Reducing fraudulent chargebacks can be a lengthy and exhausting process. While international chargeback fraud is illegal, it seems that chargebacks are reaching sky-high numbers, and in some cases, traditional anti-fraud measures don’t help companies prevent such major losses.

The volume of chargebacks can leave companies uncertain about whether they’ll face minimal chargeback losses or lose millions in the following year. Not only that but also the scope of growing fraudulent activities online makes it harder for businesses to safeguard their assets.

Ponemon Institute’s recent report reveals that 61% of respondents acknowledge their companies lack the appropriate technologies to combat online fraud. On top of that, only less than half of the respondents indicate that their organizations actually have the in-house expertise to prevent online fraud, such as chargebacks.

So, the first step to minimize costs linked to chargebacks is for businesses to actually understand what this phenomenon is, how it works, and what the key practices are to respond when the risks are identified.

In this blog post, we go around five talking points:

- What are chargebacks exactly, and how do they happen

- What is the difference between a chargeback and chargeback fraud

- Is it possible to prevent chargebacks, and if so, how

- What key reasons make chargebacks so expensive for businesses

- How to reduce chargeback fraud costs for businesses

What is a Chargeback?

A chargeback is a process that happens when a cardholder initiates transaction reversal, also known as a dispute, in order to receive a refund from their bank or the credit card company. While the process itself generally protects customers from fraud, dishonest individuals can exploit the system on purpose.

Customers often initiate chargebacks because of dissatisfaction with a product or service or errors made by the business. In practice, customers often use chargebacks simply to avoid returning disliked items or for orders that never arrived. However, chargebacks can happen when a cardholder files a chargeback for a legitimate purchase they made.

Why do Chargebacks Happen?

Chargebacks serve the purpose of addressing credit card fraud and errors like:

- There was an accidental double charge

- A subscription needs to be canceled

- An incorrect amount was charged

- There were damaged or missing goods

- The item arrived not as described

- The goods took too long to arrive

- Stolen cardholder data was used

Originally, chargebacks first aimed to remedy credit card fraud, boosting consumer confidence in credit cards. This concept was designed almost half a decade ago to create a system for basic consumer protection. In practice, today, such disputes are easily accessed tools for buyers who simply don’t want to go over the hassle of returning their received items and would much rather receive a refund instead.

What hurts businesses most is that with chargebacks, customers reclaim funds directly from their bank or card company, bypassing the merchant entirely. So, unlike refunds, chargebacks can be more harmful to merchants, given the costs and the possibility of negatively affected reputation or regulatory compliance.

What is Chargeback Fraud?

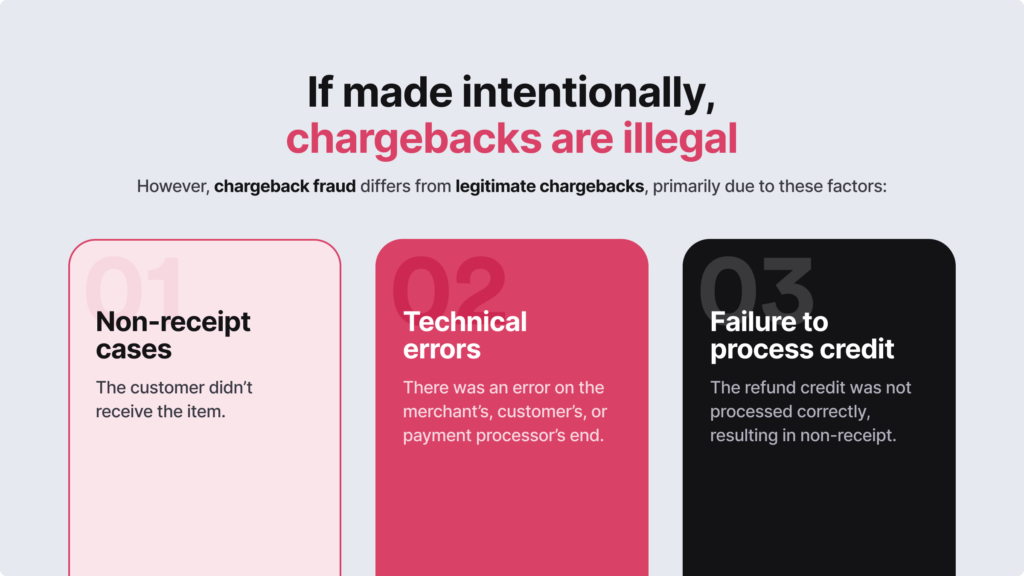

Chargeback fraud is the process when a customer disputes a charge on purpose with the intention of securing a refund and keeping the received service or product. This form of consumer fraud happens after receiving the goods or services.

The customer might claim that they didn’t receive the product, that it was defective, or that the transaction was unauthorized. Though occasional misunderstandings can occur, chargeback fraud is illegal and carries significant consequences.

Businesses can’t stop chargeback fraud. They can only address it through disputes filed after it happens. Typically, this involves reversing each fraudulent chargeback with some sort of evidence that would show that the customer authorized their purchase and that everything was done accordingly.

Related: Fraud Detection — What You Need to Know in 2024

Can Companies Stop Chargebacks?

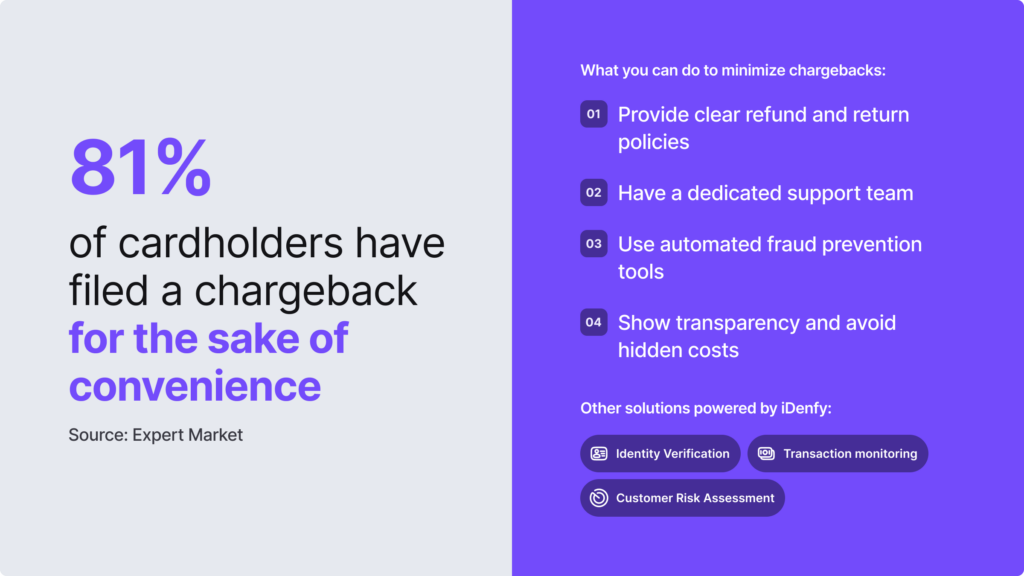

Unfortunately, there’s no such thing as stopping chargebacks from happening completely. However, companies use special tactics to minimize losses due to chargeback fraud while, at the same time, trying to minimize chargebacks altogether.

Businesses cut down on the number of chargebacks by:

- Enhancing the likelihood of successfully reversing a chargeback.

- Minimizing the chances of customers who are only seeking chargebacks.

- Implementing additional fraud prevention tools to prevent fraud in general.

- Choosing a payment processor that doesn’t have a chargeback dispute option.

If companies don’t pay enough attention to reducing chargebacks, they are risking receiving negative reviews and comments from their customers. This also makes the brand more susceptible to fraud, leading to a label of an “untrustworthy” business and loss of sales in the future.

How to Prevent Chargeback Fraud?

To effectively prevent chargeback fraud, businesses need to use special measures and maximize the opportunities for buyers to feel satisfied with their received purchases. Of course, this requires following a clear plan that would improve business operations.

Here are essential steps that assist businesses in mitigating disputes and countering chargeback fraud:

Have a Transparent Refund Policy

Customers often use chargebacks as an easy way out from the hassle of returning items or seeking refunds. To reduce fraudulent chargebacks, businesses should make an easy-to-understand refund policy, ensuring customers understand how to return their items. If a customer is determined to secure a refund, it’s crucial to guarantee that the reimbursement occurs through the company’s actual refund process rather than a chargeback. Despite both involving returning funds to the customer, refunds are more favorable for businesses than chargebacks.

Use Detailed Product Descriptions

Another major issue that customers might feel dissatisfied after receiving their items is the lack of detailed product descriptions. If the product doesn’t match the description, chances are that they might opt for a chargeback. You can avoid that by investing extra time in creating detailed and thoughtful product descriptions, categories, and filtering options, along with accurate photos or videos of the products to prevent chargebacks.

Provide Clear Delivery Updates

Equipping customers with crucial delivery updates helps them navigate all the right channels when facing delivery issues. If customers suspect their ordered product is lost in transit or unlikely to arrive, they shouldn’t resort to chargebacks. Good thing that you can enhance chargeback prevention by providing customers with clear delivery details, including the confirmation and tracking numbers and links for delivery carrier updates. You should have an internal team that’s responsible for contacting the right party if there are no updates or the package doesn’t arrive on time.

Avoid Hidden Costs and Automatic Billing

Memberships or subscription-based services that end their free trials with automatic billing can lead to unnecessary chargebacks. While automatic billing is a common business strategy, it can also result in some drop-offs for your company. If you have a free trial plan, think about eliminating automatic billing after free trials as a strategic chargeback prevention measure.

Have a Dedicated Support Team

Being accessible means that you care about your products and services. As a business, you’re not avoiding any challenges; it’s the opposite — you are taking your time to listen to your customers to solve any potential issues. So, if customers face issues with the goods or services, such as unexpected subscription charges or receiving the wrong items, and struggle to reach you, they are more likely to dispute their purchases. That’s why a strong customer support team reduces chargebacks by resolving issues directly and allows you to avoid additional chargeback costs.

Implement Fraud Prevention Tools

Automated fraud prevention tools use AI and machine-learning algorithms to analyze user behavior, their transaction data, and suspicious activity, preventing fraudulent transactions before they lead to chargebacks. At the same time, using AI-powered identity proofing tools, such as Know Your Customer (KYC) verification or simply identity verification, is a common practice to add an extra layer of protection against the fraudulent use of accounts, which is the primary cause of chargebacks in card-not-present transactions.

By implementing fraud prevention tools, you ensure that users are who they claim to be, reducing the risk of unauthorized transactions, account takeover fraud (ATO), or identity theft. By requiring users to upload government-issued ID documents, you can establish a trustworthy audience and gather key information about your users. This helps better assess the risk associated with each customer. For example, if a user’s identity is verified through KYC processes, the company can gain insights into the user’s transaction history and flag potentially suspicious activities before they escalate into chargebacks.

Related: AML Automation — Streamlined Compliance for Businesses

Why are Chargebacks Bad for Businesses?

Companies can reverse a chargeback if they suspect abuse in the process. Despite that, reversing a chargeback for businesses means many time-consuming procedures and high processing fees. That’s why some merchants see more drawbacks than benefits in this process, choosing to settle the chargeback with the customer instead.

As a result, chargebacks can cause financial losses and other negative effects, including:

- Harming the company’s reputation

- Losing the ability to accept payments

- Receiving penalties and fines

- Increasing fees from payment processors

- Losing inventory

If a chargeback happens, the customer’s bank or credit card company must refund the disputed amount to the customer and debit the exact same sum from the business’s account. Additionally, double refund chargebacks can happen when the customer files both a chargeback and a refund request. This occurs when the merchant processes the refund before getting notified about the chargeback, which leads to double payments.

What is the Cost of Chargeback Fraud for Businesses?

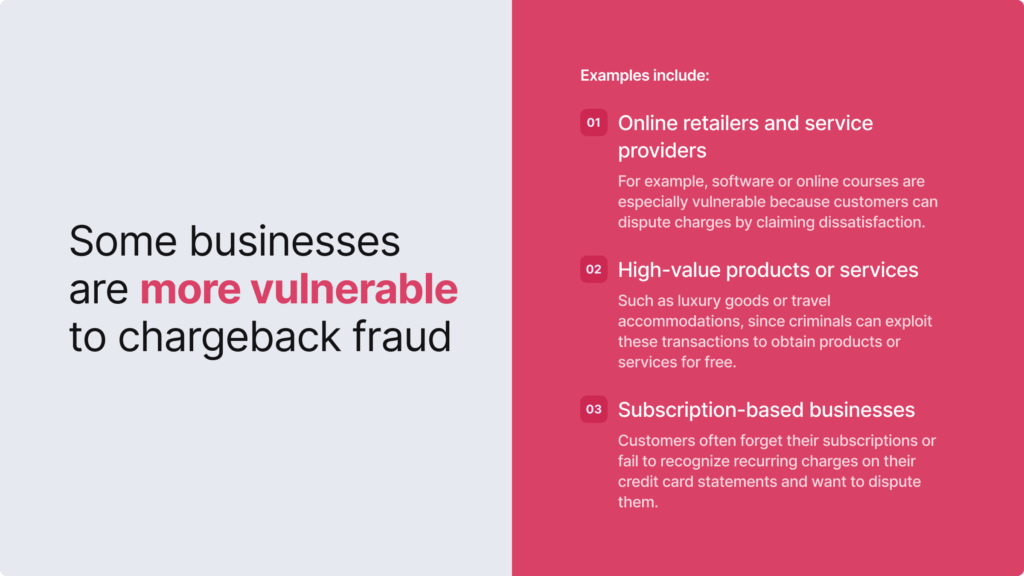

Specialists from Chargebacks.com estimate that for every $100 in chargebacks, the actual cost is $240. In the e-commerce industry, Checkout.com claims that 27% of merchants report an increase in chargeback rates.

Despite that, chargeback fraud can impact businesses of any industry or size as long as they handle credit card transactions. For example, subscription-based businesses or those dealing with luxury goods tend to face higher costs of chargeback fraud.

Businesses also have to pay for chargeback fraud with wasted time, penalties, and additional costs, such as:

- Lost opportunities. Each order resulting in a chargeback could have been a potential sale. Chargebacks translate into indirect costs, representing lost opportunities for revenue, negatively affecting the company’s growth.

- Additional operational costs. Processing an order involves various operational expenses and resources, including design, production, packaging, shipping, and logistics. In case of chargeback fraud, companies don’t receive refunds for these expenses.

- Reversal expenses. If the customer initiates a fraudulent chargeback, deciding whether to attempt a reversal correctly is crucial. Companies should attempt to reverse the chargeback if they have legitimate evidence that they can submit to the bank.

Keep in mind that most businesses accept a 1% chargeback-to-transaction as the highest appropriate figure. Depending on the company’s payment provider, they could face increased transaction fees and other penalties due to an excessively high chargeback ratio.

iDenfy’s Take On Minimizing Chargeback Fraud Costs

While it’s unrealistic to expect complete avoidance of chargebacks, businesses can better prepare themselves to dispute unwarranted chargebacks and efficiently address legitimate fraud cases. This is where, once again, effective fraud prevention programs can positively impact the losses linked to chargeback fraud.

With simple, user-friendly tools like identity verification at customer onboarding, businesses can avoid fake accounts, double-accounting, unauthorized transactions, unnecessary chargebacks, and overall fraud on their online platforms. This helps detect fake or expired documents, automatically collect and verify user’s personal data, and make sure that the person trying to register onto your platform and engage in financial transactions is real.

Read our customer stories on an effective approach to minimizing chargeback costs in industries like prop-tech, fintech, etc., and get started to find out how iDenfy can reduce your chargeback costs with custom-tailored KYC/AML solutions.