The Anti-Money Laundering Act of 2020 (AMLA) introduces nationwide anti-money laundering (AML) priorities and extends AML regulations to various industries. This makes it challenging for regulated entities to stay ahead of ever-changing regulatory rules, especially due to multiple AMLA provisions, such as the creation of a federal registry for beneficial ownership.

Many consider AMLA the most impactful AML legislation passed in decades. It holds crucial implications for compliance professionals and has marked a new era in AML compliance in the United States since 2004. In this article, we discuss the essence of AMLA and dive deeper into its provisions.

What is the Anti-Money Laundering Act of 2020?

The Anti-Money Laundering Act of 2020 (AMLA) stands as a pivotal piece of legislation in the fight against money laundering, marking one of the most significant enactments of US AML laws in decades. At the same time, AMLA establishes nationwide AML priorities and extends AML regulations to new industries.

Timeline for AMLA

June 2021:

- Publication of national AML/CFT priorities.

- Assessment and proposed rules regarding FinCEN’s no-action letter process.

December 2021:

- Proposed new rules for antiquities dealers.

- Implemented regulations for incorporating national priorities into AML programs.

- Deadline for Beneficial Ownership reporting and implementation of FinCEN Corporation registry.

- Publication of SAR threshold report.

- Final Rule of the program for SAR sharing with foreign affiliates.

- Report on Treasury review of BSA regulations and guidance.

AMLA was passed by Congress in 2021 as a component of AMLA lies the Corporate Transparency Act (CTA). The CTA, nestled within AMLA, grants the Financial Crimes Enforcement Network (FinCEN) the authority to gather beneficial ownership details and share them with relevant parties, including law enforcement agencies. AMLA also updates the AML framework by introducing new amendments to the Bank Secrecy Act (BSA).

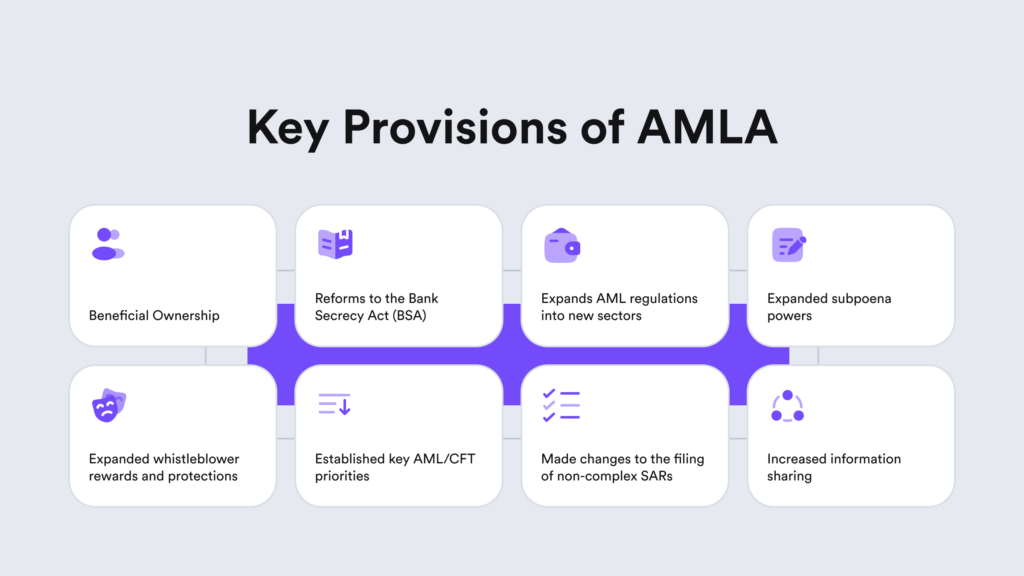

Key Provisions of AMLA

In brief, AMLA made important changes to AML compliance in these sections:

- It broadens the BSA’s definitions of financial institutions covering businesses from other industries, such as cryptocurrency services.

- It mandates businesses to disclose their beneficial owners to FinCEN.

- It modifies the process for submitting non-complex suspicious activity reports (SARs).

- It supplements existing whistleblower protections.

- It forbids the misrepresentation or concealment of certain information from financial institutions and enhances penalties for BSA violations.

- It grants the Departments of Justice and Treasury expanded subpoena powers for foreign bank records.

- It establishes new important priorities in AML/CFT compliance on a national level.

We look into each section in more detail below.

Expands AML Regulations Across New Sectors

AMLA expands BSA to regulate businesses involved in non-traditional exchanges of value, expanding the definition of “financial institutions.” This includes virtual currencies, cryptocurrency exchanges, and other businesses offering currency-substituting services, as well as art dealers or businesses selling antiquities.

That means AMLA specifies that the exchange or transmission of products acting as a substitute for money, like cryptocurrencies and art, must adhere to BSA registration and AML compliance standards. Additionally, the act allows financial institutions to share data on AML and BSA regulations with their international subsidiaries, affiliates, and including those dealing with cryptocurrencies.

Requires to Submit Beneficial Ownership Information

The mentioned section of AMLA called the Corporate Transparency Act (CTA), mandates FinCEN to create and manage a beneficial ownership registry for specific domestic and foreign businesses in the US. A beneficial owner is considered an entity or individual with 25% or more ownership interest or substantial control over the entity.

Before AMLA, the US lacked a secure and confidential non-public national registry for beneficial ownership information. Unlike many other countries, companies were not obligated to disclose this information to a state or federal database.

This provision aligns the US with Recommendation 24 from FATF’s list of 40 Recommendations aimed at combating money laundering. The registry gathers the details about beneficial owners from corporate entities, which should include their:

- Full name

- Date of birth

- Copy of ID

- Residential address

- Business address

Experts warn that the lack of reporting before AMLA has enabled criminals to misuse opaque ownership structures for businesses and their financial transactions. Currently, AMLA restricts FinCEN from disclosing beneficial ownership data except to law enforcement or federal agencies involved in national security or law enforcement.

However, financial institutions can access this information from the database to fulfill customer due diligence (CDD) requirements with the reporting company’s consent.

➡️ What is a Reporting Company?

A reporting company is any private, for-profit entity with fewer than 20 full-time employees and less than $5 million in revenue, not required to register with SEC, CFTC, or a state insurance authority. Reporting companies must provide FinCEN with each beneficial owner’s full legal name, date of birth, current address, and unique identification number from an acceptable document.

Exemptions from the “reporting company” definition:

- Publicly-traded companies

- Entities subject to significant regulatory oversight (e.g., banks, insurance companies, broker-dealers)

- Certain investment funds, charities, and investment vehicles advised or operated by banks or registered investment advisers

- Most corporations and LLCs owned or controlled by exempted entities

- Entities with a physical office presence in the US

➡️ Are there any Changes Regarding the Customer Due Diligence Process?

AMLA specifies that no provision within it should be interpreted as allowing the Treasury to eliminate the obligation for financial institutions to identify and confirm the beneficial owners of legal entities.

Nevertheless, AMLA does instruct the Treasury to amend the CDD regulation within a year of implementing rules to alleviate unnecessary or redundant burdens on financial institutions and their legal entity clients, considering the new registration prerequisites.

CDD Rule Overview:

- Obliged financial institutions must identify and verify customer identities.

- This includes identifying individuals owning 25% or more of equity interests in a legal entity customer.

- Risk-based procedures for verifying identities, aligning with the customer identification program (CIP) rule.

Related: What is the Difference Between CIP and KYC? Examples & FAQs

Develops a Non-Complex SAR Filing Process

As part of its provisions, AMLA mandates FinCEN to create an automated process for filing non-complex suspicious activity reports (SARs). This streamlined approach is designed to help companies accommodate the advanced AML compliance systems used by many financial institutions.

Additionally, AMLA mandates the US Treasury to assess the adequacy of current thresholds for SAR and Currency Transaction Report (CTR) filing requirements in order to make adjustments if necessary.

Expands Protections for Whistleblowers

AMLA shields whistleblowers from retaliation when reporting potential money laundering violations or related protected activities, regardless of whether the report is made to the employer or a governmental entity, such as the Attorney General, Secretary of Treasury, or regulators.

Retaliatory actions include threats and other forms of harassment towards the whistleblower, such as:

- Firing or laying off

- Reducing pay or hours

- Refusing overtime or promotion

- Withholding benefits

- Blacklisting and hindering future employment

- Refusing to hire or rehire

- Reassignment to a less desirable role

- Reporting the individual to the police or immigration authorities

- Subtle actions like isolation, ridicule, or false accusations of poor performance

These protections extend to internal whistleblowers who report wrongdoing to their employer rather than the government. Whistleblowers are people who share information about wrongdoing with their employer, either alone or together with others, even if it’s part of their job.

Forbids the Concealment of Certain Information and Enhances BSA-Related Penalties

AMLA enables financial institutions to share AML/BSA-related information with their foreign branches, subsidiaries, affiliates, and partners. It formalizes previous guidance allowing financial institutions to collaborate in sharing information with each other to identify potential suspicious activity and improve AML/BSA compliance.

AMLA also introduced new criminal BSA violations related to intentionally deceiving or withholding information from financial institutions, including:

- Knowingly concealing, falsifying, or misrepresenting material facts about the ownership or control of assets in a monetary transaction if the person or entity owning or controlling the assets is a senior foreign political figure and the value of the assets is at least $1,000,000.

- Knowingly concealing, falsifying, or misrepresenting material facts about the source of funds in a monetary transaction that involves an entity identified as a primary money laundering concern and violates a prohibition on opening or maintaining a correspondent or payable-through account.

Violation of either law can result in up to 10 years of imprisonment, a fine of up to $1 million, and potential forfeiture of funds involved in the crime. Furthermore, individuals associated with financial institutions risk losing bonuses through clawback if found guilty of BSA offenses.

Creates Broader Subpoena Power Over Foreign Banks

AMLA allows the US Treasury and Department of Justice to get records from foreign banks during criminal investigations. Before AMLA, US law enforcement agencies could only subpoena foreign banks with correspondent accounts in the US regarding transactions processed through those accounts.

Unlike before, the subpoena isn’t limited to records linked to the correspondent account. After AMLA, foreign banks with correspondent accounts in the US can be subpoenaed for information on any account under AML investigation. That means it can cover any account at the bank, including outside the US. If a foreign bank doesn’t follow a subpoena, it could face contempt charges and a penalty of up to $50,000 for each day it doesn’t comply with the subpoena’s terms.

While this law focuses on fighting money laundering, it also targets other crimes like corruption, tax evasion, or drug trafficking. These changes also make it easier for federal investigators to get foreign bank records without relying on international treaties. People at foreign banks who get these subpoenas can’t tell anyone named in them about it. Breaking this rule could lead to a civil penalty of double the suspected criminal proceeds sent through the bank’s correspondent account in the related investigation.

Establishes Key National AML/CFT Priorities

AMLA introduces several provisions affecting companies’ BSA/AML programs, including the change that FinCEN must share information regarding ways to combat money laundering and terrorism financing.

On June 30, 2021, FinCEN released a list of AML/CFT priorities:

- Corruption

- Cybercrime (covering cybersecurity and virtual currency)

- Fraud

- Foreign and domestic terrorist financing

- Transnational criminal organization activity

- Drug trafficking organization activity

- Human trafficking and smuggling

- Proliferation financing

At the same time, the Treasury must establish national AML priorities that must be updated at least once every four years. Federal regulators then assess whether and how financial institutions have included these national priorities in their risk-based programs.

The Impact of AMLA on AML Compliance Programs

AMLA, spanning over 1,500 pages, is considered a major turning point in the modern US AML law landscape. As some provisions are still pending implementation, AMLA has already brought some key changes to financial institutions’ compliance programs.

Some key AMLA factors that shape the company’s AML compliance approach:

- AMLA modernizes BSA and other AML laws.

- Financial institutions should constantly inform stakeholders (such as foreign affiliates or compliance specialists) about evolving regulatory compliance changes and potential impacts on daily operations.

- These new provisions require rulemaking, reports, and analyses on the financial institution’s side, which can be a complex task without automation.

For example, the mandated AML/CFT priorities must now be integrated into existing risk-based compliance programs. Additionally, the heightened regulatory oversight, establishment of national AML priorities, and introduction of a beneficial ownership database necessitate more robust compliance programs.

At iDenfy, we help businesses simplify AML compliance with a full RegTech service package in one place, including AML screening solutions for PEPs & sanctions checks, as well as watchlist screening. Other available tools on the same dashboard include bank verification (for EU companies), identity verification, Know Your Business (KYB) verification, and more.

Chat with us for advice and a free demo — all tailored to your specific use case.