Biometrics in banking are more common than some of you might think. Financial institutions have replaced traditional systems with biometrics, such as facial recognition, fingerprint sensors, or voice recognition technology. For Know Your Customer (KYC) verification in particular, biometrics help ensure regulatory compliance, creating a smooth and secure digital identity verification process.

What’s special about biometrics is their advantage against passwords. Suh authentication methods based on knowledge, including PINs or OTPs, can be easily stolen or forgotten. In contrast, biometric verification methods, which are the central focus of today’s digital payment systems, enable users to access their accounts using their distinctive biological traits.

In this blog post, we take a more in-depth look at this technology, explaining the facial recognition process and the main use cases of biometrics in banking.

What are Biometrics in Banking?

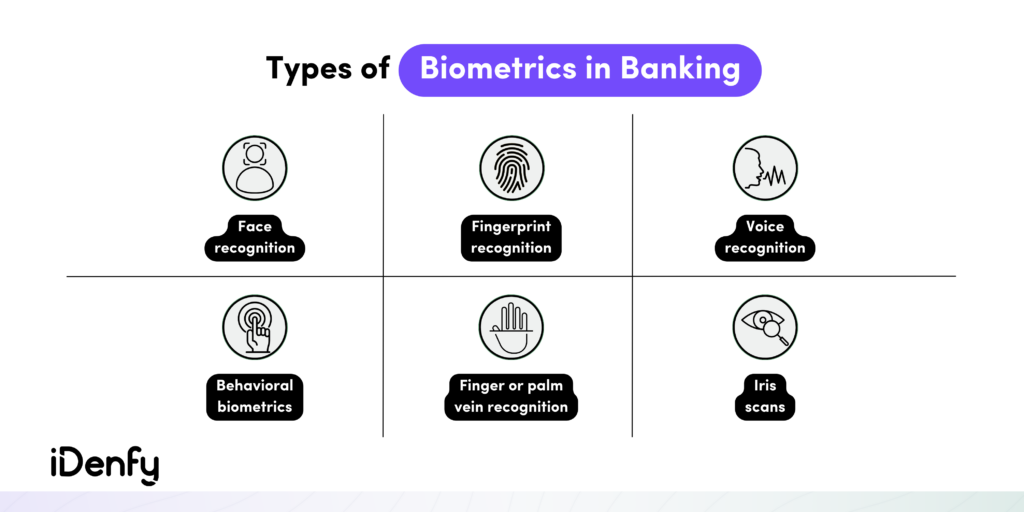

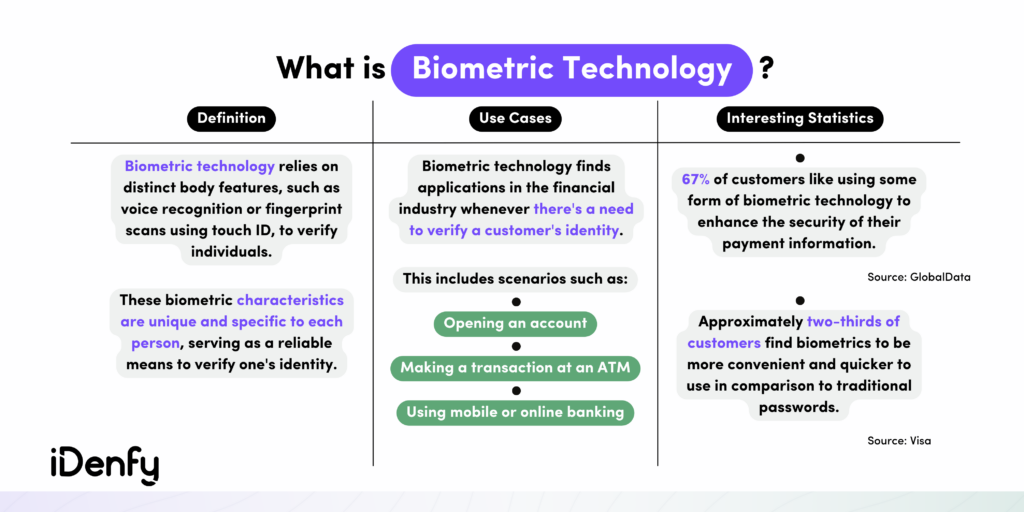

Biometrics in banking is the use of unique physiological or behavioral characteristics of individuals for authentication and security purposes in digital banking transactions and account access. These characteristics can include facial recognition, voice recognition, fingerprint scans, or retina recognition.

Biometric authentication is quickly becoming a fundamental component of the banking industry due to its ability to offer highly secure identity verification processes. Apart from that, biometrics are also used for applications in mobile banking, online banking, ATMs, and even in-branch banking.

What is Facial Recognition?

Facial recognition is a technology-based method for identifying a person’s face by analyzing their facial features. Typically, banks extract this information from a photograph or video. This data is then compared against a database of collected faces to find a matching individual.

Facial recognition software leverages technology powered by artificial intelligence (AI). Often, banks use facial recognition technology for their identity verification processes. This is how it works:

- The software receives a video or an image with a person’s face.

- It scans this data to create a detailed map of the person’s features, including precise information about their eyes and other distinctive facial characteristics, such as scars.

- Based on this comparison, the facial recognition system determines whether the facial map matches anything in its database. Some systems may also determine the customer’s risk score or provide alternative results.

For example, Apple first used facial recognition, enabling users to unlock the iPhone X and access their digital wallet. Since then, the company has kept incorporating facial recognition into newer models. According to the big tech company, the likelihood of someone with a random face being able to unlock another person’s phone is approximately one in a million.

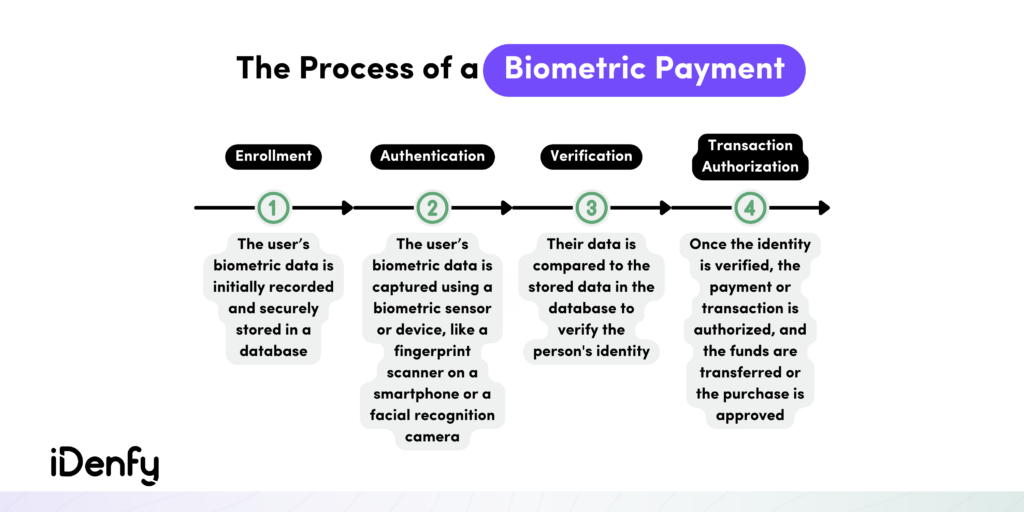

What is a Biometric Payment?

Biometric payment refers to a point-of-sale (POS) technology that’s based on biometric authentication — relying on unique physical characteristics to verify the user’s identity and enable the deduction of funds from their bank account. Familiar biometric payment examples include Apple Pay or Google Pay. They allow users to purchase items through Face or Touch ID.

Biometric technology gained recognition in the mid-2000s, particularly in settings such as grocery stores, gas stations, and convenience stores, where it facilitates swift and secure transactions. Additionally, online retailers like Amazon have embraced biometrics for one-click payment processes, focusing on the convenience of online shopping. Moreover, banks employ biometric verification for safeguarding high-risk transactions, such as large monetary transfers, ensuring enhanced security.

That’s why consumers now primarily use mobile devices for their interactions with financial services. This shift has seen smartphones take over from desktop PCs for everyday banking activities, including standard tasks like accessing online accounts, making money transfers, and handling online payments.

Why do Banks Need Biometrics?

With the rise of advanced transactional technologies to combat fraud, conventional security measures are no longer adequate. As a result, integrating biometric technology into banking systems is paramount for protecting against data breaches and other security threats. So, although digital banking offers numerous advantages for both banks and customers, it also presents a significant security challenge.

The main challenge comes from the obligation to build trust by verifying the identity of individuals accessing online banking services, which criminals can exploit. As banks make digital services more accessible and user-friendly, they naturally create opportunities for fraudsters to exploit this open door and engage in fraudulent activities.

Adopting biometrics aligns with the industry’s goal of providing customers with secure, convenient, and user-friendly banking services. Overall, banks need biometrics to:

Comply with Regulatory Requirements

Biometric technology offers an effective measure for banks to fulfill their KYC and Anti-Money Laundering (AML) requirements. Financial institutions often use biometric identity verification during the account opening process to check their users’ identities before granting them access to their services. Due to its high level of security, biometrics also serve as a robust safeguard, helping banks mitigate the risks associated with financial crimes and money laundering, which often accompany fraudulent activities.

Prevent Fraud

Biometric identity verification not only strengthens identity assurance for regulatory compliance but also serves as a robust defense against fraud. It ensures that transactions aren’t fraudulent, and, importantly, it does so more efficiently than traditional methods used by banks to verify the account holder’s identity. This efficiency is crucial considering that the Javelin 2022 ID Fraud Study found that around 22% of U.S. adults, equivalent to roughly 24 million households, have encountered account takeover (ATO) incidents.

To prevent such attacks and other types of fraud, especially identity theft, banks combine biometric verification with other authentication measures, such as a PIN or a password, creating a multi-factor authentication (MFA) system. This multi-layered approach adds an extra level of security by requiring both something the user knows (like a password) and something the user is (their biometric trait).

Provide Convenience

It’s literally the need for speed when it comes to banking services and their users. When a financial service provider faces a delay during the customer identity verification process, it not only leads to a poor user experience but also raises the chances of customers abandoning the process. Biometrics are the key that helps banks provide swift and frictionless ID verification processes for establishing customer trust and simplifying the onboarding process.

According to Juniper Research, mobile biometrics are projected to facilitate around $2 trillion in in-store and remote payments by the end of 2023, marking a significant increase from the previous years. This popularity is mainly due to the fact that biometrics can streamline in-branch banking procedures, making transactions smoother and more efficient.

What are the Use Cases of Biometrics in Banking?

Biometrics provide banking customers with a simple and convenient way to both sign up or regain access to their online bank accounts. But that’s not all. Let’s explore some of the main use cases:

1. Customer Onboarding

The first step in the customer onboarding process involves identity verification. This is how banks ensure that they are dealing with a legitimate person from the start, allowing them to filter out potential criminals early on. This is where biometrics come in to help banks build a simple and secure way for customers to open a bank account.

Additionally, this is a crucial step because banks are obligated to adhere to KYC/AML, which requires ID verification. Traditionally, this process took place in person at a physical branch. Today, as part of customer onboarding, users are asked to scan a trusted identity document, like a passport or a driver’s license, and then complete a brief biometric facial scan. This ID step enables banks to confirm the identity of each new customer without the need for an in-person meeting.

The onboarding stage presents the highest level of risk because, initially, there is limited information available about the user or their risk profile. Therefore, it’s crucial to begin with the highest level of identity assurance to defend against threats like deepfake technology or synthetic identity fraud.

2. Customer Re-Authentication

Biometrics, particularly facial recognition technology, enable banks to implement a swift and secure re-authentication process that eliminates the need for users to rely on traditional passwords when logging into their accounts. That’s crucial because legitimate accounts can still become compromised later in their customer cycle. Biometric face re-authentication consistently verifies that the individual attempting to access the account is indeed the same person who initially created the account.

Re-authenticating the customer isn’t always an option for banks. Financial institutions do this in cases when the customer poses a higher risk of money laundering, for example. Other cases when banks re-authenticate their customers are when they request additional credit, initiate a password reset, change their personal information, request a large transfer, or add a new device. This approach allows banks to strike a balance between convenience and security for their customers.

📎 Related: What is the Difference Between CDD and EDD?

3. Mobile Banking

Mobile banking is experiencing rapid global growth, where biometrics play a vital part. Using a fingerprint or facial recognition for authentication, we can make payments anywhere, anytime. Integrating biometric technology with existing fraud prevention systems means that banks can provide the highest level of security available. At the same time, banks can present greater confidence in mobile banking among their customers, especially if they utilize secure digital banking software.

And with the ongoing battle against criminals online, banks need to find a way to safeguard their customers. For example, a common tactic that hackers use is credential stuffing. It happens when criminals try to steal usernames and passwords on numerous online services. This scheme is often successful because users find it hard to create secure passwords for every online account they have. Biometrics solve this problem.

4. Branch Banking

Utilizing fingerprint, facial, or iris recognition within financial service institution branches ensures rapid and reliable biometric authentication, even during peak activity periods. For example, banks use biometrics to grant access to safe deposit boxes, ensuring that only authorized individuals can access their contents.

Similarly, when customers visit these branches, they can undergo authentication at the service counter by matching their fingerprint, facial features, or iris scan with their pre-registered biometric data stored in the bank’s database. Biometrics can also help identify regular customers as they enter the branch, enabling staff to offer personalized assistance and services based on their previous interactions and preferences.

5. ATMs

Biometrics in ATMs have become popular in many developed countries. Consequently, some banks integrated fingerprint recognition technology into their ATMs. Customers can link their fingerprints to their bank account, and when they visit the ATM, they simply need to place their finger on a biometric sensor.

The ATM scans and matches their fingerprint with the stored data to verify their identity. Once verified, customers can proceed with their transactions, such as cash withdrawals or balance inquiries, without needing a physical card or PIN. That’s why this identity proofing method provides both convenience and accuracy while requiring minimal space.

Why Biometrics are Here to Stay

The fintech sector and banks benefit from integrating biometrics and selfie verification into their services. iDenfy’s identity verification solution is also powered by AI and has built-in liveness detection technology.

It enables customers to verify their identities using their biometrics easily. Using automation not only makes the verification process fraud-proof but also reduces the time and effort required to open new accounts or access financial services. Zero friction, increased security, and a seamless balance of user experience and proper fraud prevention.

Read our customer success stories to see this formula in action, or get started right away.