Heightened operational costs, challenges in staff retention, increased fraud prevention threats, and never-ending changes in regulatory compliance. These are at least some of the challenges companies face today. From looking for the best identity verification solution to completing the onboarding process to implementing an AI-powered tool for ongoing due diligence, this is just a small piece of the puzzle in the complex fraud detection landscape.

Fraud detection is especially important in the first customer cycle or the customer onboarding stage in order to catch criminals before they start their devious schemes, even on a larger scale. That’s why financial institutions and other companies with money flow ask customers to submit identity, residence, income, and asset documents. However, verifying identities through a simple document verification process isn’t enough. And when it comes to fraud detection, manual operations can become a true hassle, leading to more opportunities for criminals.

In this blog post, we talk all about RegTech and how to make your fraud detection strategy a successful multi-layer defense against fraudsters.

What is Fraud Detection?

Fraud detection is a strategy that companies implement for various fraud prevention measures, such as screening customer behavior or monitoring transactions to combat fraudulent activity. The term ‘fraud detection’ is closely related to a broader anti-money laundering (AML) strategy. That’s why companies use fraud detection and prevention measures as part of their AML compliance processes.

Fraud detection involves identifying and preventing fraudulent activities or attempts. Implementing a fraud detection system is crucial to proactively prevent fraud, safeguarding businesses and consumers from potential financial losses. Businesses have the flexibility to customize their fraud detection programs. Regardless of its structure, fraud detection typically relies on automation and technology, as well as the company and its established policies for effective operation.

Stop fraud before it starts

From deepfakes to document forgery — iDenfy catches fraud attempts with AI-powered liveness detection and document checks.

Explore Fraud PreventionFraud Detection Examples

Identity verification is a common example of fraud detection, which confirms that the user is genuinely who they claim to be and a legitimate customer conducting the transaction. As a result, fraud detection acts as a primary security barrier against different types of fraud, from minor crimes, such as a forged signature, to major felonies, like stealing identities.

Fraud detection methods must be dynamic, extending beyond identity verification at the customer onboarding process. Other examples of fraud, such as credit card fraud, account takeover (ATO), or phishing, can lead to substantial financial consequences for both businesses and their customers. For this reason, fraud detection is important in many industries, not just banks. For instance, healthcare, cryptocurrency, and e-commerce companies use fraud detection systems to prevent unwanted consequences.

Fraud Classification

The Federal Reserve, the central banking system of the US, has created a tool to recognize fraud called the FraudClassifier Model. It’s an interactive system that categorizes fraud based on the payment’s origin and the methods that were used, which helps entities accurately identify different types of fraud. It also serves as a valuable tool for developing effective fraud prevention strategies, providing a standardized classification system with clear, step-by-step guidance for users.

Before the FraudClassifier Model, inconsistent fraud categorizations made it difficult to understand and manage different types of fraud. For example, companies didn’t differentiate between credit card theft and identity theft and grouped them together, while others used them in separate categories. This model uses consistent terminology, serving as a common language for financial institutions, regulated entities, and fraud detection service providers.

Why is Fraud Detection Important?

Fraud detection is important for preventing financial crime and severe non-compliance fines. In general, fraud poses a major threat, causing harm to both individuals and businesses. For companies, annual costs can easily reach billions, consisting of direct expenses for loss prevention and investigation services, as well as indirect costs arising from lost productivity and diminished customer trust. For example, Juniper Research’s study on combating online payment fraud forecasts global losses exceeding at least $343 billion until 2027.

Specific jurisdictions mandate fraud programs. For instance, in the UK, a “Failure to Prevent Fraud” offense was enacted in April 2023, making companies liable for employee fraud benefits without adequate fraud prevention programs. Consequently, businesses are intensifying efforts to boost their fraud detection measures, aiming to shield both themselves and their customers from financial harm.

Fraud Detection vs Fraud Prevention

Both terms, fraud detection and fraud prevention, though often confused, carry distinct meanings. Fraud detection involves identifying and recognizing instances of fraudulent activity after they have occurred, typically through screening and monitoring of transactions or behavior. In the meantime, fraud prevention focuses on implementing measures and strategies to stop fraudulent activities from happening in the first place, aiming to reduce the likelihood of fraud.

In other words, fraud detection is about recognizing fraud in real-time. Here’s a quick breakdown of the main differences between these two:

- Fraud detection is practical, enabling immediate action, investigation, and loss recovery. Detection searches for patterns indicating payment fraud, like multiple transactions to one location within a short time frame, flagging suspicious behavior.

- Fraud prevention is proactive, aiming to prevent fraud by taking pre-emptive measures. Prevention analyzes all available data on users or transactions, scrutinizing details such as data transfer, identity, and creation time.

Fraud Detection and the 3 D’s of Fraud Prevention

Fraud detection is closely tied to the triple approach to fraud prevention, also known as the 3 D’s of the fraud prevention framework. For businesses, this helps build a robust anti-fraud program that involves three vital steps:

- Deter. Increasing obstacles for potential fraudsters, dissuading them, and redirecting them to easier targets.

- Detect. Enhancing the ability to recognize signals and assess risks, enabling instant identification of fraudulent accounts or suspicious activities.

- Deny. Heightening barriers to prevent known offenders from re-entering, this way preventing repeated criminal offenses.

Fraud Detection for Individuals

When it comes to individuals, they often remain unaware of fraudulent activity until it reaches a critical stage. Nonetheless, certain warning signs can indicate potential fraud, including:

- Unusual charges on bank accounts

- Abnormal activity on credit cards

- Rejection of credit cards or loans

- Missing or delayed mail

- Receipt of bills for medical services not received

- Bills erroneously marked as unpaid despite timely payment

Related: How to Check if Someone Is Using Your Identity?

How Does Fraud Detection Improve Risk Management?

Having good fraud detection measures means that an organization has built an overall risk management strategy that improves various aspects of the business. For example, fraud detection:

- Helps maintain customer trust. It demonstrates a commitment to security and protects users from various threats, such as account takeovers or unauthorized charges.

- Ensures legal compliance. For regulated entities, such as banks or crypto platforms, fraud detection is a part of AML laws, which reduces legal exposure.

- Protects financial assets. Fraud detection helps identify fraudulent behavior early, preventing major losses and customer dissatisfaction.

- Prevents crime. It works as part of a bigger system for preventing money laundering, terrorism financing, and related financial crimes that can be conducted via the company’s financial system. For example, vendor due diligence is also vital since there are third-party risks that can be used and abused to launder funds via another company as a channel.

Related: Fraud Risks in Onboarding Systems

Common Types of Fraud

There are some popular fraud types and deceptive practices that bad actors tend to use in various industries. For example:

Refund Fraud

Refund fraud occurs when individuals or groups falsely exploit an online store’s return policy to claim a refund. The aim is to deceive the business into providing compensation for costs the fraudster never incurred. This allows them to keep both the money and the products. Common tactics include falsely claiming that the purchase was “not as described” or “unsatisfactory.”

Chargeback Fraud

Chargeback fraud happens when a customer intentionally disputes a charge to secure a refund while keeping the product or service. This type of fraud happens after the customer has already received what they paid for. Common claims include stating the product wasn’t delivered, was defective, or that the transaction was unauthorized.

The worst part is that companies cannot entirely prevent chargeback fraud but can address it by disputing fraudulent claims after they occur. This usually involves providing evidence that the customer authorized the purchase and that the transaction was handled properly.

Related: What is a Transaction Dispute? [Challenges for Merchants]

Account Takeover Fraud (ATO)

Account takeover (ATO) is a type of identity theft where cybercriminals gain unauthorized access to an online account, such as an email, bank account, or social media profile. During an ATO attack, criminals use stolen credentials to hack accounts through methods like phishing, data breaches, and social engineering. These attacks aim to steal personal and financial data, targeting not only individual accounts but also organizations.

This is why ATO fraud gives criminals a starting point to exploit vulnerabilities and potentially compromise an entire system or network. Cybercriminals use malicious tactics to infiltrate corporate systems, and in severe cases, publicly reported ATO incidents can lead to significant drops in stock market value. Criminals also frequently buy or trade usernames and passwords on the dark web at minimal cost.

Loan Fraud

Loan fraud is a deceptive practice where criminals use stolen personal data to obtain loans for financial gain. The fraudster’s goal is to access the funds without being caught, leaving the affected party with financial losses.

Loan fraud can occur whenever people borrow money or extend credit. It takes many forms, including mortgage fraud, ATO fraud, and other scams, such as online lending fraud. This type of fraud is common because some institutions (depending on the jurisdiction) require minimal information and identification during the loan application process.

New Account Fraud

New account fraud occurs when criminals create accounts using fake or stolen identities, sometimes mixing real and counterfeit details to complicate detection. They often use fake identities to secure new credit or debit cards, typically within the first 90 days of the account’s creation, starting with small deposits to avoid detection.

Fraudsters also use tactics like social engineering, phishing, or ATO fraud to commit other crimes, such as taking out loans, committing insurance fraud, or engaging in illegal black market activities. In this sense, new account fraud is often linked to other crimes.

Related: First-Party, Second-Party, and Third-Party Fraud

What Does a Fraud Detection and Prevention Program Look Like?

A fraud detection and prevention program shares similarities with the five pillars of an AML compliance program in their overarching goal of mitigating financial risks and ensuring the integrity of financial transactions. In addition to technology and automated anti-fraud tools, a comprehensive program consists of:

- Dedication of a team of fraud prevention specialists, providing human oversight for scenarios requiring manual review despite the high automation of risk-based software approaches.

- Establishment of internal processes defining risk thresholds for each customer or transaction, streamlining internal processes, and minimizing resources dedicated to manual reviews.

- Implementing a dedicated staff training system, expanding beyond just fraud and compliance teams to also include executives, ensures awareness of prevailing fraud risks and potential security hazards. This approach is designed to enhance security awareness training across the board.

- Integration of monitoring, documentation, and reporting procedures for internal data hygiene and compliance with existing regulations, such as AML requirements.

- Continuous updating of the mentioned practices through regular internal and independent third-party auditors to ensure the programs’ compliance and effectiveness.

By incorporating these principles into their design, fraud detection programs and AML compliance programs enhance the company’s ability to identify and prevent fraudulent activities, ultimately boosting the security of the financial system. Neglecting these measures can result in reputational damage or more severe consequences for the business, especially if it is a regulated entity.

Related: What are the Five Pillars of AML Compliance?

What are the Best Fraud Detection Practices?

When considering the implementation of fraud detection for your business, it’s crucial to know the best practices. So, it’s safe to say that the effectiveness of a fraud detection and prevention strategy hinges on the tools you use. Given the ever-changing landscape of fraud, it’s essential to use a systematic toolset combining both technological solutions and manual anti-fraud review measures.

Here’s a short overview of the most effective fraud detection practices based on common technological solutions:

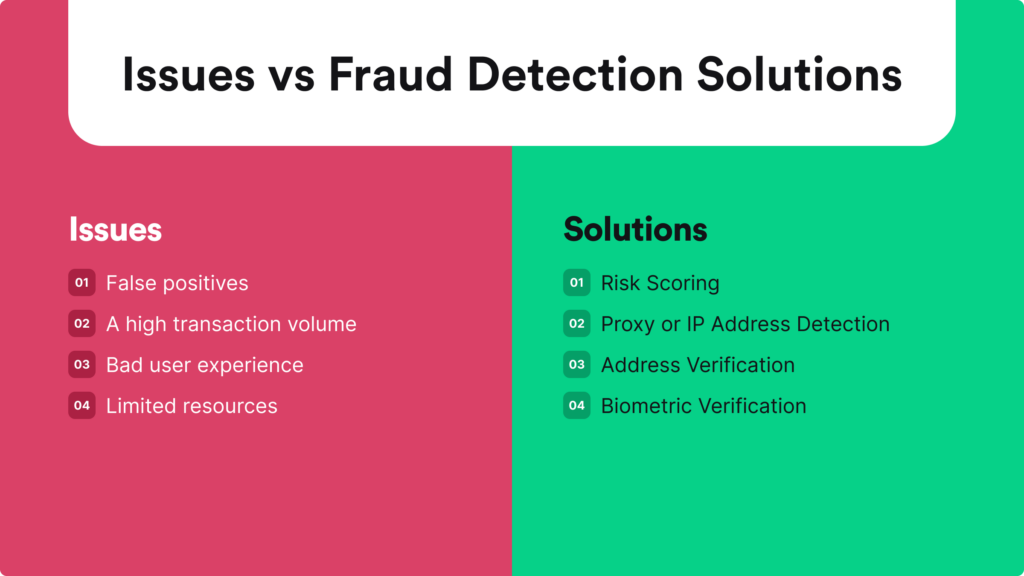

1. Risk Scoring

The majority of online fraud prevention tools operate through the application of risk rules, which can range from straightforward measures like blocking specific IP addresses to more complex evaluations of user behavior frequency. At the core of customer AML risk assessment is a risk model designed to compute a risk score or rating, typically categorized as high, medium, or low. This score or rating serves as a concise tool for the compliance team and the business line, offering a transparent overview of the risks associated with the customer relationship and related activities within the institution.

Risk scoring analyzes a diverse set of data points and their interrelations to gauge the likelihood of various outcomes, typically spanning a spectrum from “most likely” to “least likely.” These models, which heavily rely on machine learning, include common types of fraud prediction or identification measures. They can assess user activity, categorizing it as “fully legitimate,” “fully fraudulent,” or falling somewhere in between.

2. Proxy and IP Address Detection

In 97% of cyber fraud cases, proxies play a pivotal role. In the past, hackers frequently relied on proxy networks constructed from malicious code. This involved luring victims into downloading malware onto their PCs. Today, criminals often attempt to deceive geolocation systems by employing proxies to mask their IP addresses, complicating the process of flagging transactions for review based on IP information or tracing the location of a fraudster.

That’s why the presence of an anonymous IP address, or proxies, can serve as an initial and clear indication of potentially fraudulent intentions. So, whether the company is in the midst of onboarding a new user or facilitating a transaction, conducting a geolocation scan on customers can be a proactive measure to avoid unwarranted losses. Proxy detection is specifically designed to unveil the true location of a user by penetrating through a proxy address.

3. Address Verification

Address verification is a crucial practice of fraud detection that involves verifying the accuracy of billing information provided during a transaction. It shares similarities with geolocation, but it differs in its focus. Address verification works by comparing the buyer’s provided address data with the address on record with the card issuer. If the buyer fails to provide the correct billing address, it raises a potential red flag for fraud.

Here are examples highlighting the benefits of address verification in enhancing a business’s fraud detection strategy:

- Reduction of unauthorized transactions. Address Verification helps businesses identify instances where the provided billing address does not match the records held by the card issuer. If a discrepancy is detected, it can serve as a red flag for potential fraud, reducing the likelihood of unauthorized transactions.

- Custom risk assessment options. Address Verification allows businesses to customize their risk assessment strategies. They can adjust the level of scrutiny based on factors such as transaction amount or customer history, tailoring fraud prevention measures to their specific needs.

- Minimized the stolen credit card rate. In cases where a fraudster gains access to credit card information but lacks the corresponding billing address, Address Verification becomes a crucial obstacle. Fraudsters are less likely to have accurate billing details, making it harder for them to complete transactions successfully.

- Fewer chargebacks. Validating billing addresses helps prevent chargeback fraud resulting from unauthorized transactions or disputes. By accurately verifying addresses, businesses can provide evidence of due diligence in verifying customer identity and transaction legitimacy.

4. Blacklists

Blacklisting is a security practice wherein a catalog of recognized malicious or suspicious entities is established. A blacklist empowers businesses to restrict access from specific users based on various criteria. For example, a company can use this fraud detection practice to prevent transactions from specific countries or regions known for high volumes of online fraud. So, if any of these entities attempt to access the company’s network, they’re automatically blocked, denied access, or flagged for further scrutiny.

This practice transforms blacklists into a potent detection tool, enabling the identification and removal of bad actors who may have eluded detection in the past. For instance, by identifying and preventing these criminals from using your platform and adding them to your blacklist, you can stop them from regaining access in the future when they inevitably attempt to do so again.

Related: Top 5 Ways Fraudsters Commit Identity Theft

5. Biometric Identity Verification

Traditional document and ID authentication, once considered highly secure due to its reliance on difficult-to-replicate parts such as the MRZ zone, has faced challenges in recent times. Advances in technology enabled fraudsters to exploit this method using AI, synthetic identities, 3D-printed masks, deepfakes, and more fraudulent techniques.

To address the vulnerabilities in traditional authentication methods, biometric identity verification and liveness detection technology have emerged as a crucial security enhancement. This algorithm combines biometric data with physiological responses, such as detecting blinking, to effectively detect fraudulent attempts and ensure a more robust Know Your Customer (KYC) process.

For example, in biometric ID verification scenarios, security systems can prompt users to perform specific actions like blinking, nodding, or smiling. This additional layer of security ensures that the KYC process includes dynamic responses, making it harder for non-human entities to bypass the system by responding to random requests.

Facial recognition technology also allows companies to securely re-authenticate users in real-time without relying on traditional passwords. This is crucial as legitimate accounts can be compromised later in the customer cycle. Biometric face re-authentication ensures that the individual accessing the account is the same person who created it initially.

Identifying Challenges in Fraud Detection

The challenge for companies in fraud detection stems from the constant evolution of criminal techniques. To establish an effective fraud detection and prevention program, a delicate balance between automation and internal human compliance teams is crucial. Moreover, businesses need awareness of industry and jurisdiction-specific costs and regulatory frameworks, along with a comprehensive understanding of the primary challenges associated with fraud and its detection processes.

The most common challenges companies face include:

- False positives. Fraud detection systems must be able to differentiate between legitimate paying customers who contribute to the company’s ROI and fraudsters who exploit it.

- Cost management. Many businesses consider investing in additional fraud detection tools, which can be costly. However, relying solely on one fraud detection tool, for example, for transaction monitoring, poses a security challenge.

- Diversity in transaction types. From crypto platforms to traditional banking services like savings accounts, the list goes on. The extensive use of digital services creates entry points for even more fraudulent activities.

- Transaction volume and speed. A high transaction volume coupled with a focus on speedy processing for user convenience can create vulnerabilities, increasing the risk of potential fraud and data breaches for a company.

- Bad user experience. Depending on the industry, collecting necessary personal information for the KYC process is essential. However, this can introduce customer friction, which needs to be balanced against proper user onboarding as well as ongoing due diligence processes.

Related: AML Fraud: Types and Detection Measures

Improving Your Fraud Detection Program with iDenfy

One thing’s clear — you don’t want to partner with a third-party fraud detection service provider who doesn’t have the necessary compliance understanding or in-house expertise to keep up with evolving fraud trends. At iDenfy, we have perfected a complete fraud prevention hub with all of the needed KYC/KYB and AML tools for your fraud detection program.

Improve your fraud detection quickly with our automated systems, user-friendly dashboard, and easy integration through plugins. No need to worry about adding unnecessary complications for users.

Find out more about the variety of fraud detection solutions we offer and a free demo of our RegTech services here.