Over the years, Anti-Money Laundering (AML) initiatives have aimed to increase the difficulty of concealing illicit profits. Despite AML regulations mandating that financial institutions create advanced customer due diligence strategies for evaluating money laundering risks and spotting suspicious transactions, non-compliance cases continue to rise annually.

Initially, AML regulations primarily targeted banks and similar entities. However, they have expanded their reach to encompass a wide range of institutions. This includes not only traditional banks but also iGaming platforms or cryptocurrency exchanges.

While various AML guidelines and regulations exist worldwide, AML programs typically consist of five fundamental pillars. We’ll explore what exactly these five pillars are and learn how they can help your organization stay compliant.

What is Anti-Money Laundering (AML) Compliance?

Anti-money laundering (AML) compliance encompasses a network of laws, regulations, and processes designed to unveil attempts to disguise illegal funds as lawful income. Money laundering is the practice of concealing various criminal activities, spanning from minor tax evasion and drug trafficking to instances of public corruption and the funding of organizations labeled as terrorist entities.

The Bank Secrecy Act (BSA) mandates that financial institutions must create AML programs to effectively combat illicit activities. In the UK, the Money Laundering Regulations (MLRS) and in the US, the Anti-Money Laundering Act of 2020 help companies establish comprehensive AML programs with standard guidelines, assisting them in safeguarding both themselves and their customers from crime.

Related: AML Compliance Program — Step-By-Step Guide in 2023

Automate your AML checks

Screen customers against global sanctions, PEPs, and watchlists in real time with iDenfy AML Screening.

Explore AML ScreeningWhat are the Pillars of an AML Compliance Program?

While the BSA specifically applies to the United States, the five AML pillars are recognized internationally. That means businesses globally employ them when developing their own AML compliance programs.

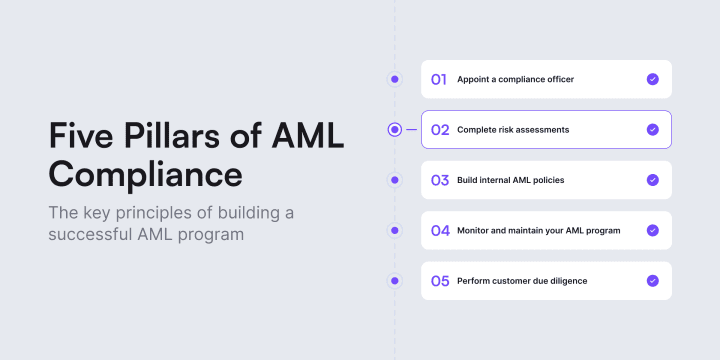

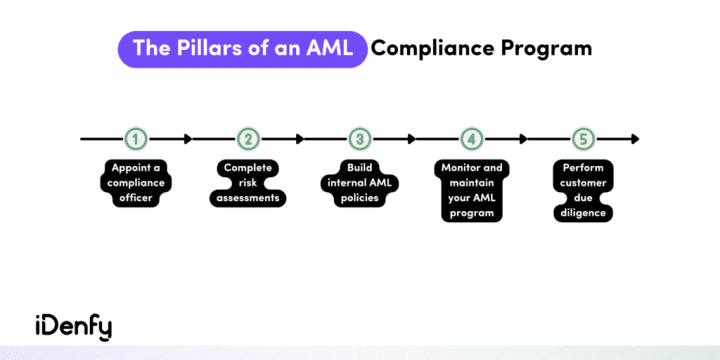

The five pillars of AML compliance offer a holistic approach, emphasizing internal controls, assigned roles, training and awareness, independent testing, and a risk-based strategy for ongoing Customer Due Diligence (CDD).

The five pillars of AML consist of:

- Designating a compliance officer

- Completing risk assessments

- Building internal controls and AML policies

- Monitoring and auditing your AML program

- Performing CDD

Below, we’ll review the five pillars of AML compliance in more detail.

1. Designate a Compliance Officer

The first step is to find a person in your company who would be responsible for the whole AML program. A designated compliance officer’s duties consist of ensuring compliance and, at the same time, sharing and updating their AML expertise with the whole company. They typically assess existing processes, create new processes, and ensure that the revised strategy aligns with all current AML regulations and is effectively implemented in your company.

Other compliance officer duties include:

- Recommending modifications based on audit findings

- Training and updating staff members on compliance regulations and changes

- Communicating these changes to stakeholders and management

It’s important that the designated compliance officer has a deep understanding of the industry your company operates. They also serve as the main point of contact for regulatory authorities.

2. Complete Risk Assessments

To have a robust AML compliance program, you must establish clear protocols, controls, and procedures for detecting financial crimes. Your compliance measures should also follow a risk-based approach. That’s why you must tailor your mitigation measures based on the level of risk. That’s because each organization operates differently, and policies must incorporate customized strategies.

In practical terms, these AML compliance controls should include various measures. For example, customer identity verification, screening and monitoring, as well as the ability to report suspicious activities to the relevant authorities. Keep in mind that risk assessments are not static. They should be periodically reviewed and updated to account for changes in the institution’s operations, regulatory environment, and evolving risks.

Companies often manage their risks by implementing these processes:

- Identification. You should identify and understand the specific risks your company faces in terms of money laundering and terrorist financing. This involves analyzing your operating industry, products, services, customer types, and geographic regions to help you pinpoint potential vulnerabilities.

- Assessment. Once you identify the risks, you should assess their potential impact. An effective risk assessment helps prioritize risks and allocate resources effectively to address the highest-risk areas.

- Customer risk profiling. Often, part of the risk assessment involves categorizing customers into different risk levels. High-risk customers, such as politically exposed persons (PEPs) or customers from high-risk jurisdictions, require a higher level of scrutiny — enhanced due diligence (EDD).

- Transaction monitoring. Banks, financial institutions, and other companies implement systems and processes to monitor transactions in real-time. That’s because you must flag and report suspicious transactions for further investigation.

3. Build Internal Controls and AML Policies

To effectively manage risks, it’s crucial to establish a well-defined compliance department. That means staying informed about emerging market trends and new compliance regulations. For instance, many financial firms now embrace environmental, social, and governance (ESG) policies to align with customer expectations.

Every member of your team, regardless of their role, should know how compliance impacts their job, especially those in customer-facing positions and those responsible for fraud detection. They should also receive training on the tools and applications used for fraud detection and be familiar with the procedures for reporting fraudulent activities.

Of course, numerous external organizations offer training programs, so you don’t need to handle all training in-house. Importantly, training should not be a one-time event. Your designated AML compliance officer should ensure regular refresher training whenever updates or changes are made to your AML compliance program.

Related: What is an AML Risk Assessment? [With Examples]

4. Monitor and Audit Your AML Program

Not only internal training and monitoring of AML programs are crucial, but also conducting regular auditing of your compliance program by independent third-party entities. That’s because a proper evaluation of an institution’s compliance cannot rely solely on internal testing. These regular third-party audits help identify potential vulnerabilities in your compliance program. Keep in mind that they are essential to uphold operational integrity.

It’s important to note that these compliance audits are distinct from financial audits. They solely concentrate on AML regulations and the company’s efforts to safeguard against criminal activities. Annual audits are a bare minimum, but institutions facing elevated money laundering risks should keep up with a more frequent auditing schedule. That’s how your independent auditing will help identify outdated practices and streamline AML processes. It plays a critical role in identifying weaknesses, improving practices, and demonstrating compliance with regulatory authorities.

Related: What are the Key AML Laws in the US? [Business Guide]

5. Perform Customer Due Diligence (CDD)

In May 2018, the Financial Crimes Enforcement Network (FinCEN) implemented the Customer Due Diligence (CDD) rule. Today, it’s become one of the five fundamental pillars of AML compliance. The CDD rule obliges companies to identify and verify the identity of their customers and continuously monitor their activities to detect and report any suspicious transactions.

In general, performing CDD consists of four core elements:

- Verifying the identity and assessing the risk level of each customer.

- Identifying the beneficial owners of legal entities.

- Understanding the nature of customer relationships.

- Continuously monitoring transactions to detect any suspicious behaviors or patterns.

The CDD rule recommends a risk-based approach, where organizations assess both customers and transaction requests based on their level of risk. Assessing the risk associated with each customer and transaction allows you to customize your due diligence efforts. You should apply enhanced due diligence (EDD) measures when dealing with higher-risk situations. For example, if a customer is from a high-risk area where the risk of money laundering is high, you should apply due diligence measures.

Related: Customer Due Diligence Solutions — How to Build CDD Compliance?

How to Stay AML-Compliant?

If implementing the five pillars of AML, monitoring transactions, submitting reports, conducting regular audits, or training new employees all at once seems too much of a hassle, you should consider implementing AML Screening and other AML solutions, such as risk assessment and risk-scoring tools that can help identify high-risk clients who need extra attention from compliance analysts. With that in mind, AI-powered RegTech software can help you streamline your AML operations while ensuring a frictionless experience for the end customer.

Additionally, it’s essential to regularly update your AML program as new laws are enacted and regulations evolve. Neglecting this could potentially lead you to enormous fines and losses for your business — and we don’t want that.

So, if you need guidance on establishing a strong AML program, our identity verification, AML screening, risk-scoring, and other solutions could help you automate your compliance workflow and reduce the hassle for your compliance teams. Contact us for more info.