Building an effective anti-money laundering (AML) compliance program is easy on paper. In reality, many financial institutions face challenges when it comes to doing it all: verifying customer identities, developing internal controls, updating policies, and continuously monitoring for suspicious activity.

In this blog post, we take a more detailed look into the Bank Secrecy Act while examining its requirements and discussing key strategies to ensure compliance and prevent fraud.

What is the Bank Secrecy Act?

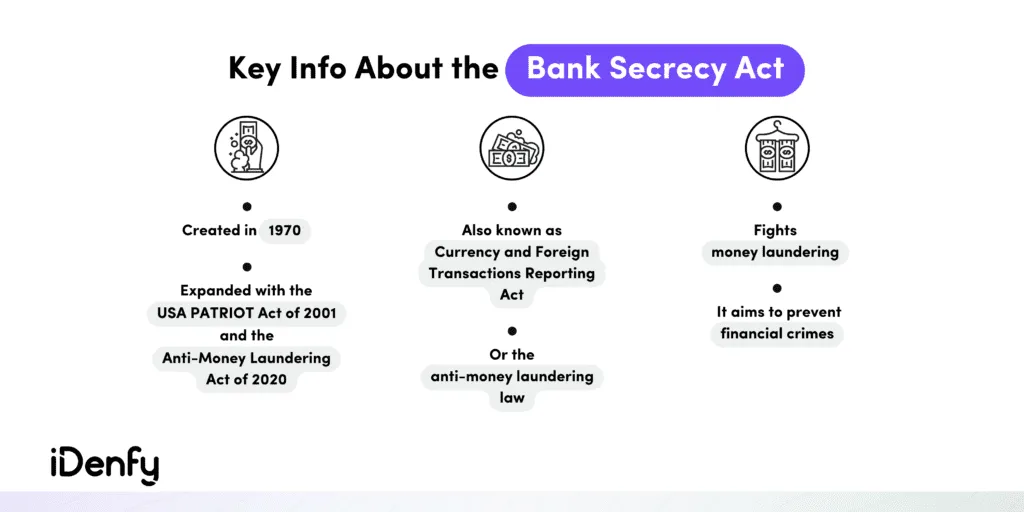

The Bank Secrecy Act (BSA) is a crucial US regulation that outlines required record-keeping and reporting practices intended to fight against money laundering. It was first implemented in 1970 but remains one of the key grounds for the global regulatory landscape. It’s also known as the Currency and Foreign Transactions Reporting Act and is sometimes called the anti-money laundering law.

The Bank Secrecy Act is developed by the Department of Treasury’s Financial Crimes Enforcement Network (FinCEN) and lays out specific conditions that must be reported. The BSA requires institutions to identify and monitor potential money laundering activities and report them to authorities for further investigation and prosecution:

Specific BSA/AML compliance program rules:

- File reports of cash transactions above $10,000.

- Keep records of cash purchases of negotiable instruments.

- Report suspicious activity that might signify money laundering, tax evasion, or other crime.

The Bank Secrecy Act has undergone multiple amendments over time to adapt to the changing financial landscape and evolving strategies employed by criminals. Currently, the BSA collaborates with the Patriot Act to combat money laundering and terrorist financing.

💡 Related: KYC in Banking Explained

Automate your identity verification

See how iDenfy helps 1,000+ companies verify customers in seconds with AI-powered KYC.

Explore iDenfyWhat is the Primary Objective of the Bank Secrecy Act?

The main objective of the Bank Secrecy Act is to prevent financial institutions from engaging in illicit activities, such as becoming channels of money laundering. The BSA regulates banks, lenders, and other financial entities to report to the government and report suspicious activity in case of tax evasion and other financial crimes.

FinCEN, the administrative body for the BSA, imposes specific requirements on financial institutions to ensure compliance with its provisions. Senior management in financial institutions must possess a comprehensive understanding of the legislation in order to fulfill their BSA-related requirements effectively.

What are the Bank Secrecy Act Requirements?

Since the law establishes several requirements that financial institutions must meet, maintaining compliance with the Bank Secrecy Act can be a complex task. The BSA requires financial institutions to implement proper record-keeping policies and ensure that documentation and appropriate information are collected.

In addition, the BSA obliges financial institutions to take action when suspicious activity occurs, including cases involving:

- Receiving trade or business payments in the form of cash exceeding $10,000. If that happens, filing an IRS Form 8300 is required.

- Having ownership of one or more foreign bank accounts, mutual funds, or comparable financial accounts. Financial institutions must report these accounts to the IRS annually.

- Engaging with a money services business (MSB). According to FinCEN, an MSB is any person conducting business, regardless of regularity or organizational structure, and also includes organizations like check cashers, currency exchangers, and money transmitters.

This all goes into the fact that the Bank Secrecy Act requires financial institutions to develop their own internal AML policies, procedures, and controls. This rule was developed in Section 352 of the Patriot Act, which amended the BSA, and further expanded requirements for financial institutions.

💡 Related: What are the Key AML Laws in the US? [Business Guide]

Which Agency Enforces the Bank Secrecy Act?

The Financial Crimes Enforcement Network (FinCEN) enforces the Bank Secrecy Act. It also sets clear requirements for financial institutions that are also designed for the same purpose of helping prevent financial crime, fraud, money laundering and terrorist financing. FinCEN is also responsible for reviewing and analyzing suspicious activity reports submitted by reporting companies.

What are the Five Pillars of AML Compliance?

Complying with the Bank Secrecy Act is crucial for financial institutions to prevent money laundering and other financial crimes. But what does it take to stay compliant? Since its first introduction, the BSA evolved, and new regulations have been introduced.

Modern AML compliance revolves around five key rules or pillars. They instruct financial institutions to:

- Designate a BSA/AML compliance officer. They are responsible for supervising the institution’s AML initiatives and ensuring strict adherence to all BSA rules.

- Establish an internal framework of policies and controls. This helps build a system that achieves and sustains AML compliance. This framework should encompass special fraud prevention measures, such as identity verification, screening and monitoring, as well as other activities.

- Collaborate with an independent third-party auditor. They help provide a fresh perspective, detect vulnerabilities within the compliance program, and ensure ongoing compliance.

- Create training programs for your staff. The training should be aligned with current trends in the financial market and address common signs of money laundering, such as unusually large transactions, suspicious personal information, or atypical account behavior.

- Deploy in-depth risk assessment. That means following a risk-based approach, which involves executing customer due diligence (CDD) and enhanced due diligence (EDD) practices to detect suspicious user behavior, establish risk profiles, and monitor high-risk accounts or transactions more effectively.

💡 Related: AML Compliance Program — Step-By-Step Guide

Who is Responsible for BSA/AML Compliance?

The described five pillars of AML compliance mandate financial institutions to choose a designated compliance officer. In general, compliance officers are the first line of defense in safeguarding the financial institution from fraud and ensuring that it meets all regulatory requirements.

The compliance officer’s job is to oversee and manage all people associated with the company, including employees, customers, and other stakeholders. That involves internal training and ensuring that all members are aware of the main money laundering prevention processes. The responsible BSA/AML compliance officer is also accountable for supervising the activities of other compliance officers and is appointed by the board of directors.

How to Ensure Compliance According to the Bank Secrecy Act?

Apart from the five pillars of AML compliance and the importance of building a BSA/AML compliance program, there are other crucial responsibilities that financial institutions must take into account.

To simplify the BSA rules for you, we’ve divided them into two stages that you must follow:

Conduct Customer Identity Verification

All financial institutions are obliged to stay compliant with Know Your Customer (KYC) regulatory requirements. Identity verification wasn’t initially mandated by the BSA. Despite that, the principles of KYC were introduced through FinCEN in the early 1990s and further expanded by the Patriot Act in 2001.

This is a common procedure during the customer onboarding process when a user creates an account for the first time on a digital platform and has to verify their personal information for security reasons.

Customer identity verification processes differ among financial institutions but generally involve collecting customer data, such as name, date of birth, address, or Social Security number, from reliable sources like government-issued ID documents. Verified customers are then checked against databases like sanctions lists, adverse media lists, PEPs, and global watchlists.

Ensure Continuous Monitoring and Reporting

The BSA mandates financial institutions to conduct ongoing monitoring and, this way, prevent financial crime. There are also multiple reports that companies must file in case the suspicious activity actually occurs.

The main BSA-required reports include:

- IRS Form 8300. Companies that receive cash payments amounting to $10,000 or more in a single business day, whether from a single transaction or multiple transactions, are required to file a Form 8300.

- Currency Transaction Report (CTR). Institutions must submit a CTR whenever a customer engages in cash transactions exceeding $10,000 in a single business day, regardless of whether it involves single or multiple transactions.

- Foreign Bank and Financial Account Report (FBAR). Individuals who possess a minimum of $10,000 in a foreign bank account are required to file an FBAR annually. While the responsibility lies with the account holder, it’s common for tax professionals or wealth managers to handle the filing process on behalf of their clients.

- Suspicious Activity Report (SAR). Financial institutions must file a SAR if they suspect any suspicious activity. It typically involves patterns of behavior that may suggest a customer’s intention to evade CTR requirements or involvement in activities such as money laundering, wire fraud, terrorist financing, or other forms of financial crime.

While reporting involves submitting various reports to the appropriate authorities, monitoring plays a complementary role by actively observing and analyzing transactions and customer behavior to detect potential red flags and suspicious activities.

💡 Related: An Overview of the Anti-Money Laundering Act of 2020 (AMLA)

Why is the Bank Secrecy Act Still Important Today?

The Bank Secrecy Act is one of the key pieces in AML compliance and plays a vital role in protecting the whole financial system. The BSA’s specific requirement of reporting certain monetary instruments above $10,000 helps successfully deter financial crimes and money laundering.

More importantly, its influence is felt today since many newly emerging industries, such as crypto or online gaming, are already regulated by KYC and AML compliance requirements, which originated with the BSA. Failure to comply with the Bank Secrecy Act can lead to severe penalties, resulting in damage worth thousands of dollars.

With iDenfy’s fully automated all-in-one identity verification and fraud prevention platform, you can ensure secure customer onboarding. Along with customer and corporate KYC checks, we offer various due diligence solutions in one place — all of which help you stay in BSA/AML compliance without hassle.

See our solutions in action or get started right away.