Money laundering is the process of integrating dirty money, which is illegally obtained through various methods, such as organized crime and its associated activities, and cleaning it to appear legitimate. The primary challenge with money laundering is its complexity, particularly for financial institutions responsible for monitoring transactions to prevent it. A large portion of money laundering is successful and goes undetected, often through channels like real estate, art, and other tangible assets, with some estimates suggesting that up to 50% goes unnoticed.

Like many different businesses and industries, not only financial institutions, are now strictly regulated and need to comply with the Anti-Money Laundering (AML) framework. Sophisticated schemes are used by criminals who know the techniques of how to use their dirty funds without raising suspicion. Some methods are less deceptive than others, but if illegal money is used and its true source is concealed, it’s a serious crime, and that crime is money laundering.

In this blog post, we look into how criminals succeed with money laundering, examine real-world money laundering examples, explain how AML compliance addresses the issue, and share ways to detect and prevent this crime.

What is Money Laundering?

Money laundering is an illegal process that involves criminals using their illegally obtained money and making it look “clean” and appear legitimate. That’s why the laundering part means that the “dirty” cash was cleaned, and any potential links that could trace the criminals and their true source of funds are erased. To solve this issue, global regulatory organizations have created AML laws and regulations, which require companies to implement their own internal policies and AML processes designed to stop such illegal activities.

Money laundering happens in different ways. For example, since criminals don’t want to raise suspicion, they find ways to make the money look like it came from a proper, legal source. For example, they can use other entities, aka businesses they own themselves, to launder money. That’s why a huge part of AML compliance is Know Your Business (KYB) verification, a process designed to help assess and verify other companies, determining if their operations are legitimate and compliant.

For years, only individual client verification, known as Know Your Customer (KYC), was required. However, regulators began to spot serious gaps in the system, such as the use of shell companies for money laundering. To address these risks, KYB verification was introduced. However, there are multiple risk factors that increase the chances of money laundering. For example, the use of cross-border transactions or cryptocurrencies or digital assets with a nature of anonymity also doesn’t help when it comes to money laundering.

KYC for crypto and blockchain

Stay compliant with evolving crypto regulations. iDenfy helps exchanges and DeFi platforms verify users globally.

Explore Crypto SolutionHow Does Money Laundering Work?

Money laundering is appealing to criminals because they are driven by the goal of earning more and making a profit. To make the money appear legitimate, criminals move it through financial institutions. This works because fraudsters often profit from drug trafficking or other financial crimes, and they often end up with large sums of cash.

Money laundering is based on funneling the illegally obtained money into the legitimate financial system. With this process, criminals aim to:

- Hide the origins of illicit funds so they can be used without drawing attention to the crimes behind them.

- Turn illegally obtained money into assets that appear to come from lawful sources.

Money laundering negatively impacts not only the financial institutions that are used as channels for cleaning the money but also the general financial system. It also helps terrorists, drug traffickers, and other types of criminal organizations to expand their operations and weaken the broader economy.

Three Stages of Money Laundering

Money laundering typically consists of three main stages. While these steps may sometimes overlap or repeat, they generally include:

1. Placement

It’s the first and most vulnerable stage for criminals, as it involves moving large amounts of illicit cash into the financial system without attracting attention from authorities or banks. To avoid detection, criminals often break the money into smaller, less suspicious amounts. This can include methods like depositing funds into offshore accounts or using other tactics to begin disguising the origin of the money.

Common placement techniques include:

- False invoicing, when no real goods or services are exchanged.

- Smurfing or making multiple small deposits below AML reporting limits.

- Buying high-value items like art or luxury goods to later sell for clean money.

- Moving illicit funds through foreign exchange markets, especially in less-regulated areas.

For this reason, to prevent money laundering, regulations like the Bank Secrecy Act (BSA) mandate that financial institutions maintain records of cash purchases and need to report cash transactions over the $10,000 threshold. All red flags ned to be investigated, while detected suspicious activity needs to be reported via a Suspicious Activity Report (SAR).

2. Layering

The second stage involves moving illicit money through a series of complex and often fraudulent transactions to conceal its origin. The goal is to mix the dirty funds within the financial system and erase any clear audit trail that could link the money back to illegal activities. This process of repeatedly moving and disguising the money is why it’s called “layering.”

Common layering examples include:

- Using the stock market to move illicit money.

- Investing in real estate or using shell companies to launder funds.

Applying chain-hopping to convert cryptocurrency and transfer it across different blockchains. - Mixing and tumbling transactions across multiple exchanges to obscure their origin.

3. Integration

It’s the final stage, where criminals mix illegal funds into the legitimate economy, making the money appear clean. Through integration, criminals can use their illicit funds openly, often by purchasing luxury goods or investing in legal businesses. They may pay taxes and accept financial losses to avoid raising suspicion with tax authorities and law enforcement.

This stage blurs the line between illegal money and legitimate wealth, allowing criminals to use their funds freely. Often, they reinvest laundered money by buying businesses and generating legitimate income, which helps continue the laundering cycle.

Related: 3 Stages of Money Laundering Explained

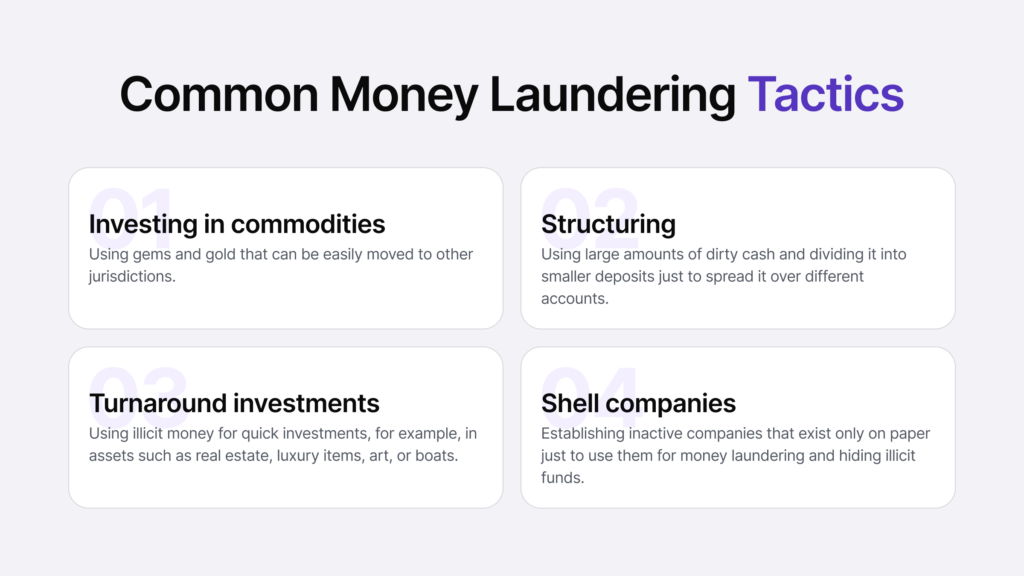

Common Types of Money Laundering

There are various money laundering types, but they can be grouped into four main categories: smurfing (also known as structuring), using banking methods, currency exchanges, and double invoicing. Since new technologies constantly develop, money launderers also adapt, making it harder for companies or AML analysts to detect suspicious transactions.

Here are the most common money laundering types in more detail:

- Smurfing. This involves breaking large sums of illegally obtained money into smaller transactions across multiple different accounts below reporting thresholds to avoid getting flagged.

- Gambling. Money laundering occurs in both physical and online casinos. Usually, a fraudster buys chips or credits with dirty money, plays through some wins and losses, then cashes out and cleans the illicit funds.

- Tax havens. Using specific jurisdictions that are known to have less stringent AML rules, perfect for criminals seeking to evade or minimize taxes, or worse, launder illicit funds.

- Trade-based laundering. This involves misreporting the value of goods on purpose, for example, by under-invoicing or falsifying shipment quantities to hide dirty money.

- Cash-intensive businesses. This happens when criminals invest in businesses that are based mostly on cash, such as vending machines, and can be both a form of passive income and a source to mix into the legitimate financial system.

Once the money appears clean, criminals can use it freely. This blurs the line between illegal funds and legitimate wealth. But criminals rarely stop here; they often repeat their tactics, continuing the cycle by reinvesting the funds by buying businesses and generating legitimate income through salaries to keep laundering money.

Related: Examples of Money Laundering and Prevention Methods

What is Electronic Money Laundering?

Electronic money laundering refers to the use of digital platforms and online transactions, such as online banking and financial services, to move and conceal illegally obtained funds.

For example, electronic channels like peer-to-peer (P2P) mobile transfers, crypto and digital assets, or other payment services have made money laundering easier for some criminals.

Additionally, criminals use extra tools that hide their identities and can make it more complex for internal Trust and Safety teams to detect fraud. For example, proxies that hide the user’s IP address can be used for fraud, including money laundering, as a way to obscure internet activity, making the integration stage of money laundering difficult to trace. However, the same principle applies to various use cases. For instance, an online casino gaming site can be used for money laundering by using dirty cash, buying gaming currency, then converting it back into untraceable, clean funds.

So, while not all digital currencies are completely anonymous, cryptocurrencies like Bitcoin are still widely used in criminal activities, including money laundering linked to drug trafficking and other illegal operations. Their relative privacy and ease of transfer make them attractive tools for hiding illicit funds.

What is Anti-Money Laundering (AML)?

Anti-money laundering (AML) is a series of legal frameworks, regulations, and procedures designed to detect and expose illicit funds that are disguised as legitimate earnings. Its primary goal is to combat money laundering and other financial crimes committed by criminal or terrorist organizations around the world.

AML is governed by regulations at both national and international levels, compelling entities within the financial industry, such as banks, fintech companies, and insurers, to establish internal procedures and controls while reporting suspicious activity to relevant authorities. Some industries, like cryptocurrency, as discussed earlier, are more prone to such crimes, which means all platforms operating in this sector need to verify their customers and conduct transaction monitoring after the initial onboarding process.

To stay compliant, regulated companies need to have a solid AML framework that includes:

- Verifying customers and business partners using KYC procedures.

- Screening individuals and entities against sanctions lists using automated AML tools.

- Identifying the true beneficial owners of legal entities through proper due diligence measures, with stricter checks for higher-risk cases.

- Monitoring transactions and customer behavior to spot and report suspicious activity.

- Keeping accurate records of customer identities and financial transactions.

AML Laws and Money Laundering Prevention

Here are some key laws and institutions that play a major role in defining AML compliance and combating money laundering activities:

The Bank Secrecy Act (BSA)

Enacted in 1970, the BSA, also known as the Currency and Foreign Transaction Reporting Act, was the first US law specifically designed to combat money laundering through banks and financial institutions. It requires banks to assist government investigations by monitoring customer transactions. Under the BSA, any cash transaction over $10,000 must be reported via a Currency Transaction Report (CTR).

The Patriot Act

Introduced after the 9/11 attacks, the Patriot Act aims to detect and prevent terrorism, both domestically and abroad. It strengthened collaboration between financial institutions and government agencies and increased penalties for money laundering. A key component is the requirement for Customer Identification Programs (CIPs), which obligate institutions to verify the identities of their clients through KYC verification processes.

Financial Crimes Enforcement Network (FinCEN)

Operating under the US Department of the Treasury, FinCEN collects and analyzes financial transaction data to combat money laundering, terrorist financing, and other financial crimes. It enforces customer due diligence rules for financial institutions and helps strengthen the regulatory framework established by the BSA.

The Financial Action Task Force (FATF)

The FATF is an intergovernmental body that also sets global standards to combat financial crimes, including money laundering and terrorist financing. One of its milestones is recognizing virtual assets (VAs) (or digital currencies) as a risk to financial integrity. This led to the FATF issuing guidance for applying a risk-based approach to AML, especially targeting VAs and virtual asset service providers (VASPs).

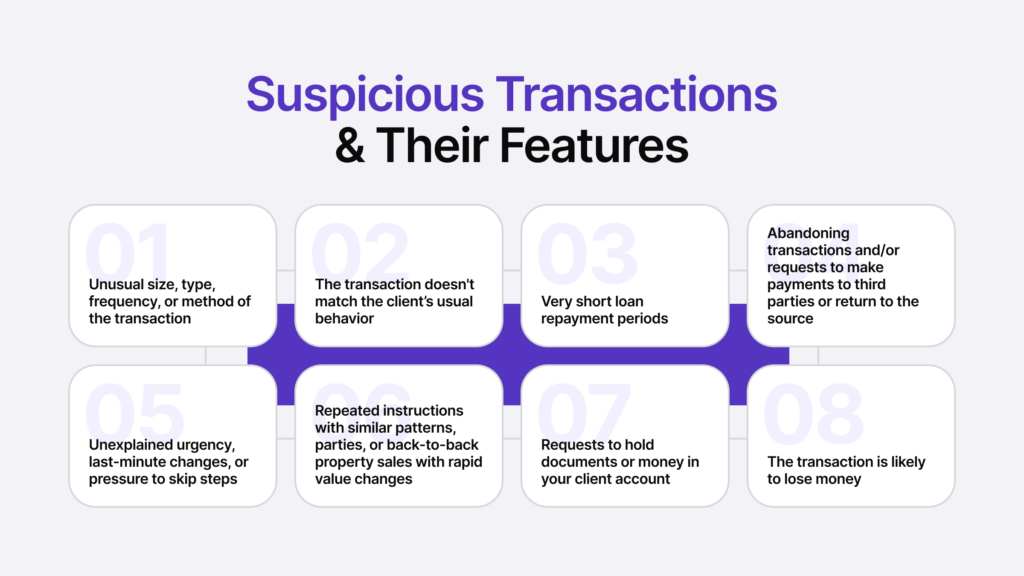

What are Money Laundering Red Flags?

Money laundering red flags, also called AML red flags, are warning signs that may indicate money laundering or other illicit financial activity. These can include unusual customer behavior, suspicious sources of funds, or sudden transactions that don’t match a customer’s typical profile. Identifying these signs helps businesses and financial institutions detect and investigate potential financial crimes. In general, criminals who attempt to launder money often engage in activities that deviate from normal customer behavior.

For example, it might be a person making the transaction who isn’t an official representative or party, or the bank notices multiple transactions between the same parties in a short period. Also, classic signs are third parties or intermediaries that are based in high-risk jurisdictions without a clear reason. When it comes to business ownership, it could be a listed director or representative who is underqualified and doesn’t appear appropriate for their role. It means the true owners behind the financial crime are hiding their identities.

Other red flags include large cash payments, unexplained third-party involvement, concealing ownership to obscure the origin of assets, frequent use of multiple accounts, setting up or managing nonprofits that may serve as fronts for laundering criminal proceeds, and transactions involving foreign bank accounts or virtual wallets from various jurisdictions.

How to Prevent Money Laundering?

It’s impossible to control criminals and their actions, including completely eliminating the issue of money laundering. However, standard steps, such as verifying all clients and business partners using a proper AML program, help prevent financial crimes and being used as a money laundering channel. Most businesses that get tangled up in such schemes and need to pay legal fines are being used unknowingly. For this reason, constant screening, staff training, and monitoring internal controls to see if they work are needed.

Companies should also know which behaviors or types of transactions need to be treated with extra caution and additional due diligence measures. Complex business structures or challenges in identifying the true owner of an entity or purchases of high-value items like art, jewelry, or luxury goods need to be reviewed and monitored according to the company’s internal risk appetite. This is why regulatory authorities stress the importance of the risk-based approach to AML. When onboarding customers, automated identity verification solutions, such as iDenfy’s, are beneficial.

For example, fintech companies can prevent fraud and money laundering by implementing a more stringent KYC flow. This includes requesting the user to upload their government-issued ID photo and complete a biometric check. Sometimes, database verification is also used, where the user’s personal information is cross-checked against another government database to find potential matches.

Additionally, the institution often needs to screen the client against AML databases, such as PEPs & sanctions, global watchlist, and adverse media. For instance, a PEP, or a Politically Exposed Person, is always a high-risk customer, which means they need to be inspected more carefully than a low-risk customer without any potential links to financial crime. Screening negative news also helps detect ties to money laundering and other crimes, which should not be tolerated when forming new business relationships in certain industries.

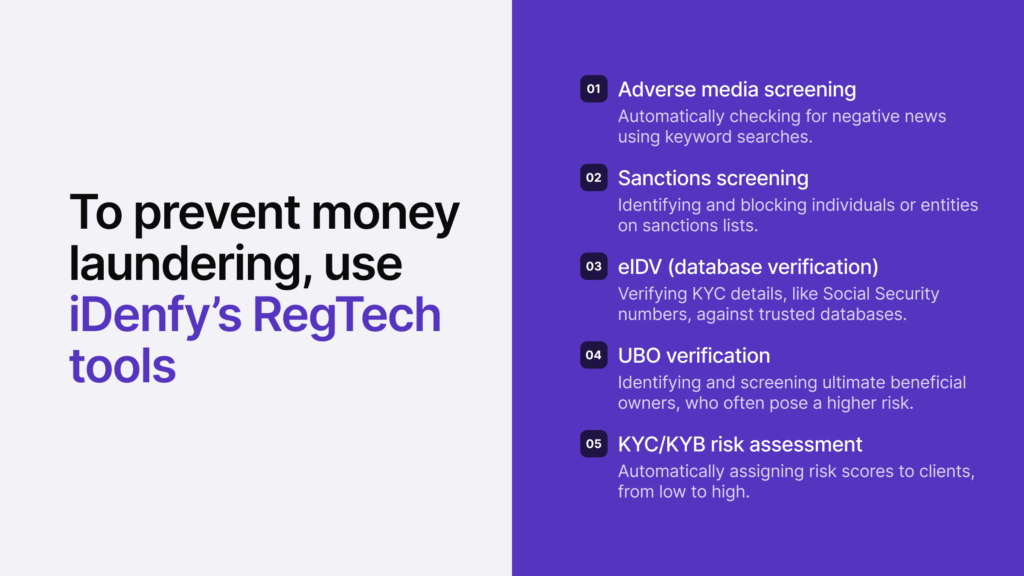

At iDenfy, we help companies prevent money laundering and other financial crimes with our complete compliance and fraud prevention platform. Our AML toolkit includes services like:

- Identity verification (document and biometrics)

- Business verification (including features like EIN verification, AI data cross-matching & more)

- AML screening (PEP screening, sanctions screening & watchlist screening)

- Adverse media checks

- Bank verification (available in the EU)

- Other due diligence measures, such as address verification (like automated utility bill verification)

- Other fraud prevention solutions, such as phone or email verification (to collect extra information about the customer)

Book a free dashboard tour to see any of the mentioned solutions in action.