With each passing year, there is a significant rise in identity fraud. Identity fraud makes up a major part of online crime that involves different levels of impersonation or fake portrayal. As the number of frauds increases, so do the victims. And if there are victims, that means there are fraudsters as well. These fraudsters broadly commit three types of fraud: first-party, second-party, and third-party fraud.

Irrespective of the fraud these perpetrators commit, their ulterior motive is to steal resources, whether it’s data or money. Let’s jump right into it and explore all about first-party, second-party, and third-party fraud.

Book a Meeting on How to Protect Your Business From Fraud with Identity Verification

Hiding Their True Intentions

All fraudsters work to hide their true intentions from their targets. The process involves creating a trustworthy and believable front. To successfully steal something from someone, they must convince others that they are genuine people with real intentions. They start by creating a digital footprint that does not raise any flags like minimal defaults, positive credit history, steady incomes, etc.

Impersonating Someone

To impersonate someone and steal their information, fraudsters need to gain the target’s personal data illegally. They need as much truthful information about a person as possible to create a robust digital footprint. It allows them to commit the crime and disappear without a trace. Merely knowing your name is not enough. Fraudsters search for your house and email address, contact number, date of birth, social security number, etc., to have a higher chance of succeeding.

PII Data Theft

All the above information about a person falls under the PII or Personally Identifiable Information category. The criminal minds obtain PII using illegal methods like phishing, data breaches, and web scraping. PII data theft is a significant fraud network where criminals use stolen data to execute different cybercrimes.

Depending on what identity fraud they execute, the frauds belong to three categories:

- First-party fraud

- Second-party fraud

- Third-party fraud

The motive behind these frauds is common, but their way of execution varies. We explain each fraud type in more detail below:

First-Party Fraud

First-party fraud is a common and widespread issue. It involves a person or a group falsely identifying themselves or providing incorrect information. The person mostly does this while applying for a loan or credit, and they do so to get better rates. There are even instances of people committing first-party fraud for false insurance claims to get a payment.

For example, a person can commit first-party fraud to qualify for a mortgage. They lie about their current employment status. Sometimes, people also alter personal details to get an insurance policy. Some people also lie about a big purchase on their credit card when the bank calls them to check if it is them. They deny making any such purchase to get a refund while the retailer pays the chargeback.

Here are other common first-party fraud examples:

- De-shopping involves purchasing items, like clothes, to use them before returning them for a full refund.

- Fronting involves setting up a service in another person’s name to cut costs, like a young driver getting cheaper car insurance by applying under a parent’s name.

- Address Fronting entails using a different risk address, either owned by the individual or unrelated, to lower service costs, such as getting car insurance for a holiday home instead of a main residential address.

Learn More About Automated Fraud Prevention Tools

Second-Party Fraud

Second-party fraud is much more complicated than first-party fraud. This type of fraud involves an individual agreeing to give their personal information to a family member or a close friend to commit the fraud. Their friend will use the information to order products or services through a new device not linked to the account. It makes the whole fraud look legitimate and makes it difficult for banks to show if the customer willingly participated. Second-party fraud is sometimes called friendly fraud.

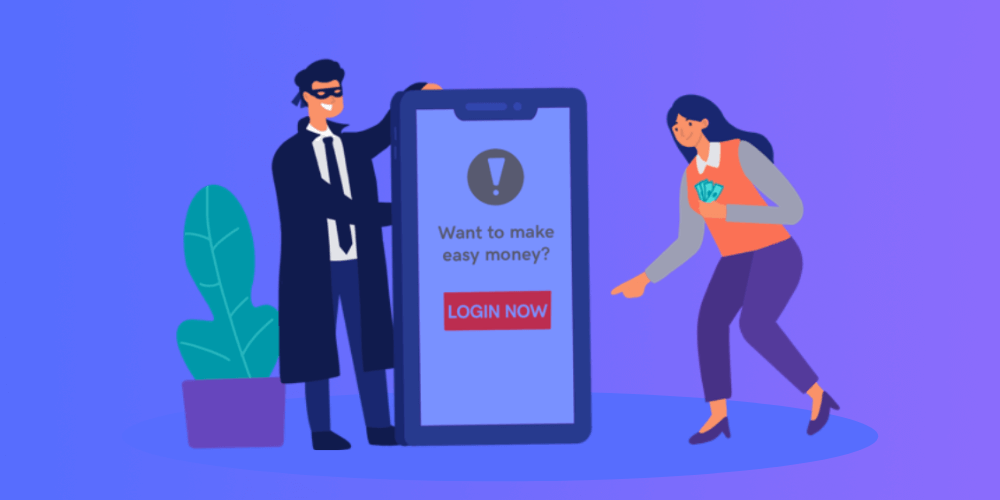

Cunning fraudsters have even found a way to participate in second-party fraud. They entice innocent customers with quick money-making schemes. When the customer experiences to gain the amount, they consent to accept and transfer funds to and from their bank account in the second party’s interest.

The whole process is precisely money laundering, and the customers who transfer the amount are called money mules. Since the people who transfer the amount are real with truthful information, it is challenging to detect such fraud. For example, supermarkets sometimes have signs that say, “Want to make easy money?” Anyone with a monetary problem could easily fall into this trap. Once they agree to participate, fraudsters use their information to commit fraud.

What customers can do to prevent second-party fraud:

- Conduct thorough research on job offers or promotions. If a deal seems too good to be true, it likely is.

- Refrain from agreeing to any request involving transferring money through, into, or out of their bank account.

- Decline offers that require them to establish a new company or LLC in their name as a condition for employment or receiving a prize.

- Never agree to let someone else use their bank account for receiving and forwarding money, regardless of their promises.

Third-Party Fraud

Third-party fraud is the most popular among all the three fraud types. It involves fraudsters using an innocent person’s identity and information to take over their bank account without their consent. Third-party fraud also includes a fraudster creating a new identity from stolen and faulty information.

This fraud type is often linked to organized criminal rackets. According to iDenfy’s estimates, nearly 50% of third-party fraud is part of some fraud ring within the fraud related to numerous identities. The fraudsters acquire PII and use it to hijack accounts to buy products, services, or credits. Currently, third-party fraud is booming, as mobile banking and many fintech companies have unlocked the door for various vulnerabilities.

Here are some examples of the most popular third-party fraud types:

- Account takeover or ATO fraud is the most common example of third-party fraud. The fraudsters take over a victim’s account through their PII, which they have either hacked or obtained through some method like phishing.

- Another example of third-party fraud is loan stacking. In this case, a fraudster applies for several loans at once using someone’s identity and never pays back.

Related: Top 5 Marketplace Fraud Examples You Should Know

Concluding Point

When it comes to curbing first-party, second-party, and third-party fraud, the challenge is immense, as the perpetrators are not just criminal organizations but also loyal customers. It makes it challenging to develop a single solution that is effectively applicable to all three fraud types. With technological advancements, fraudsters have better tactics and tools to impersonate someone, commit a crime, and then cover their tracks. In a virtual world, it is nearly impossible to authenticate an account without context.

But banks and other industry players have one way to avoid such fraud. Many companies are using third-party RegTech solutions or are developing ID verification tools using AI. Such verification methods help companies check if a customer’s documents are genuine and if they’re a real person. In today’s context, where tools like ChatGPT are easily accessed and used for the wrong reasons or where deepfakes can’t be assessed with a human eye anymore, picking out a robust KYC solution for customer onboarding is vital.

At iDenfy, we build a complete KYC/KYB/AML fraud prevention hub with all the needed tools in one place, including AI-powered identity verification, AML screening, Business Verification for corporate customers, and much more.

Book your free demo today and protect your business from first-party, second-party, and third-party fraud.

This blog post was updated on the 15th of December, 2023, to reflect the latest insights.