Last updated: July 2026.

Crypto exchanges, NFT marketplaces, and Web3 platforms are legal targets for financial regulators worldwide — and the compliance burden keeps growing. This guide covers what KYC means in a blockchain context, what the actual fraud risks look like, and how automated identity verification changes the equation for crypto companies of any size.

Governments classify blockchain and crypto service providers as Virtual Asset Service Providers (VASPs) and hold them to the same Anti-Money Laundering (AML) standards that apply to banks. That means KYC — Know Your Customer — is not optional. It is a legal obligation, and getting it wrong has real consequences: regulatory fines, criminal exposure, and reputational damage that shuts platforms down.

The fraud numbers make the stakes concrete. In 2021 alone, cryptocurrency scammers obtained $14 billion — and that figure only counts what was traceable. The same year, 95% of spot trading volume reported on major market data sites was later identified as fabricated, according to Bitwise research. Meanwhile, 58% of NFT trades in 2022 were classified as wash trading. KYC doesn’t eliminate these risks entirely, but it removes the layer of anonymity that makes large-scale fraud viable in the first place.

TL;DR: Crypto exchanges, NFT platforms, and Web3 services are classified as Virtual Asset Service Providers under global financial regulations — which makes KYC and AML legally mandatory, not optional. In 2021, crypto scammers took $14 billion. Wash trading made up 58% of all NFT trades in 2022. Only 1 in 10 NFT investors has never experienced fraud. Without identity verification, platforms become infrastructure for money laundering — as Bitzlato ($700M) and Tornado Cash ($7B) proved. Automated KYC verifies customers in under 30 seconds and blocks bad actors before they get in.

Jump to a section:

- What Is KYC in Blockchain?

- Customer Due Diligence in Crypto

- The Three Core KYC Processes

- What Is AML in Blockchain?

- The Fraud Landscape — Crypto and NFT

- Non-Compliance Costs — Real Cases

- Why Crypto Companies Need KYC

- How Major Exchanges Approach KYC

- Manual vs. Automated KYC

- Future Trends

- The Bottom Line

What Is KYC in Blockchain?

KYC in blockchain is the same process it is anywhere else — verifying who a customer is before allowing them to transact — applied to a technology that was originally built to make that verification optional. Crypto exchanges, NFT marketplaces, and digital finance platforms built on blockchain are now required by regulators across the EU, US, UK, and most major financial jurisdictions to verify user identities. iDenfy’s identity verification for crypto is built specifically for this regulatory environment.

The driver isn’t only regulatory pressure. Blockchain’s pseudonymity — where users are identified by a wallet address rather than a name — is exactly what makes it attractive to money launderers, sanction evaders, and fraud actors. KYC replaces that pseudonymity with a verified identity, which changes the risk calculus for anyone trying to misuse the platform.

Three things to understand about KYC in blockchain:

- KYC is the get-to-know-your-client procedure blockchain financial services conduct before allowing potential users to transact on the platform.

- KYC is not a bypass option — regulated crypto platforms have no legal basis to skip it for users who meet certain volume or transaction thresholds.

- KYC in blockchain requires Customer Due Diligence (CDD) — the process of verifying identity and assessing risk before onboarding.

KYC for crypto and blockchain

Stay compliant with evolving crypto regulations. iDenfy helps exchanges and DeFi platforms verify users globally.

Explore Crypto SolutionWhat Is Customer Due Diligence in Crypto?

Customer Due Diligence (CDD) is how crypto companies — and banks, and every other regulated financial institution — establish that a user is who they say they are, and that dealing with them doesn’t create regulatory or fraud risk. It covers three things: verifying identity, assessing risk profile, and monitoring activity over time.

At the identity verification stage, the standard data points collected are:

- Full name

- Date of birth

- Email address

- Phone number

- Country and residential address

- Government-issued identification document

- OTP validation for contact verification

Some jurisdictions go further. The Travel Rule — first applied to traditional wire transfers by FinCEN in 2019 — now extends to crypto. It requires financial companies and VASPs to collect and share information about both originators and beneficiaries on transactions above set thresholds. The principle is similar to the Bank Secrecy Act in the US, which mandates data sharing for transfers of $3,000 or more. Crypto transactions above equivalent thresholds now carry the same obligation.

Related: How Identity Verification Is Helping Combat Cryptocurrency Crimes

The Three Core KYC Processes

KYC compliance in crypto runs through three distinct processes. Each serves a different function — and gaps in any one of them create compliance exposure.

1. Customer Identification Program (CIP)

CIP is the first gate. It’s where a platform collects and verifies the essential identity data from new users: document verification, address verification, face recognition, and risk scoring. Larger platforms operating in multiple jurisdictions will layer additional requirements on top — typically driven by the local regulatory framework of the markets they serve.

Related: What Is a Customer Identification Program (CIP)?

2. Customer Due Diligence

Standard CDD covers most users. But when signals suggest elevated risk — unusually large transactions, activity from high-risk jurisdictions, ownership structures that obscure beneficial ownership — Enhanced Due Diligence (EDD) kicks in. EDD demands additional verification steps, deeper source-of-funds documentation, and in some cases ongoing reporting. Crypto platforms that skip EDD on high-risk users don’t just face fines; they risk being used as a vehicle for the exact activity CDD is designed to prevent.

3. Continuous Monitoring

A clean onboarding result doesn’t mean a user stays clean. Sanctions lists update daily. Politically exposed persons (PEPs) change status. Transaction patterns evolve. Continuous monitoring keeps a platform’s risk picture current — a user who passed onboarding two years ago can be re-flagged when their circumstances change. This is where a lot of platforms fall short: onboarding is automated, but post-onboarding monitoring still runs manually, or on a quarterly batch schedule that misses same-day designation changes.

Related: What Is Ongoing Monitoring?

What Is AML in Blockchain?

AML in blockchain refers to the controls that ensure transactions on a platform are legal and traceable. Blockchain’s structure creates an inherent tension with AML requirements — transactions are recorded on a public ledger, but wallet addresses are pseudonymous, not anonymous. That distinction matters. Blockchain activity can be traced, but tracing it requires linking wallet addresses to real-world identities — which is exactly what KYC provides. See the full list of AML databases iDenfy screens against.

Effective AML on a crypto platform combines transaction monitoring with a risk-based approach: not every transaction gets the same scrutiny, but high-value transfers, unusual patterns, and activity from flagged jurisdictions trigger deeper review. Without verified identities at the foundation, transaction monitoring has no anchor — you can see that something suspicious happened, but you can’t determine whose account is responsible. For DeFi platforms specifically, the compliance picture is explored in detail in DEXs and KYC.

The Fraud Landscape — What Crypto and NFT Platforms Are Actually Up Against

The fraud numbers in this space are not theoretical. They reflect real losses, real victims, and real enforcement actions. Understanding what’s happening makes it easier to see why regulators are pushing harder on KYC requirements — and why the argument for lighter-touch compliance doesn’t hold up against the data.

Crypto Fraud at Scale

In 2021, cryptocurrency scammers obtained $14 billion. That figure covers traceable losses; the actual total is higher. According to Bitwise research from 2019, 95% of spot trading volume reported on major crypto market data platforms was fabricated — a figure that points to the scale of wash trading and market manipulation that persists when identity requirements are absent. Of 46% of finance apps now built on Web3 technology, a substantial share operate with minimal KYC. That’s where the exposure lives.

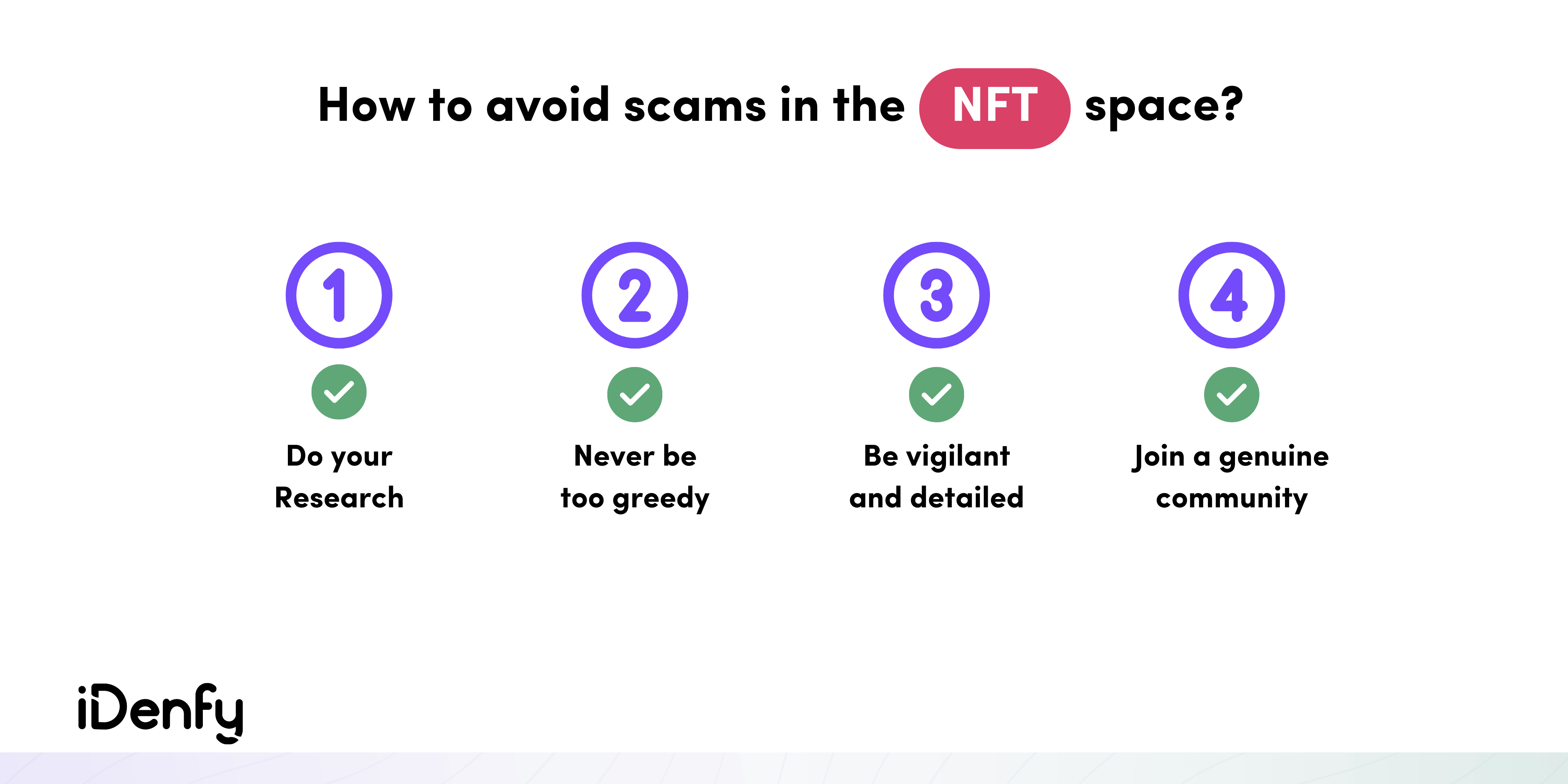

NFT-Specific Fraud Types

NFT platforms have their own fraud taxonomy. A PrivacyHQ survey of 1,008 US NFT investors found that only 1 in 10 had never experienced fraud — and fewer than 50% felt their NFT holdings were secure. The dominant fraud types on NFT platforms are:

- Rugpull scams. A team builds hype during the mint phase, collects funds, then deletes all social accounts and shuts the website. Examples include Frosties-NFT and Trollz, where investors were left holding worthless tokens after the creators disappeared with the proceeds.

- Phishing attacks. Counterfeit links mimicking wallet interfaces or marketplaces redirect users to fraudulent sites that capture credentials or drain wallets. In February 2022, OpenSea was targeted in a phishing campaign that affected 17+ users and resulted in losses of millions of dollars.

- Fake NFTs and bidding manipulation. Stolen artwork is minted as NFTs and listed for sale. In bidding schemes, scammers accept offers then pay a lower amount than the agreed bid — exploiting the lack of identity verification on buyer and seller alike.

- Wash trading. Investors sell assets to themselves through multiple wallets to generate artificial volume and price signals. In 2022, 58% of NFT trades were classified as wash trading — a manipulation that’s far harder to sustain when every wallet maps to a verified identity. See how synthetic identity fraud enables these schemes at scale.

- Ponzi schemes. Projects promise unrealistic returns, use later investors’ funds to pay earlier ones, and collapse once new investment dries up. These require anonymous entry to work at scale.

FATF guidance already identifies NFT platforms that serve as financial instruments or stores of value as falling within the VASP definition — subject to the same AML and KYC requirements as crypto exchanges. The regulatory direction is clear: KYC is coming to NFT platforms whether they plan for it or not.

Non-Compliance Has Real Costs — Recent Cases

These are not hypothetical enforcement scenarios. They are documented outcomes from platforms that treated KYC as optional.

The Bitzlato Case

Bitzlato‘s deficient KYC procedures permitted the processing of $700 million in illicit transactions. The weak identity controls created an open path for criminals laundering proceeds from drug sales and ransomware attacks — activity that stronger verification would have flagged or blocked at onboarding.

The Tornado Cash Case

In 2022, Tornado Cash was sanctioned by the US government after facilitating the laundering of over $7 billion in virtual currencies — including funds linked to North Korean state-sponsored hackers. The service’s design was explicitly non-KYC. That design choice became the basis for sanctions that effectively shut the platform down and resulted in criminal charges against its founders.

Why Crypto Companies Need KYC

In Europe, VASPs are required to comply with the Anti-Money Laundering Directives — AMLD5 and AMLD6. In the US, FinCEN has clarified that virtual currencies and the platforms that trade them are subject to BSA anti-money laundering obligations. Both frameworks require KYC. There is no jurisdiction where a regulated crypto platform can legally serve users without verifying their identities.

Beyond the legal obligation, KYC protects the platform itself. Here’s what it delivers in practice:

- Transparency and user trust. Verified platforms attract users who want security for their funds. Fraudsters self-select away from platforms where they know their identity will be checked — they move to softer targets.

- Reduced identity theft exposure. Robust identity verification — including liveness detection — catches fraudsters using fake or stolen identities before they get access to the platform. iDenfy‘s 3D liveness detection addresses impersonation threats common in crypto and Web3 contexts. See how iDenfy detects deepfakes and fraud risks at onboarding.

- Money laundering prevention. Every verified user is traceable. That traceability — when users know it exists — changes behavior. Launderers move to platforms without it.

- Reduced legal and regulatory risk. Non-compliant platforms don’t just face fines — they face operational shutdown, criminal exposure for executives, and the reputational cost of being publicly associated with illicit finance.

Related: What Is Cryptocurrency? Key Facts & Security Tips

How Major Crypto Exchanges Approach KYC

Regulatory requirements vary by jurisdiction, and some exchanges historically registered in low-compliance jurisdictions to reduce their KYC burden. That gap is closing. FATF’s updated guidance, the EU’s Markets in Crypto Assets (MiCA) regulation, and FinCEN’s enforcement posture have pushed KYC requirements toward global applicability regardless of where a platform is incorporated.

The major exchanges have already adjusted. Coinbase requires full KYC before any buy or sell transaction. Binance allows limited withdrawal functionality for unverified accounts but restricts trading access until verification is complete. Exchanges operating in the US require personally identifiable information (PII), a government-issued ID, and a Social Security Number as part of the onboarding flow. What varies is the depth of the verification and the friction it creates — which is where the technology choice matters.

Manual vs. Automated KYC — Where the Real Difference Shows Up

Manual KYC runs through human analysts reviewing submitted documents and identity data. It works at low volume. At any meaningful scale, it creates three problems that compound each other:

- High cost. Regulatory-grade manual review requires trained staff. For small and mid-sized crypto companies, the cost of running a compliant manual KYC operation can outpace the compliance budget — especially when verification volumes spike.

- Slow turnaround. Customers who complete onboarding and then wait hours or days for manual document review don’t always wait. Drop-off at the verification stage is a real conversion problem, not just an inconvenience.

- Human error rate. Sophisticated document fraud — altered holograms, printed photographs, digitally edited ID images — is difficult for human reviewers to catch consistently. Automated systems trained on fraud signals catch patterns that a human analyst reviewing their twelfth document of the day will miss.

Automated KYC resolves all three. Document classification, OCR extraction, liveness detection, and AML screening run simultaneously — verification completes in seconds, not hours. Onboarding doesn’t slow down as volume grows. And fraud detection is consistent regardless of how many sessions are running in parallel. Video KYC and liveness detection are the specific technologies that close the manual-review gap in crypto onboarding.

Related: Top 5 KYC Challenges and How to Overcome Them

Future Trends: KYC in the Next Phase of Crypto

The regulatory trajectory is toward more KYC in crypto, not less. The FATF Travel Rule update requires not just identity verification at onboarding but transaction-level data sharing — who is sending, who is receiving, and what the trail looks like. MiCA brought the EU’s crypto framework in line with traditional financial regulation. The decentralized finance sector, which has operated largely outside compliance frameworks, is next.

The counterargument — that KYC introduces centralization and undermines the decentralized ethos of crypto — runs into a practical problem: fraud and money laundering at the scale documented above draw regulatory responses that are far more disruptive than KYC requirements. Zero-knowledge proof technology is developing as a potential middle path: cryptographic verification that proves identity without exposing underlying personal data. It’s not production-ready at scale, but it represents the most credible technical route toward compliance that doesn’t require a platform to hold and process every user’s passport scan. The broader shift toward decentralized identity sits in the same direction. For stablecoins specifically, iDenfy offers a dedicated stablecoin compliance service.

For now, automated KYC with strong biometric verification and integrated AML screening is the standard that regulators expect and that the fraud data justifies. Platforms that build it in early are in a better position — both with regulators and with users who care about where their funds are held.

Want to discuss how iDenfy fits into your crypto platform’s compliance stack? Book a call with our team.

The Bottom Line

KYC in blockchain is a legal obligation for regulated crypto platforms — and an operational necessity for any platform that doesn’t want to be used as a vehicle for the fraud and money laundering that has defined the industry’s enforcement history. The $14 billion in crypto fraud losses in 2021, the documented NFT fraud types, and cases like Bitzlato and Tornado Cash are not edge cases. They are what happens when identity verification is absent.

The technology to run KYC without destroying the user experience exists. Automated verification completes in under 30 seconds. Liveness detection stops deepfake and impersonation attacks. Integrated AML screening covers the post-onboarding risk picture. The decision isn’t whether to implement KYC — it’s whether to implement it well.

Related: Best KYC Software — Ranked and Reviewed