Transaction disputes can lead to chargebacks, and lately, the chargeback season has been generous for customers disputing their transactions, resulting in millions in damages to businesses. Partially, this is no surprise since many businesses now operate through remote e-commerce channels. But what exactly is a transaction dispute? This process happens when a customer files a complaint about a debit or credit card purchase. So, when a transaction is disputed, the payment the business received can be reversed and refunded to the cardholder.

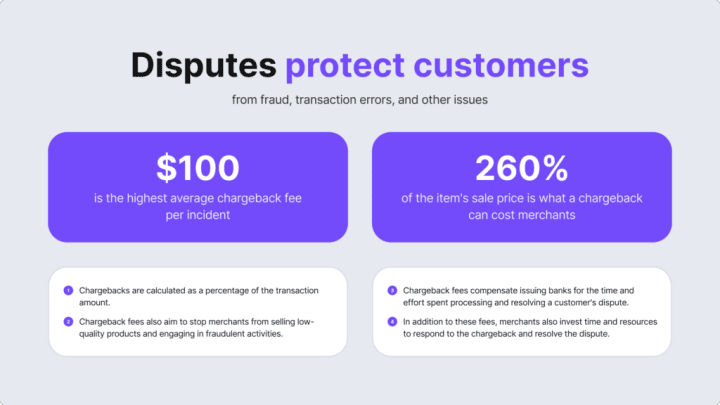

The original goal of such disputes — to maintain a fair and transparent payment system — is vital. Customers exploit this to their advantage and aim to keep the funds without a legitimate reason. In general, disputes should be opened only due to fraudulent activity, such as unauthorized charges, or issues with the merchant, such as an unreceived item. For merchants, this can lead to restrictions, financial penalties, lost inventory, and more.

We discuss critical business tips and ways to respond to transaction disputes.

How Does a Transaction Dispute Work?

The cardholder has to file a complaint against a merchant about a specific transaction. They contact their bank to challenge the payment. Often, the claims from the customer’s side involve a potentially unauthorized transaction, but in general, a transaction dispute can arise for various reasons, such as if the services weren’t provided, the item arrived damaged, the card details were used without the cardholder’s authorization, etc.

For merchants, it’s challenging both to prevent and predict disputes because they can arise from different sources. For example, friendly fraud or first-party fraud happens when a legitimate cardholder engages in fraudulent behavior (whether intentionally or not). In contrast, true fraud disputes work by disputing an actually fraudulent purchase.

Related: What is Chargeback Fraud?

Automate your identity verification

See how iDenfy helps 1,000+ companies verify customers in seconds with AI-powered KYC.

Explore iDenfyThe Legality Behind Transaction Disputes

A transaction dispute is a legal right for the consumer. It isn’t a new practice as well. By implementing a standard transaction dispute policy, the credit card industry wanted to add more trust and confidence as a practice to boost sales and ensure security.

However, many users and bad actors abuse this system. As a result, merchants lose revenue and spend time dealing with the whole dispute process. Additionally, even more funds are required if the business chooses to contest the dispute.

If you’ve worked with payments, you know there’s a list of reason codes showing why the customer disputed a certain charge (if it reaches the chargeback rate).

Cardholder Complaints Qualifying for a Transaction Dispute

🔴 Billing Errors

- Incorrect amounts or dates linked to the dispute.

- Charges not showing the cardholder’s change of address.

- Missing post-purchase credits or returns.

- Charges made outside agreed times or methods.

🔴 Unauthorized Charges

- The cardholder didn’t approve a transaction (for example, the fraudster used stolen information).

- The cardholder doesn’t recognize the charge in their bank statement.

- Items or services show up on the invoice, but they weren’t ordered.

- Multiple identical items were purchased in a short timeframe.

🔴 Service Quality Issues

- Missing items.

- Damaged goods.

- The items didn’t match the description.

- Non-compliance with terms of service/other regulations.

Related: AML Fraud — Types and Detection Measures

What is the Key Difference Between a Dispute and a Chargeback?

The main difference is that most chargebacks start with a dispute. However, not all transaction disputes can lead to chargebacks.

That’s because of the process, which often looks like this:

- A customer disputes a transaction by contacting their card issuer or the bank.

- The bank then reviews the customer’s case and decides if there’s a valid reason to reverse the charge.

- If the bank agrees with the opened dispute, it becomes a chargeback.

Additionally, both terms have been recently used in the same context. In the US, federal laws describe this process as “transaction disputes,” but card issuers have adjusted the terminology over time. For example, Visa has replaced the “chargeback” term with “dispute” in all its procedures and policies.

Related: Chargeback Fraud Prevention — Key Strategies for Businesses

Merchant vs PSP

A merchant is any business that accepts payments. Payment processors use the term “merchant” to refer to their business clients. Fintech companies supply the technology and services that help these merchants process payments efficiently.

A payment service provider (PSP) is a company (such as PayPal or Stripe) that handles digital financial transactions for a merchant. Often called a payment aggregator or an intermediary, PSPs are the quickest way to start accepting payments online. Instead of each business having its merchant account, the PSP uses a single account to handle all its clients’ transactions. PSPs offer services like payment processing, fraud prevention, or currency conversion.

Related: Customer Risk Assessment — How to Do it Right [Step-By-Step Guide]

Why Does the Cardholder’s Transaction Dispute Get Rejected?

If the reasons for a dispute are invalid or cannot be proven, the bank or the card issuer can reject the dispute.

Common reasons why transaction disputes are rejected include instances like:

- The buyer didn’t like the item.

- The buyer forgot a subscription payment was due.

- A household or family member made the transaction.

- The buyer didn’t contact the merchant for a refund first.

Card companies and banks can also reject potentially fraudulent transactions. Similarly, a transaction dispute can be denied if it seems fraudulent. In addition, banks can initiate disputes on behalf of their customers if a transaction raises concerns. In this case, the cardholder might not be aware until the refunded funds appear in their account.

The Step-By-Step Dispute Process

If the transaction dispute process still raises some questions, we’re breaking it down for you in more detail below:

1. The Cardholder Files a Dispute

The person opening the dispute is typically unhappy with the purchase. For this reason, they contact their bank to dispute the transaction. This step is simple, as most banks can be contacted by phone, email, directly through their website, or the banking app.

Other reasons a person disputes the transaction can be that their billing statement had an unfamiliar transaction description, there were duplicate charges, their card was used without permission (fraud), and other complaints we’ve discussed above.

As a response, the merchant is then often required to provide detailed evidence showing they fulfilled the order on their side by providing different details, such as:

- Transaction receipts.

- Proof of delivery, like a delivery receipt or confirmation email.

- Proof of shipping, such as a tracking number or shipping receipt.

- Positive Address Verification System (AVS) response.

- Any communication evidence with the customer that supports the completion of the transaction.

2. The Issuer Examines the Cardholder’s Claim

The issuer is reviewing the cardholder’s claim to determine its validity.

There can be two outcomes:

- The transaction dispute is valid. In this case, the issuer needs to refund the cardholder. The funds will come from the card company’s dispute process (the issuer recovers the money from the merchant and returns it to the cardholder) or the issuer, who is responsible for handling the loss.

- The transaction dispute is invalid. In this scenario, the issuer rejects the cardholder’s dispute and holds the cardholder responsible for the transaction. This often happens when the person files a dispute too late and not within 60 days of the statement date.

If a chargeback is issued, additional steps can be involved. For example, if it’s friendly fraud, the merchant can submit a detailed argument with evidence in order to try and recover the lost revenue.

3. The Issuer Initiates the Chargeback

A chargeback is filed only after all other resolution methods haven’t worked out between all parties. That’s because dispute analysts will try other methods to resolve this issue before resorting to a chargeback.

After the final decision is made, the chargeback dispute is closed, and the losing bank must pay all the process fees:

- If the cardholder wins, the provisional credit to their account becomes permanent, and the bank removes the temporary credit from the merchant’s account to refund the issuer. The merchant is responsible for paying the fees.

- If the merchant wins (this is rare at this stage), the provisional credit to the merchant’s account becomes permanent, and the issuer reinstates the transaction on the cardholder’s account, covering the arbitration fees.

Disputes should be resolved as quickly as possible. For example, Visa has a 30-day policy, and Mastercard has a 45-day policy. In practice, if the dispute escalates, it can take several months for it to be resolved.

How to Prevent a Transaction Dispute?

As transaction and dispute volumes increase, managing them becomes more challenging. Card brand regulations list various reasons for disputes, including criminal fraud, friendly fraud, and merchant error. Although criminal fraud appears to be the biggest threat, friendly fraud is also a major concern for merchants. Some customers often mistakenly think the dispute process is the same as receiving a refund.

Despite that, banks tend to agree on disputes with the cardholder if the complaint seems valid to keep customer trust. But the issue is that customers who win a dispute are more likely to repeat this kind of behavior. So, merchants often don’t agree with invalid disputes since they cost a lot of money.

While it’s impossible to eliminate disputes entirely, businesses can use strategies to reduce them and minimize losses by:

- Improving their chances of successfully resolving disputes.

- Reducing the number of customers seeking disputes through clear policies and item descriptions.

- Implementing AI-powered fraud prevention tools that spot suspicious behavior patterns.

Managing disputes involves two key steps: preventing as many disputes as possible and addressing the disputes. This includes implementing a dispute mitigation strategy that includes minimizing errors and using automated iDenfy to eliminate threats. Otherwise, neglecting dispute management can lead to negative customer reviews, increased fraud risk, and a damaged reputation, potentially resulting in future losses.

To explore your specific case in detail, let’s discuss how our fraud prevention suite (KYC/AML/KYB RegTech tools) can help minimize disputes and detect fraud in real-time.