Customer due diligence (CDD) enables businesses to assess the risk of engaging in a business relationship and helps prevent fraud, money laundering, and other illicit practices. In simple terms, CDD solutions confirm a client’s identity and evaluate the risks they may pose to the business.

Customer due diligence checks help companies verify customers and assess their risk profiles. For example, financial institutions must conduct due diligence before granting them access to open an account. This way, companies can make better decisions and protect themselves from legal penalties and financial losses.

Interesting notes to remember:

- Investing in reliable customer due diligence solutions is essential to building a secure and trustworthy business environment.

- CDD helps safeguard organizations and builds credibility by helping foster long-term relationships with clients.

- By effectively managing risks and conducting CDD, businesses can attract new customers, retain existing ones, and gain a competitive edge in the market.

But the biggest challenge for companies is to continue the CDD processes after they onboard their customers. Companies must consistently evaluate the risk level posed by each customer. Organizations use customer due diligence solutions and their benefits to achieve this goal.

In this article, we go deeper into customer due diligence and share tips on how to check and verify the identity and background of potential business clients and customers through automated solutions.

What is Customer Due Diligence in the context of KYC/AML?

Customer due diligence is a legal requirement for organizations establishing business relationships with customers. CDD is also part of Know Your Customer (KYC) and Anti-Money Laundering (AML) compliance directives:

- KYC collects comprehensive customer information to establish their identity and evaluate their suitability for business relationships. KYC refers to customer identification, which is part of AML compliance designed to confirm a customer’s identity.

- AML aims to prevent illegal activities like money laundering and terrorist financing. AML compliance unites many processes to prevent money laundering, including verifying customers’ identities or monitoring transactions for suspicious activity.

That’s why CDD, KYC, and AML are all connected processes that help businesses know and understand their customers better.

What Steps Does the CDD Process Include?

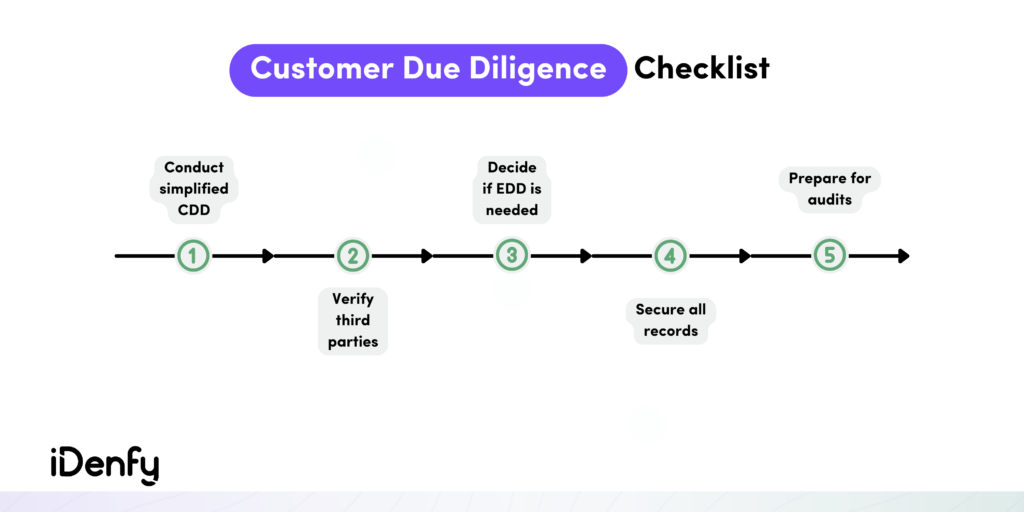

Customer due diligence is a dynamic process. Consequently, it’s not enough to verify customers’ identities during onboarding. There are certain steps and elements that companies must establish. For example, all data must be stored and updated so regulators can access it easily for audits.

Banks and financial institutions should use customer due diligence solutions and include these steps in their CDD process:

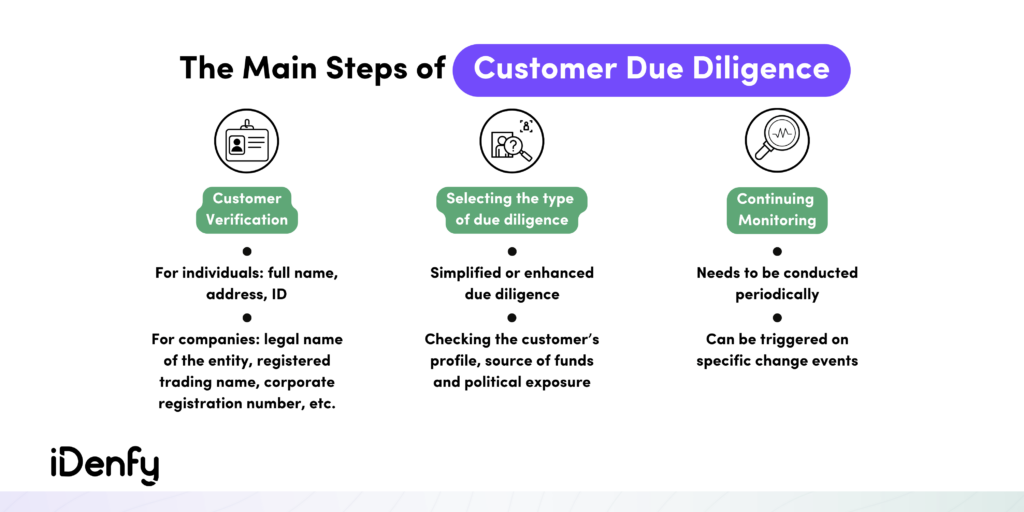

1. Identity Establishment

Prior to initiating any business relationship, the bank or financial institution in question verifies the identity and business activities of potential customers. This entails collecting and verifying the customer’s information. To simplify this element, many companies use automated identity verification software that enables efficient document checks.

2. Customer Risk Level Classification

After confirming the customer’s identity, the company assesses and classifies the level of risk associated with that customer’s relationship and the business. Companies must also securely store this information in a digital location that provides convenient access during regulatory audits.

3. Choosing the Level of Due Diligence

Once the company verifies the customer’s identity and assesses their risk level, they need to decide which type of due diligence checks is most suitable: simplified due diligence, customer due diligence, or enhanced due diligence (EDD).

Risk-Based Customer Due Diligence Assessment

The level of due diligence depends on the customer’s risk profile and relationship with the organization. As part of gathering and verifying identity information, the company can establish customer risk profiles. They guide the extent of CDD that needs to be conducted.

Customers categorized as low-risk generally require basic CDD measures and less frequent monitoring. Conversely, customers identified as high-risk will require EDD, involving closer examination of financial transactions and more frequent monitoring.

What Data Should be Analyzed During CDD Checks?

Customer due diligence involves collecting and analyzing information from various data sources to determine the customer’s identity and risk profile. This includes examining the customer’s personal information (name, address, photo of their ID), their activities and the markets they operate in, and their business relationships with other entities.

Financial institutions must also collect data from private and public sources, including the following:

- Basic identity information provided by the customer

- Public data sources, for example, company listings

- Private data sources from third-party providers

- Sanctions lists, mostly published by governments

The Four Customer Due Diligence Requirements

FinCEN established the Final CDD Rule requiring companies to create policies and maintain transparency by:

- Establishing and verifying customer identities.

- Establishing and verifying company beneficial ownership.

- Understanding the nature and purpose of customer relationships and documenting risk assessments to build customer risk profiles.

- Conducting ongoing monitoring to detect and report suspicious activity while keeping all customer data up-to-date.

Customer Due Diligence for Banks

CDD applies across the financial industry. That means all financial institutions must take a risk-based approach to customer due diligence, depending on the type of business relationship and the customer’s risk profile.

Banks can use automated CDD solutions to ensure they remain compliant with local laws and operating market regulations. In general, they must take steps to verify their customers and the entities they are working with to prevent fraudulent activities, such as impersonation or identity fraud.

CDD Stages in Banking

Banks and other financial institutions must apply customer due diligence in certain situations. This helps ensure compliance and prevent fraud in the following business relationship stages:

- When establishing a new business relationship. Banks must conduct CDD checks to assess the customer’s risk profile and verify their identity to prevent working with fraudulent entities.

- During certain transactions. Some transactions are more risky than others and require additional CDD measures. For example, if the transaction involves large sums or the customer is from a high-risk region with high money laundering rates.

- In case of suspicious activity. Banks must apply CDD if the customer shows any red flags and signs of money laundering or terrorism financing.

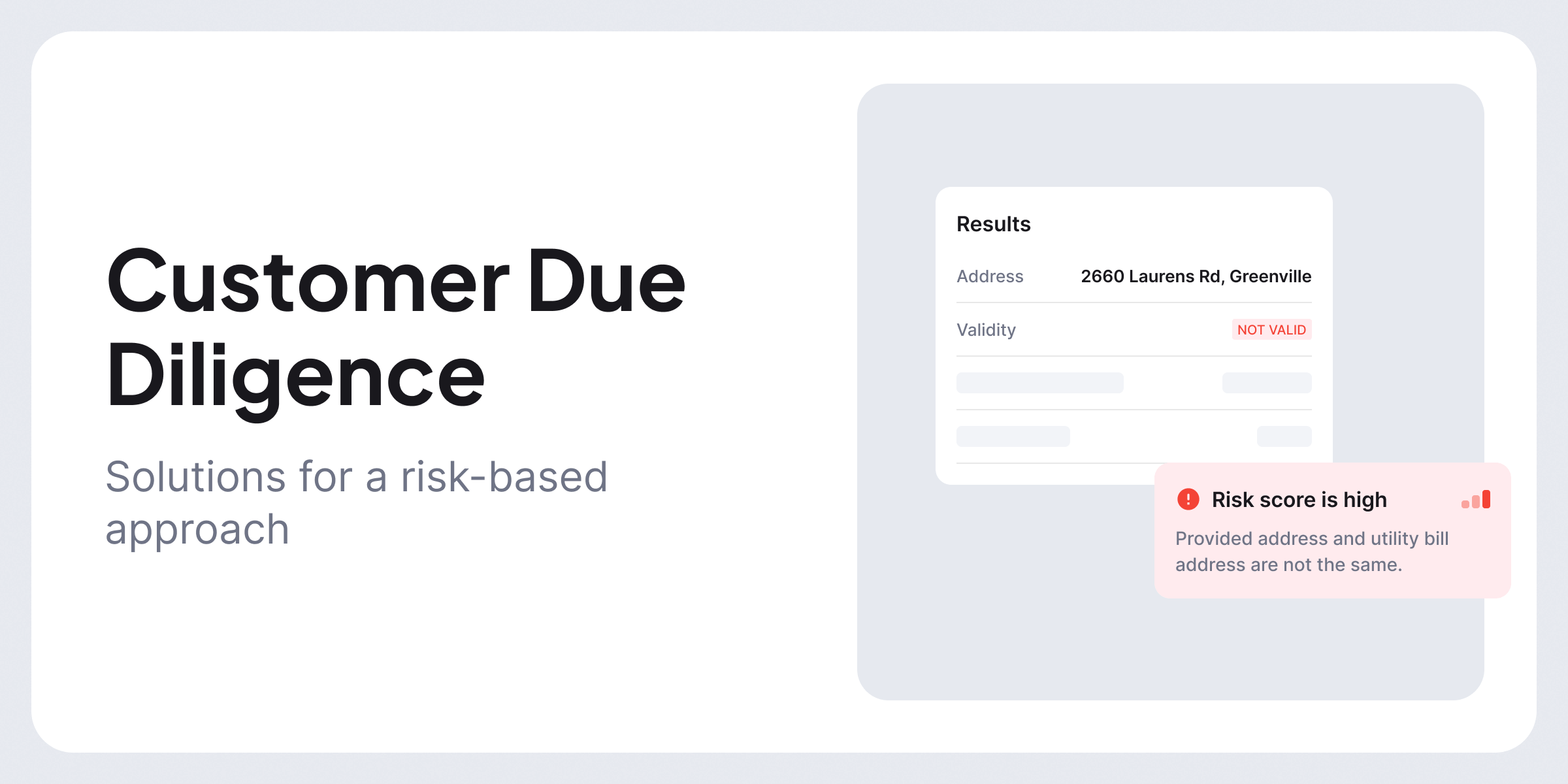

- If the customer’s data doesn’t match. If the identification data the customer provided doesn’t meet requirements or is suspicious, banks must conduct additional CDD checks.

Customer Due Diligence Process Challenges

AI advancements in the finance industry, regulatory reforms, constantly evolving sanctions, stricter penalties for non-compliance, and smarter tactics from criminals increase the pressure on specialists. That’s why compliance teams struggle to handle large amounts of data and face numerous challenges during the CDD process.

Key challenges businesses face when conducting CDD/AML procedures manually:

- Time-consuming and labor-intensive work. Manual CDD processes require significant time and effort. The manual collection, verification, and analysis of customer information and documentation can be time-consuming. This leads to delays in customer onboarding and negatively impacts the customer experience.

- Higher risk of human error. Manual CDD processes are prone to human errors, including data entry mistakes, overlooking critical information, missing compliance updates, or failing to detect suspicious patterns. These errors can have serious consequences, such as missed red flags or false negatives, compromising the effectiveness of the CDD.

- Limited scalability and efficiency. Compliance officers can struggle to handle large volumes of customer data efficiently. As businesses grow and customer bases expand, managing the increasing workload manually can be challenging, leading to decreased scalability for the company.

In fact, the risks associated with insufficient CDD processes, as well as regulatory non-compliance, have become so significant that traditional manual processes for customer verification and monitoring are often insufficient in addressing these challenges.

Automated Customer Due Diligence Solutions

To overcome these challenges and keep in line with the evolution of finance, companies are integrating automated solutions into customer due diligence programs. These solutions simplify the work for compliance officers through automation, helping to complete the CDD process.

Here are some examples:

- Identity verification. Automated identity verification solutions scan and extract data from ID documents in seconds, making the onboarding process for the customer simple and efficient. Facial recognition and liveness detection technology detect fraudsters who try to pass the verification using masks. These systems also compare ID documents against trusted databases and flag potential discrepancies.

- Customer risk scoring solution. AI-powered systems can analyze customer data and assign risk profiles. This helps companies assess the level of due diligence required for each customer. With this CDD solution, you can effectively eliminate obstacles from the process while ensuring that you fulfill your compliance obligations.

- AML monitoring software. This type of monitoring software typically consists of tools that can scan customer information against sanctions lists, global watchlists, and politically exposed person (PEP) databases in real-time, continuously. They generate alerts if a customer matches any suspicious profiles and inform the analyst using the solution about the next steps. Often, AML monitoring software is vital for high-risk, suspicious clients who need extra due diligence checks and need to be reviewed constantly.

- Ongoing monitoring. Automated transaction monitoring software analyzes customer behavior patterns, applying predefined rules and AI algorithms to detect unusual activities. These systems generate real-time alerts if further investigation or another due diligence level is needed.

How iDenfy Helps Conduct CDD Checks and Ensure KYC/AML Compliance

The primary approach to CDD must allow you to collect and verify basic info about your customer. Including their name, date of birth, and photograph of an official document that confirms their identity and residential address.

At iDenfy, we collect, verify and help you keep data records in compliance with CDD, AML, and KYC regulatory requirements.

We offer not only fully automated identity verification but also offer multiple solutions to layer CDD checks without disrupting the experience for the end user — tailored to any industry, including crypto, fintech, streaming, gaming, and more.

Get started today, or contact us to learn more about how to simplify compliance and ensure a frictionless onboarding experience for your customers.