Know Your Business (KYB) is a process that verifies the legal status of a business and its compliance with Anti-Money Laundering (AML) regulations. Regulated entities must perform KYB verification to protect their interests. This background check prevents forming ties with shell companies or any illegally operating organizations.

In brief:

- To ensure that they are working with legitimate businesses that operate within the law, financial institutions such as banks and fintechs must perform both KYC and KYB checks.

- This process helps companies understand potential business partners and those with whom they want to start a business relationship.

KYB, in particular, takes this step further by additionally requiring companies to establish UBOs. This layer of security enables businesses to determine who directly benefits from the company’s profits, making it harder for criminals to conceal their illegal funds. In the B2B field, this is very important, as companies need to do background checks on the other entity’s shareholders, company owners, directors, suppliers, or third-party vendors.

What is Know Your Business?

The Know Your Business (KYB) process is designed to verify another company by confirming its legitimacy through multiple important data points. This often includes verifying the company’s registration number, license, physical address, shareholder information, source of funding, and so on. KYB is part of a bigger AML framework that aims to detect fraud and prevent illicit activities that can come with B2B relationships, such as money laundering using shell companies.

Verify businesses, not just people

Automate company verification, UBO checks, and business due diligence with iDenfy KYB.

Explore KYB SolutionWhy is KYB Verification Important?

Using KYB verification services is critical to detect fraudulent activity among corporate clients effectively and prevent partnering with non-compliant businesses or those that are too much of a risk based on your internal AML risk assessment.

The key reasons why businesses implement KYB checks include:

- A proper process for identifying business owners, shareholders, or individuals attempting to conceal illicit funds through hidden corporate structures.

- A better way to understand the legitimacy of another company, which then helps companies identify legitimate corporations and non-compliant or high-risk entities.

For example, it’s illegal to partner with a sanctioned entity. That’s why during KYB verification, businesses conduct AML screening, scanning various sanctions lists, among other procedures aimed at detecting crime, including ties to money laundering. Since corporate clients are more complex to deal with than individual customers, KYB helps establish a more thorough understanding of the other company.

How is Know Your Business (KYB) Linked to Know Your Customer (KYC)?

Both processes are designed to verify accounts before starting a business relationship. KYB is designed for corporate entity onboarding, while KYC verification is aimed at individual clients.

However, KYB is much more complex and involves KYC as part of its framework because you need to identify and verify separate people, like Ultimate Beneficial Owners (UBOs), directors, etc., overall determining the corporate company structure. This helps improve risk management and determine if the company is the right fit in terms of a new partnership (for example, you’re an e-comm platform looking for a new payment provider, even then, it’s best to do a quick KYB check).

Related: KYB vs KYC — What is the Difference? [Explanation Guide]

How Do KYB Checks Help With Compliance?

KYB checks help firms assess the suitability of a business by answering the main question — if it’s worth (and safe) to start a new business relationship with that entity. Ultimately, KYB compliance is the process of doing your due diligence on another entity and finding the risks that can be linked with that business.

In KYB compliance, the company and its people need to be verified and assessed, and then categorized based on their risk profiles. That’s because an entity’s ownership structure can be colorful in the sense that it consists of various persons of significant control. These include Politically Exposed Persons (PEPs) and Ultimate Beneficial Owners (UBOs), who are often automatically classified as high-risk customers. An individual can become a PEP, or they can get sanctioned due to changes in the geopolitical environment.

Related: What is the Difference Between CDD and EDD?

The History of Know Your Business Compliance

AML compliance in the US goes back to the Bank Secrecy Act (BSA) of 1970. It includes tracking suspicious activity, scrutinizing foreign transactions, and reporting cash transactions over $10,000, which are regulations we observe today.

Fast-forward to 2001, when the world was shocked by the 9/11 events, and we faced another significant AML compliance requirement with the Patriot Act. It obliges financial institutions to collect information on individuals holding or opening new financial accounts.

However, the Panama Papers scandal exposed the Patriot Act’s limitations. We learn that enhanced due diligence measures were ineffective in stopping the rogue offshore finance industry from using illegal funds. To address this issue, in 2016, the government introduced new requirements specifically for onboarding business customers, known as KYB.

What are Some Examples of Regulations for KYB Checks?

KYB requirements are not universally standardized and may differ based on where you do business. That said, key ones include:

- The CDD Final Rule

- The Bank Secrecy Act (BSA)

- EU’s Anti-Money Laundering Directives, as well as

- The Financial Action Task Force (FATF)

- The Financial Crimes Enforcement Network (FinCEN)

KYB regulations have one goal. And that’s to improve financial transparency and help uncover criminals who use companies to hide illegal activities. For example, the CDD Final Rule aims to do so by requiring companies to identify and verify beneficial owners. These are the people who are responsible for a company, either by owning shares or having voting rights, ultimately benefiting from the business when it opens an account..

Related: Global KYB Compliance — Top 3 Challenges and Solutions

What Kind of KYB Checks Should Businesses Perform?

The CDD Final Rule doesn’t describe the exact steps for carrying out KYB checks. However, there’s a standardized approach that most businesses follow if they are regulated and need to follow KYB requirements strictly. This includes conducting AML screening (PEPs, sanctions, and adverse media and watchlist screening), UBO identification and verification, as well as conducting ongoing monitoring to detect AML red flags or changes in the company’s risk profile.

KYB also includes basic screening of the company. This includes verifying:

- The company’s legal name

- The company’s operating address

- Business registration status

- Licensing documentation

To summarize: know your business checks are not a uniform checklist that applies identically to every company. The scope and depth of these know your business checks should scale with the risk profile of the entity being onboarded.

A low-risk domestic supplier with a clean, publicly available corporate record requires far less scrutiny than a holding company registered in a high-risk jurisdiction with a complex UBO structure. In contrast, large corporations and complex corporate structures with hidden UBOs and ties to Russia need extra attention and evaluation to determine if the entity is transparent and worth partnering with.

Related: 6 Steps to Conduct a Know Your Business (KYB) Verification Check

What is Required to Verify a Company in Practice?

As a regulated entity, you must assess the risk associated with your business relationships by conducting due diligence for each potential customer. And for that, you need to collect multiple documents and verify concrete business data. So, while KYB onboarding might seem pretty simple for some, it’s actually way more complex.

The key steps include:

1. Verifying Licensing and Registration Details

This includes reviewing official government databases and conducting document checks to see if the entity is registered and has a license. In general, the company that’s being verified should also provide detailed information to simplify the KYB verification process. Avoidance or lack of cooperation should be treated as a red flag.

Related: The Main KYB Risk Factors You Should Know

2. Conducting Due Diligence

It’s the process of evaluating the level of risk associated with a potential business relationship. Unlike customer due diligence, which involves verifying a customer’s identity, due diligence for businesses entails determining the company’s UBOs. If the UBO poses a higher risk, the company should follow enhanced due diligence (EDD).

3. Verifying Ultimate Beneficial Owners (UBOs)

A thorough understanding of a company’s ownership structure is essential. All of the company’s UBOs must be verified through standard KYC checks. This helps identify the entity’s owners and detect fake or altered documents that might hide illegal or, sometimes, shady and hidden corporate structures.

4. Sanctions Screening

It’s the process of identifying and verifying if sanctions imposed by regulatory authorities prohibit the potential business relationship. During KYB, the process of screening sanctions lists is important, as it involves checking whether the company or its employees are listed on any sanctions lists.

Related: The Complete Sanctions Screening Guide

5. PEP Screening

It’s the process of assessing any potential risks related to individuals and their links to political corruption. That means that during KYB, regulated companies need to screen their business relationships to detect any involvement with politically exposed persons (PEPs). Businesses with a positive PEP status pose a higher level of risk due to the higher chances of being involved in financial crimes. PEPs are categorized into domestic and foreign PEPs, and, for example, foreign PEPs are treated as high-risk, which means they need to undergo EDD.

6. Adverse Media Check

This means checking negative news and monitoring multiple news outlets and seeing all of the flagged updates (often, based on keyword research) in real-time, allowing companies to respond to adverse media coverage adequately. For example, you can find links to crime, such as the entity’s director being involved in a corruption scandal in the past, which automatically can be a deal breaker for a B2B relationship.

Related: Keywords in Adverse Media — Search & Screening Challenges

Why Does KYB Matter?

Regulatory authorities have discussed over the years that there was a gap left in the compliance landscape, allowing criminals to use various business structures to launder funds more successfully. There was a contrast since, compared to KYC measures (which have been in place since the early 2000s), KYB is a relatively new tactic. Business relationships were subject to less scrutiny than individual ones, allowing criminals to create shell companies that existed just on paper or hide the true ownership structure of a company and use other individual names to launder funds.

Since business records were only briefly verified and assessed, fraudsters could commit fraud and engage in all sorts of illegal schemes without undergoing personal screening, similar to how it all went down in the infamous Panama Papers scandal, where non-compliance reached a new level. Thankfully, FinCEN introduced new beneficial ownership reporting rules and included KYB verification in its CDD Requirements. To this day, this is a very important milestone, as it helped to create standardized and global guidelines on how to verify not only customers but whole corporate entities more accurately.

What are KYB Procedures?

The CDD Rule does not provide specific instructions on how each organization should perform KYB checks. However, even though Know Your Business regulations vary by jurisdiction, general KYB procedures oblige businesses to follow a risk-based approach and perform due diligence.

The KYB process is not a single check but a structured sequence of steps, which has three components at a minimum, similar to how KYC is also based on the principle of the three steps to KYC. These include:

➡️ Business verification. Verifying the business.

➡️ UBO verification. Identifying the company’s ultimate beneficial owners (UBOs).

➡️ Ongoing monitoring. Maintaining updated customer information and monitoring risk on an ongoing basis.

Systematically missing red flags, entities not being put on monitoring lists on purpose, equals non-compliance and strict penalties, which can eventually lead to money laundering cases.

Information Required for KYB Checks

The KYB process entitles companies to comply with AML laws, including the mentioned CDD Rule. To ensure compliance, companies must collect and verify different data points, including:

- Name and business registration status. The company’s legal name and the standing of the business, as well as the licenses and permits (if they are needed to operate in a particular jurisdiction/industry)

- Address. The company’s operating address. Remember that a business operating address might not match the registered address.

- Ultimate beneficial owners (UBOs). This is the identification and verification of shareholders who have 25% or more beneficial ownership in the company.

Regarding Know Your Business checks, it’s crucial to focus on two factors: proper due diligence and a suitable compliance program that will guarantee that you are not doing business with criminals.

➡️ By implementing KYB requirements, companies can avoid conducting business with entities that are involved in unwanted scenarios like sanctions, tax fraud, and, in more severe cases, terrorism financing or money laundering.

Who Needs to Perform KYB?

Financial companies are required by law to conduct KYB verification. The Final CDD Rule states that the following businesses need to follow KYB compliance regulations:

- Commodities brokers

- Mutual funds

- Banks

- Fintechs

- Securities brokers or dealers

- Commodities brokers

- Futures commission merchants

- Other financial institutions

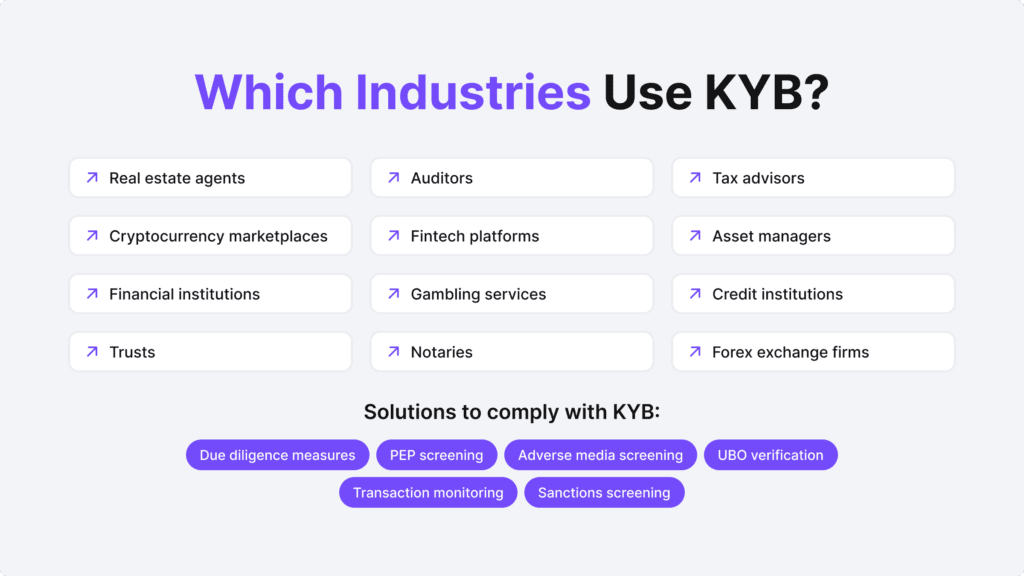

Similarly, according to the EU’s 5th AML directive, crypto marketplaces, gambling operators, tax advisors, auditors, asset managers, credit institutions, notaries, and other financial companies need to carry out KYB checks to maintain compliance. However, there are exceptions where this rule does not apply. For example, verifying the identities of beneficial owners in KYB isn’t required for businesses in regulated markets within the European Economic Area (EEA) or regulated non-EEA markets.

Keep in mind that even though you might not be a regulated business, KYB verification checks are still a good investment in your company’s internal AML risk assessment (or fraud prevention) program. That’s because all businesses need to determine risk factors: both internal and external (in this case, potential dangers linked to a new supplier, for example).

That’s why, even though industries like e-commerce have less strict corporate due diligence requirements, they still need to make sure that all partners or users on their marketplaces are legit and not selling illegal services or fake items. Otherwise, they’re risking major financial losses, especially due to risks like disputes and an increased chargeback rate, which can sometimes lead to the loss of a business license.

Related: Global KYB Compliance: Top 3 Challenges and Solutions [With Examples]

Manual vs Automated KYB

Many compliance officers agree that KYB checks can give you a headache, especially if you don’t automate any processes, such as verifying UBO identities or automatically screening sanctions lists. All processes in KYB verification require companies to collect, analyze, and manage large volumes of data. This includes even the tiniest data pieces, such as the company’s registration number, or more detailed assessments, such as document verification and looking up official documents from at least a few government registries to cross-check information and ensure that it’s legitimate. Depending on the use case, verifying the source of funds or a person’s residential address is also important and time-consuming.

Banks and other regulated entities that have a large number of accounts that need to be onboarded, screened and monitored often choose to implement KYB software simply because it helps analysts save hours and hours of work. There’s no longer a need to search for government databases online, as most solutions have gate-free, connected access to multiple global registries. For example, if you’re operating both in the US and in some EU markets, you’ll probably need to review multiple records. And not every country has a proper register like the UK’s Companies House. Offshore havens like the British Virgin Islands do not require the same amount of information, which often already is a challenge, even if you’re using KYB automation.

While manual intervention is still needed, as it’s practically impossible to proceed with EDD without the touch of a compliance officer, automated KYB workflows simplify processes linked to complex company structures and industry-specific requirements. That’s because automated KYB platforms handle large data volumes, automatically triggering KYC checks for individuals and conducting general background checks on the business in the same dashboard. On top of that, they allow companies to customize their KYB processes, send tailored questionnaires to corporate clients when extra information is required, and conduct ongoing monitoring to receive real-time alerts regarding suspicious activity.

Benefits of KYB

The key benefits that KYB checks provide include:

Better Risk Management

Automated KYB software can detect changes in a customer’s risk profile in real-time, alerting compliance officers to take action more quickly. This makes reporting practices easier and also allows for detecting document fraud or identity theft more accurately since automation screens and verifies data faster. On top of that, it’s a great way to cut costs and focus on high-priority compliance tasks and identify high-risk clients rather than treating all cases manually and the same.

Streamlined Verification Processes

AI-powered KYB solutions can automatically extract necessary information from national and international databases, streamlining document verification procedures, including more complex processes, such as cross-checking client data with different government databases. This is important as multiple documents need to be verified.

For example, KYB software can streamline the collection of general company information, such as Name, registered number, registered office, and principal place of business, including other details regarding the people behind it, for example, KYC verification for all of the board of directors. Besides, local and global regulations differ, and companies with cross-border operations must comply with all relevant countries, which is challenging without KYB automation.

Ensured Compliant Ongoing Monitoring

KYB compliance isn’t a one-and-done task. It requires re-assessing multiple documents and adapting to regulatory compliance changes, which evolve quickly (for example, sanctions lists). Even the lowest risk accounts can develop “bad tendencies” or be used as money mules for money laundering for a commission. On top of that, flagged clients and those who are “high-risk” require periodic monitoring to see if the risk profile changes.

How iDenfy’s KYB Software Can Enhance Your KYB Process

Historically, Know Your Business checks were known for their complexity, especially when discussing manual back-and-forth research and data collection struggles between multiple sources and third-party vendors.

Collecting information, verifying data, and examining beneficial owners lacked a unified system for integrating all these steps. Modern KYB solutions are fully automated, allowing compliance officers to avoid difficult manual screening processes by streamlining their work through automation.

Despite that, compliance remains a difficult task for many companies, especially now that KYB applies not just to banks and financial institutions. So, if you want to meet regulatory KYB requirements without slowing down the efficiency of business onboarding, there’s only one solution, and it’s automated KYB.

If you’re looking for an accurate, fast, and user-friendly KYB verification solution, try out our free demo to check out how automated Business Verification works with iDenfy.

See our customer success stories here.