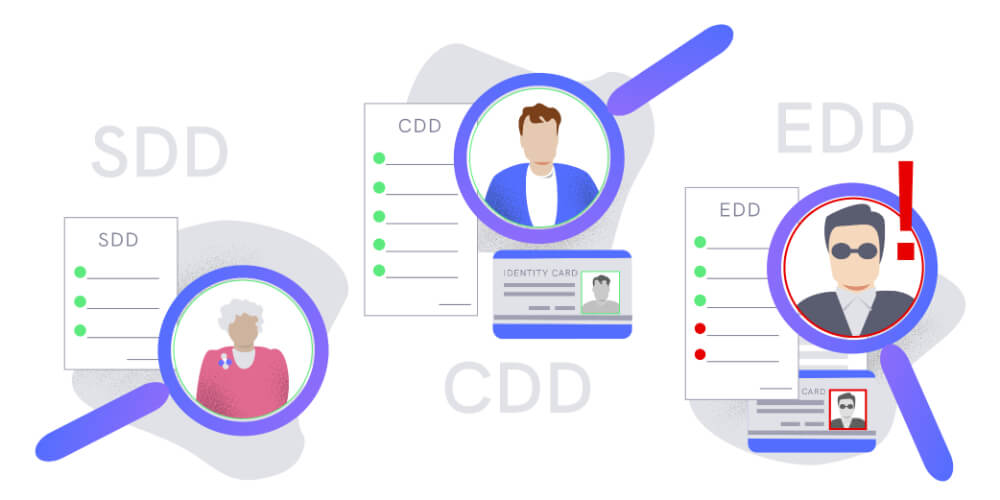

There are three levels of CDD, and each level is designed to handle clients based on their risk levels:

Simplified Due Diligence (SDD)

Financial institutions use SDD for clients with low risks of potential terrorist funding or money laundering and no need for full CDD.

Basic Customer Due Diligence (CDD)

Banks use it to cover basic details required for customer identification and verification.

Enhanced Due Diligence (EDD)

Enhanced due diligence is specifically used for higher-risk clients. It involves obtaining additional information. The banks then use this information to understand the client’s fund activity and prepare for any risk.

KYC Regulations Around the World

Governments and regulatory bodies worldwide have recognized the importance of implementing robust KYC frameworks to maintain the integrity of their financial systems.

Below, we explore KYC regulations worldwide and highlight key compliance aspects in different jurisdictions.

Australia

The Australian government formed the Australian Transaction Reports and Analysis Centre (AUSTRAC) in 1989 to monitor all the country’s financial transactions. The center also directs client identification requirements in Australia.

Canada

Canada established its Financial Transaction and Reports Analysis Centre of Canada (FINTRAC) in 200 as its financial intelligence unit. In June 2016, the unit updated its regulations to ascertain individual clients’ identities and ensure AML and KYC regulations compliance.

India

In 2002, the Reserve Bank of India introduced its KYC guidelines for the country.

Italy

The Banca d’Italia set the KYC requirements in 2007. It explained the requirements that all financial institutions operating in the Italian territory must follow.

United Kingdom

The Financial Conduct Authority (FCA) demarcated the Money Laundering Regulations 2017 to govern the KYC regulations in the UK.

United States of America

The Secretary of the Treasury had to finalize KYC regulations before October 26, 2002, in line with the USA Patriot Act of 2001. It made KYC compulsory for all US banks. All the processes that followed the regulations must satisfy a customer identification program.

European Union

The EU has two anti-money laundering directives that govern the union’s KYC regulations. They published their Fifth Anti-Money Laundering Directive (5AMLD) on July 9, 2018, and came into effect on January 10, 2020. On the other hand, the union published the draft for 6AMLD in late 2018, which came into effect in June 2021.

Rest of the World

KYC regulations are not limited to specific regions and have been implemented across the globe. Many countries, including Australia, Canada, Switzerland, and South Africa, have established their own KYC requirements and regulatory frameworks to ensure compliance with international anti-money laundering (AML) standards set by organizations such as the Financial Action Task Force (FATF).

How iDenfy Can Simplify the KYC Process

Understanding KYC is one thing, but complying with these regulations is another task. There are too many complicated terms with open grounds for manipulations.

KYC often involves the use of advanced technology and data analysis techniques. Many organizations leverage automated solutions and artificial intelligence algorithms to streamline the process, enhance accuracy, and reduce manual effort.

Automated tools can efficiently analyze vast amounts of data, cross-reference information with external databases, and flag any potential risks or discrepancies.

iDenfy has designed highly accurate AI-based identification tools that can help you conduct eKYC and online identification. With iDenfy, banks can devise their KYC process and conduct the time-consuming PII gathering process, customer identification, and verification within minutes.

Equipped with highly-advanced machine learning and artificial intelligence, iDenfy can verify a customer’s ID documents using available public data online like residential papers, bills, etc. iDenfy keeps learning while collecting essential data points that eventually help the tool itself to perform better.

Several companies worldwide have used iDenfy and its ID verification services to run their KYC process and reach complete compliance.

Verify customers identity within 15 seconds. Schedule a free identity verification demo here.

💡Interesting Facts About KYC Trends

- Recently, the realm of KYC due diligence has undergone a notable expansion to incorporate environmental, social, and corporate governance (ESG) factors.

- By 2027, the wider market for digital identity solutions is projected to reach a substantial value of $70.7 billion.

- Complex identity fraud schemes have risen, making it more difficult to manage and prevent crime.

- Companies spent nearly $1.4 billion in 2021 on AML and KYC services.

- Online fraud risk has reached unprecedented volumes causing real challenges for digital growth.

This post was updated on May 26, 2023, to reflect the latest insights.

Verify customers identity within 15 seconds. Schedule a free identity verification demo here.