A risk-based approach in AML compliance requires investing in appropriate measures to prevent financial crime. However, companies must decide which processes they want to deploy on their own. That means compliance guidelines have specific frameworks that leave flexibility gaps for companies to choose which KYC and AML measures are best suited to their needs.

To implement a risk-based approach, financial institutions must conduct an anti-money laundering risk assessment for each customer. This leads to developing a customer risk profile, also known as customer risk scoring, which necessitates carrying out customer due diligence (CDD) procedures.

Summary:

- The definition of a risk-based approach

- A risk-based approach in the context of AML compliance

- Different examples of a risk-based approach

- The benefits of following a risk-based approach

- Crucial steps for businesses to implement their own RBA

What is Anti-Money Laundering (AML) Compliance?

Anti-Money Laundering (AML) compliance refers to a regulatory framework that consists of laws and regulations explaining measures that financial institutions and other regulated industries must take to prevent financial crime, such as money laundering.

A risk-based approach to AML compliance requires banks, financial institutions, and other regulated entities to thoroughly evaluate potential risks. This involves gaining a thorough understanding of your customers (this is where KYC comes in) – examining the specifics of their operations, industries, and characteristics, no matter if they are potential or existing clients.

Automate your AML checks

Screen customers against global sanctions, PEPs, and watchlists in real time with iDenfy AML Screening.

Explore AML ScreeningGlobal Compliance Regulations for a Risk-Based Approach to AML

The term risk-based approach to AML was first mentioned in 2020 when presented by the UK Financial Services Authority (FSA), now known as the Financial Conduct Authority (FCA). It was further defined in 2012 by the Financial Action Task Force (FATF) in 2012. Since then, the concept of proactive risk management has been introduced, emphasizing the implementation of appropriate security measures to help effectively manage various crime risks.

In general, there are several AML regulatory bodies in different jurisdictions. As a result, businesses must be aware of local and global regulations when ensuring AML compliance. For example, the FATF covers more than 200 countries and jurisdictions. It’s also one of the leading inter-governmental bodies that set new laws and policies to achieve regulatory reforms.

Do All Financial Institutions Follow the Same Risk-Based Approach?

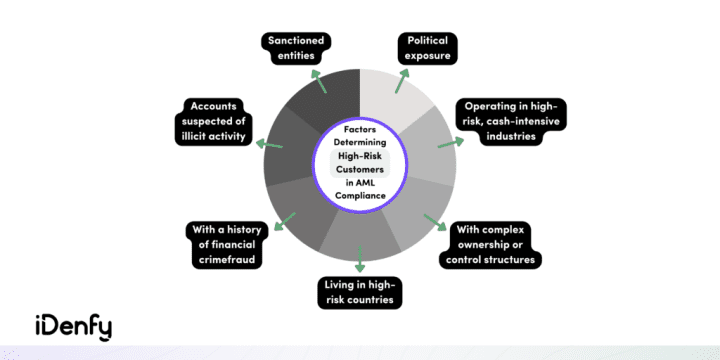

AML compliance is closely tied to a risk-based approach as it focuses on tailoring measures to effectively mitigate the specific risks a financial institution may face. However, financial institutions have different environments, so a risk-based approach can’t be a standard process that’s identical for all regulated bodies.

As an illustration, let’s imagine that two banks are committed to AML compliance, but their risk-based approaches differ based on their customer profiles and the inherent risks associated with their operations. The first bank can tailor its AML measures to the lower risks it faces, while the second bank can adopt a more rigorous approach due to the higher risks associated with its international trade financing activities.

That’s why it’s important to correctly implement processes in your AML compliance program, especially in relation to the risk-based approach and its control processes related to the assessed risk levels of customers.

A Risk-Based Approach to AML Examples

We can demonstrate the differences in risk-based approaches using two customers as examples:

#1 Investment Bank Customer Profiles

Consider an investment bank that deals with high-net-worth individuals and small business owners. The bank has performed risk assessments on its customers and identified two distinct profiles:

- Customer A, who’s a high net-worth individual, is an investor and entrepreneur (Monthly Income: $200,000; Monthly Expenses: Varying based on investments and lifestyle)

- Customer B, who’s a small business owner, running a local coffee shop (Monthly Income: $8,000; Monthly Expenses: Mostly fixed, covering shop rent, employee salaries, etc.)

In this scenario, the investment bank recognizes that the spending patterns of these two customers differ significantly due to their occupations and income levels. While high spending from Customer A might be related to investment activities and lifestyle, similar spending from Customer B could raise suspicions of unusual activity. The bank adjusts its monitoring processes to account for these differences, ensuring that actions taken align with the perceived risk level.

#2 E-Commerce Platform Users

An e-commerce platform assesses the risk associated with its users’ transactions to prevent fraudulent activities. Here are two user profiles:

- User A, who’s an online business owner, sells electronic products (Average Monthly Revenue: $90,000; Monthly Expenses: Purchase of electronics, packaging, and shipping)

- User B is a freelance graphic designer offering design services (Average Monthly Revenue: $3,000; Monthly Expenses: Software subscriptions, utilities, marketing)

The e-commerce platform recognizes that User’s A higher revenue and corresponding expenses are justifiable given their business type. However, if User B suddenly starts making high-value transactions that are out of line with their established income and expense patterns, this could raise red flags for potential illicit activities.

So, this leaves us with the consensus that in both examples, the risk-based approach involves tailoring monitoring and processes based on customers’ characteristics, behaviors, and risk levels. This ensures that suspicious activities are appropriately identified, investigated, and reported.

Why is it Crucial to Have a Risk-Based Approach to AML?

It’s important to adopt a risk-based approach to AML because it helps prevent non-compliance fines, which can lead to millions in damages. Apart from reputational loss, loss of revenue, and other issues that happen when illegal transfers happen, RBA helps businesses minimize the amount that’s already happening or prevent crime in general.

In a practical sense, businesses can be triggered by this approach since it requires additional time, funds, and effort toward risks that hold greater danger and higher potential for harm. However, to protect yourself and your business, you are obliged to know your customers very well so that you can build an effective risk-based approach strategy.

To illustrate, consider the KYC risk-based approach. It helps build a seamless customer onboarding process by adapting the identity verification flow according to the customer’s risk level. Customers with low-risk profiles can be quickly verified, while those with higher-risk profiles undergo extra KYC verification steps.

How to Implement a Risk-Based Approach to AML?

Implementing a risk-based approach means that the business should identify the highest compliance risks and make them a priority. To achieve this, you should create controls based on the potential level of damage they can do to your organization.

In simple terms, you can think of a risk-based approach as managing any regular risks in your company. For example, in drug development, a risk-based approach is used during clinical trials. Researchers assess the potential risks and benefits of a new drug candidate. Trials are designed to focus more on monitoring potential adverse effects in the early phases, where risks are higher, and adjustments are made accordingly.

In the context of AML compliance, the principles are the same. We explain the main steps that you should take below:

1. Perform a Risk Assessment

In order to implement a proper risk-based approach to AML, you’ll need to consider several risk factors. This includes asking yourself questions based on the customer’s geography, vulnerabilities, infrastructure, and regulatory requirements:

- To what extent is this customer susceptible to money laundering, considering the locations of their business operations?

- Is there a possibility that this customer could face money laundering risks?

- Are there any internal vulnerabilities that could facilitate money laundering activities?

- Is this client in full compliance with all regulatory requirements?

You should also consider not only customer risks but also evaluate your business risks related to the potential money laundering through products and services. Important factors include your operating industry, the services and products you offer, the jurisdictions you operate within, your average transaction size, your average transaction volume, the number of customers you’ve already identified as high-risk, and how you acquire customers.

2. Determine Risk Profiles

As the next step to determining your company’s money laundering risks, you should additionally check the level of risk posed by each customer who requests to open an account. You can begin by assigning an ‘unknown’ level of risk until review allows the assignment of a ‘low’, ‘medium’, or ‘high’ level of risk.

To determine the customer’s risk profile, businesses should use a similar table of factors like:

- The industry they operate in.

- The jurisdictions where their operations are located.

- The jurisdictions where their clientele is situated.

- The range of products and services they provide.

- The nature of transactions they engage in.

- The categories of companies they interact with.

- Ownership and operational details of these companies.

- The involvement of third-party entities in their operations.

Building an effective AML compliance program involves identifying potential risks, determining p risk profiles, and building an action plan corresponding to the risk levels for that specific institution. Since not all organizations are inclined to engage with all types of businesses, setting your criteria will help concentrate on threats aligned with the actual risk profile.

The main resource for helping you set grounds for your company’s regulatory frameworks is the FATF, which provides valuable information and the advantage of a global perspective on money laundering. While the FATF itself doesn’t create laws or regulations, it explains the best practices. More importantly, its recommendations influence the design of future jurisdiction-specific implementations.

🧷 Related: AML Compliance Program: Step-By-Step Guide in 2023

3. Choose Effective Risk Controls

After you complete the risk assessment and determine the risk profiles, your risk-based approach to AML should lean towards choosing the most appropriate controls to mitigate these risks. Once you set your risk-based approach in place, it should be less complicated to include any new information as things go on.

For instance, if someone with an unusual background wants to create an account on your platform without a strong risk-based approach, they’d be treated as a unique case. By comparing the customer to the determined risk profiles, you can instantly see if they fit the rules you’ve set beforehand.

However, it’s important to choose effective solutions to control risks based on their effectiveness. These measures should guarantee the appropriate level of scrutiny: heightened security for high-risks and reduced friction for low-risk customers.

Elements for an Effective Risk-Based Approach

To have an effective risk-based approach to AML, you will need to implement the following elements:

Know Your Customer (KYC)

KYC guidelines obligate you to verify client identities. That means organizations must collect and verify users’ personal data, such as name, address, and birth date, as well as, in extra cases, more detailed financial data, such as occupation, transaction history, and more.

The new industry standard is to have automated KYC solutions that could verify and onboard large volumes of clients automatically while still ensuring high accuracy rates. Depending on the customer’s risk profile, popular identity verification measures include: Document Verification, Biometric Verification, Video Identification, Phone Verification, and Address Verification.

Customer Due Diligence (CDD)

Not every customer poses the same level of money laundering risk to your organization. However, the biggest challenge for companies is to continue the CDD processes after they onboard their customers. Companies must consistently evaluate the risk level posed by each customer.

Different data and signals showcase the customer’s risk level. That means you should choose the level of due diligence accordingly, either standard, simplified due diligence, or enhanced due diligence.

🧷 Related: What is the Difference Between CDD and EDD?

Watchlist Screening

A risk-based approach includes screening your customers against various global crime lists to build a more comprehensive approach when it comes to security and compliance. Screening the customer helps you determine if you want them to be associated with your business.

The main elements in this part of the process include:

- Watchlist Screening: It compares people and entities to watchlists for potential risks or matches with sanctioned or high-risk individuals. These lists are made and updated by government and law enforcement agencies.

- Adverse Media Screening: It’s the process of checking news and public information sources to identify any negative or potentially risky associations related to individuals or entities.

- PEPs and Sanctions Screening: PEPs (Politically Exposed Persons) hold prominent public positions, and sanctions involve restrictive measures against those involved in illegal or risky activities. Screening ensures that businesses avoid engaging with individuals or entities that might pose financial crime risks.

Taking all this into consideration, embracing a risk-based approach to AML is absolutely necessary. Despite that, building an AML compliance program from scratch can be a long and exhausting process.

At iDenfy, we help you ensure compliance without the hassle. See our automated KYC/AML solutions in action, or book a demo to find out more.