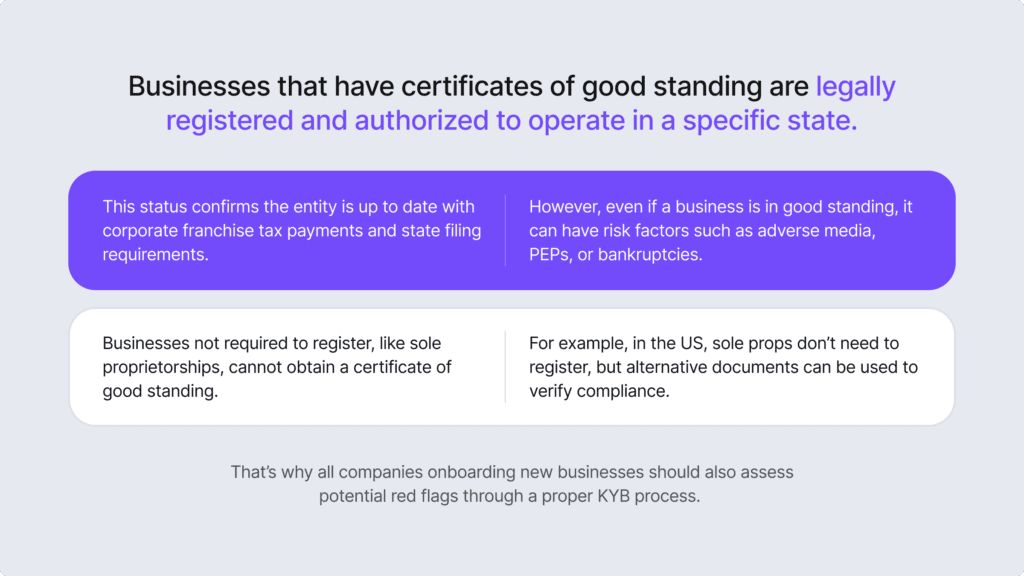

Companies that want to maintain their good standing status and comply with various financial requirements must stay current with state reports, pay fees and taxes, and be legally registered in their jurisdiction. So, in other words, a certificate of good standing helps you verify if the other business is legitimate. It confirms that the company is compliant and legally registered with the state. At first glance, checking if another company is in good standing is simple. All you need to do is visit a website and search for the name. However, having this status doesn’t mean that the business is risk-free.

That’s why additional Know Your Business (KYB) checks are vital when starting a new business relationship. This sort of background check helps find adverse media, Politically Exposed Person (PEP) statuses and other vital information that you need to comply with anti-money laundering (AML) requirements. For that, financial institutions and other regulated businesses need to follow the risk-based approach, asking the ultimate question of whether it’s the right move to onboard this business and start the partnership.

In this blog post, we explain how to check another business’ status, what it means if the company is in “good standing,” and what extra requirements and risks you need to know when verifying corporate clients.

What Does “Good Standing” Mean?

If an entity is in good standing, that means it has paid all necessary fees and filed the required reports to the relevant authorities. A good standing includes filing paperwork and consistently meeting compliance requirements, such as retaining documents and meeting financial obligations, including paying taxes on time. This status confirms that the entity exists and that it can legally do business in the state.

Having a certificate of good standing is important because it:

- Verifies that the business is legally registered with the state.

- Confirms that the business is compliant and active.

- Shows their financial health and that the company is prepared to legally open a business bank account, obtain a loan, etc. (otherwise, lenders often don’t engage with the entity).

Larger companies like limited liability companies (LLCs), corporations and any entities formed in a state or registered as foreign entities in that state can request a certificate of good standing. Despite that, this status isn’t the same as having an occupational or business license, which is also often a legal requirement for companies to stay compliant. That means there are cases when the business can work legally without having a certificate of good standing.

Automate your identity verification

See how iDenfy helps 1,000+ companies verify customers in seconds with AI-powered KYC.

Explore iDenfyExamples When a Business is not “In Good Standing”

If the company fails to meet at least one of the regulatory requirements, that means they failed to meet proper registration rules and are not in good standing. For example, in certain states, businesses can lose their good standing if they don’t pay the franchise tax on time.

Another example is when the company relocates without notifying the Secretary of State and, as a result, fails to file the annual report notice. So, in general, common cases include not paying certain fees or not meeting paperwork deadlines, including not designating a registered agent.

Losing good standing can lead to several negative consequences, including:

- Tax liens

- Loss of limited liability protections

- Restrictions, such as restricted access to state courts

- Dissolution within the state

- Fines and other penalties

For example, when it comes to legal matters, the company might be unable to initiate lawsuits until they regain good standing. In this case, there’s also the risk of losing the business name to another company (if it doesn’t violate trademark laws). Additionally, not being in good standing can lead to the company facing stricter scrutiny. However, this does not generally affect the company’s contract rights.

What is the Secretary of State?

In the context of good standing in business, the Secretary of State’s office manages business registrations within their jurisdictions in the US. This is essential for legally conducting business in a state. However, other factors are also important, such as being in good standing with the Internal Revenue Service (IRS), the primary tax authority in the US.

To assess all factors, companies use KYB software and do business registry lookups to check various databases, such as the Better Business Bureau (BBB), where you can access official and reliable government reports to ensure that the companies that you work with are low-risk, compliant entities. A business may have a certificate of good standing but still pose risks, such as a high likelihood of bankruptcy.

Related: The Main KYB Risk Factors You Should Know

What Situations Require to Provide a Certificate of Good Standing?

Before an entity expands into another state, it needs to show the Secretary of State office there that they are in good standing with the state where they operate. This is a requirement before starting operations in different jurisdictions. However, there are other scenarios that require a certificate of good standing.

For example, even if not legally required to operate in a state, a certificate of good standing is vital for:

- Selling a business

- Insuring or funding a business

- Attracting new business partners

- Renewing permits or licenses

- Opening a business bank account

- Forming contracts with other businesses

- Setting up payment systems

- Buying property for your business

- Receiving government contracts

- Registering to operate in another state

For example, if you’re applying for a business loan, you’ll require a certificate of good standing to prove your entity’s status and to show that you’re compliant. The same goes for when you’re attracting new investors or Proof of Income during financial audits. Another situation where you’ll need to be “in good standing” is when entering new business contracts. Some partners or clients request this document to check if your company is operating legally as a guarantee to assure that you’re meeting compliance and contractual obligations.

Types of Companies that Can Get a Certificate of Good Standing

Registered businesses are eligible to obtain a certification of good standing. That’s mainly because they are required to register with their state. Once that’s done, regulatory bodies monitor entities and review compliance procedures with state regulations to check if the business is still active.

It depends on the state and the exact process for getting a certificate of good standing. It involves a government agency, such as the Department of Revenue or the Secretary of State’s office. Some offer remote application portals and others will ask you to go through an authorized service provider.

In general, these are the types of entities that can get a certificate of good standing:

- LLCs

- Partnerships

- Limited partnerships

- Limited liability limited partnerships (LLLPs)

- Corporations

- Other legally recognized business structures

Keep in mind that some types of businesses, such as a sole proprietorship, may not be eligible for this document, as they are not required to register with the Secretary of State. Additionally, banks can sometimes request a “bank letter of good standing,” which serves the same purpose. It also confirms the status of the existing relationship between a bank and its customers. For example, a business representative with an account at the bank can request this document to verify and acknowledge the established business relationship.

Who Needs to Check if Another Company is in Good Standing?

Many businesses use this document to check if another company is legitimate. That’s because it’s a relatively easy way to assess whether the entity is reputable, compliant, and genuine.

So, even if a business is not legally required to have a certificate of good standing, maintaining good standing can be a valuable way to demonstrate transparency. That’s particularly important in various stakeholder interactions, showcasing the business’s commitment to compliance and credibility.

Examples of entities that need to check often if another company is in good standing include:

- Fintechs and banks. Both traditional financial institutions and fintech platforms require companies to be in good standing before allowing them to access commercial bank accounts. This is a standard compliance verification process that helps mitigate financial risks and minimizes the chances of fraud.

- Insurance companies. They need to assess another business’ good standing as part of their risk management strategy. Naturally, companies that are not in good standing pose bigger risks and should be assessed in a more detailed way before being accepted as a client.

- Loan service providers. Such entities need to assess another business’ financial standing and risk profile. This helps make a decision whether it’s the right choice to onboard another company that is not in good standing and approve the loan. That said, such entities have higher possibilities of facing fines or other issues, like non-compliance.

Checking if another company is in good standing is vital to avoid partnering with businesses that aren’t properly registered or lack “good standing,” as nobody wants to enter a long-term business relationship with a risky entity that could potentially bring more risks and legal violations.

Related: 6 Steps to Conduct a Know Your Business (KYB) Verification Check

How Can You Determine if a Business is in Good Standing?

You can see whether the company is in good standing by:

- Finding information through the SEC’s EDGAR system. This is possible if the business is large enough to be publicly traded.

- Checking with the Secretary of State’s office in the state where the business is operating.

- Requesting a copy of the certificate of good standing from the business itself.

However, this isn’t enough because there are other risks that you need to determine during your AML risk assessment.

For example, part of that, there are KYB processes that are designed to confirm ownership stakes in a certain company (because criminals sometimes hide behind opaque ownership structures and launder funds this way), including other processes like checking the company’s financial data and assessing if related individuals are authorized to represent the company by screening them through different AML databases. Then, the last step is your responsibility to decide if it’s safe to start a business relationship and if the company is in “good standing.”

Other steps to take when assessing whether a company is in good standing during your background check:

🟢 Search for Adverse Media

Adverse media, or negative news, refers to publicly available information gathered from various news sources to identify individuals or companies linked to crimes such as money laundering, bribery, sanctions evasion, drug trafficking, organized crime, financial fraud, tax evasion and similar offenses. This can create potential risks if you’re linked to that business. If you find a match during screening, you should assess the risk by evaluating the incident, its timing, and the business’s involvement.

While screening newspapers and analyzing thousands of articles may seem inconvenient, adverse media has proven to be an important tool in AML and an effective risk management measure. To make it more efficient, companies collect information about the business and its owners and verify these details with official sources by scanning different media outlets using methods like keyword-based techniques or third-party AI-powered solutions.

Related: What is Adverse Media Screening?

🟢 Identify Politically Exposed Persons (PEPs)

A Politically Exposed Person (PEP) is an individual with a prominent status who may be more susceptible to engaging in activities like bribery, money laundering, or corruption. PEPs often hold significant roles in international organizations or governments. Companies view PEPs as higher-risk clients because they are more likely to be involved in financial crimes, such as money laundering. Family members and close associates of PEPs also carry these risks.

So, next to assessing if the company is in good standing, you should identify and verify PEPs and determine whether you want to onboard this high-risk individual and start a business relationship with them. If a match is found, and the customer has a PEP status, you should evaluate how the person’s position could pose direct or indirect risks to your company. To put it simply, it’s not illegal to work with PEPs, but they carry risks.

That’s why adopting a risk-based approach in AML compliance enables businesses to identify and steer clear of high-risk individuals, such as PEPs, who could misuse their services. This approach means that low-risk clients typically do not require extensive checks (simplified due diligence can be applied), medium-risk clients undergo customer due diligence (CDD), and high-risk entities are subject to enhanced due diligence (EDD) measures.

Related: PEPs and Sanctions Checks Explained

🟢 Check for Bankruptcy Filings

This is also an important step because a company filing bankruptcy is a red flag. It indicates that the company may struggle to meet its financial obligations. Partnering with such a business can increase risks when it comes to debt or when attracting new business partners. This means you’re risking losing assets or severely damaging your operations. For example, if a supplier files for bankruptcy (after showing financial red flags before onboarding) in the middle of your contract, it can lead to asset liquidation. This can also disrupt the supply of critical components needed for your business to run smoothly.

In the US, bankruptcies are handled by federal courts. One of the most reliable ways to check is the Public Access to Court Electronic Records (PACER) system. For publicly traded companies, search the Securities and Exchange Commission (SEC) database. Look for 10-K or 8-K reports that disclose bankruptcy. Credit rating agencies also often include bankruptcy history in their reports. To make this process more efficient, automated solutions like iDenfy’s KYB software simplify document management by providing access to government and credit bureau reports (available for download), connecting to over 180 company registries across 120+ countries for official, real-time data.

🟢 Review the Company’s Address

A proper company in “good standing” has a legitimate physical location and a registered office space. You can review this information simply using search engines and features like Google Maps (which shows a photo of the location that you’re searching for). This helps to check if the address is accurate, up-to-date, and matches the company’s profile. Without an address, an entity might be a shell company that has no active operations. That means it exists only on paper potentially as a money laundering channel. iDenfy’s software also carries this feature and shows the location of the company address that you’re searching for.

In the context of AML compliance, both corporate (entities) and individual clients need to prove their address. To complete this step, you might have to review multiple documents like registration licenses, utility bills, residence permits, and other official records. Remember that a company might operate from multiple addresses in different countries besides its main registered HQ location. You should verify all addresses and cross-check this information using database verification measures.

How iDenfy’s Solutions Help Ensure You Work With Businesses in Good Standing

Gathering and assessing different types of documents in different jurisdictions that have inconsistent compliance requirements, languages, or, sometimes, missing registries, along with other challenges when determining if the company is in good standing — and if it’s really legitimate and worth working with — can be a complex task, especially without automation. Additionally, relying on inaccurate or unreliable databases puts you and your business at risk.

At iDenfy, we recommend you simplify KYB compliance and AML risk management processes with a single, feature-rich Business Verification platform. In one dashboard, you can enable:

- AML screening (such as PEPs and sanctions, as well as adverse media checks).

- Company detail verification (such as the address and registration number).

- Ownership structure verification (for example, verifying all directors, UBOs, etc.).

- KYC for individuals (identity verification for all individuals linked to the company).

- Automated risk assessment (client risk scoring in the same KYB dashboard).

And much more, like custom questionnaires, to personalize your onboarding process and request specific documents linked to finding out if the business is in good standing.

Feel free to contact us for a demo.