Perpetual KYC (pKYC) stands out as a relatively new and effective method for safeguarding customers. Adopted by global RegTech solution providers and businesses from various industries, pKYC elevates the traditional identity verification process by implementing continuous Customer Due Diligence (CDD). This approach can regularly re-authenticate users and identify suspicious activities, this way, helping businesses reduce fraud.

What exactly is the pKYC process, how does it work with other compliance frameworks, and is it actually implemented in practice — we answer these and more questions below.

What Exactly is Perpetual KYC?

Perpetual KYC (pKYC) involves consistently updating and verifying customer information. Typically, this is possible due to the use of automated systems driven by AI, ensuring accurate customer records are maintained through a streamlined and real-time verification workflow.

Perpetual KYC checks are designed to confirm the identity and assess the risk status of a client or customer. Unlike a standard Know Your Customer (KYC) program that conducts checks annually or at specified intervals, like customer onboarding, pKYC is based on an ongoing and continuous monitoring approach of individuals and corporate clients.

Automate your KYC process

iDenfy verifies customers from 200+ countries in seconds. AI-powered, compliant, and trusted by 1,000+ companies.

Explore KYC SolutionpKYC’s Relevance in the Market

pKYC solutions are in high demand in the market right now, especially due to an increase in anti-money laundering (AML) fines. Organizations like the Financial Crimes Enforcement Network (FinCEN) are preparing recommendations, and as more strict rules in the regulatory landscape appear, businesses are searching for effective ways, such as pKYC, to minimize financial crime risks at both an effective rate and cost.

Within the financial services industry, there is a consensus that traditional KYC is becoming obsolete and no longer aligns with current needs. You can say that pKYC has surfaced as a strategic response to the constant complexities of the global financial landscape. In the face of growing sophistication in financial crimes, pKYC provides a proactive solution for customer verification.

Key pKYC Components

pKYC goes beyond traditional customer verification methods by using dynamic monitoring and verification methods based on AI-powered tools. This ongoing approach allows businesses to detect and address anomalies or fraud risks more efficiently.

The main components of pKYC include:

- Automated identity verification. Using AI and ML, pKYC automates identity verification processes, minimizing reliance on manual reviews and boosting overall efficiency.

- Real-time alerts. Through real-time monitoring of customer data, pKYC facilitates instant anomaly detection, triggering alerts for immediate action. This ensures swift mitigation of risks and enhances the overall proactive response to potential issues.

- Ongoing monitoring. Unlike traditional KYC, pKYC operates without waiting for scheduled reviews to update customer data. If additional scrutiny is needed, a ‘trigger’ or ‘alert’ initiates the CDD process, activated by factors like suspicious behavior, a new entity designation, or a customer modifying identifying information.

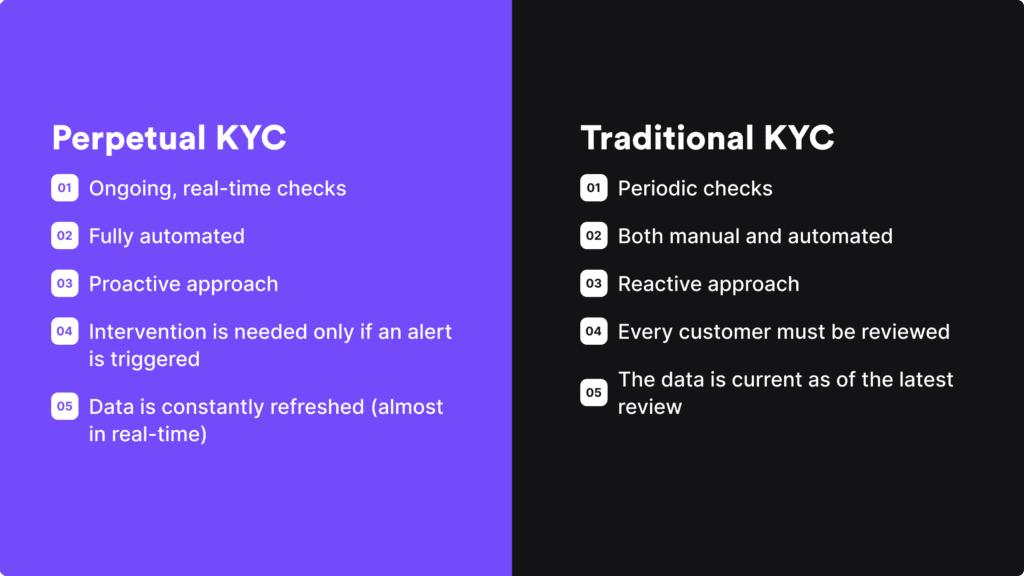

What is the Difference Between Traditional KYC and Perpetual KYC?

Traditional KYC operates at predetermined intervals within the customer relationship, while perpetual KYC adopts a real-time, ongoing approach to due diligence. Unlike traditional KYC, which may involve outdated data, perpetual KYC ensures the continuous accuracy of customer information throughout the entire business relationship.

Traditional KYC has the potential for customer information to become outdated between scheduled reviews, leaving it inaccurate until the next KYC check. This time gap poses a risk of undetected financial crime. This happens because traditional KYC typically occurs during customer onboarding and later at intervals of one, three, or five years, based on perceived customer risk.

In the meantime, pKYC presents a proactive strategy that minimizes fraud risks, improves compliance, and empowers businesses to make well-informed decisions based on current and reliable customer data. Different from standard KYC, which often relies on manual methods or periodic reviews of customer information, perpetual KYC embraces a continuous and automated approach, employing real-time monitoring and automated systems to verify and update customer data.

How does the pKYC Process Work?

Different companies may choose different pKYC approaches. Some opt for re-verifying identity at the onset of every interaction. Alternatively, others use progressive risk segmentation, assessing transaction risks and making verification decisions accordingly. As a company, you also have the flexibility to adjust your pKYC strategy based on your internal compliance procedures.

For example, if you’re operating in a luxury goods market, you may require customer re-verification for high-value purchases. A similar pKYC approach can be applied to age-restricted services or products, such as tobacco and alcoholic beverage marketplaces or adult-oriented streaming platforms that require age verification by law.

However, the foundation of the pKYC process is consistent because it’s based on ongoing monitoring. That means businesses can establish triggers to alert them to any changes that require further investigation of a certain customer.

This could be based on several risk factor categories:

- Suspicious customer behavior

- Inclusion in a watchlist, sanctions list, or PEP list

- Transactions from locations known for high fraud and financial crime rates

This automated pKYC approach enables swift responses to potential threats, preventing issues before they even escalate further. While KYC is sometimes considered a hassle in fintech, where convenience is at the top of the pyramid, customers subjected to pKYC can develop a sense of trust in the platform.

Key Challenges of Traditional KYC Methods

Ongoing monitoring in pKYC involves regularly updating customer information and assessing any changes that sometimes pose risks or compliance issues. However, maintaining this up-to-date data on customer relationships, especially when using traditional, manual YC processes, can create delays and other issues.

Common challenges for businesses include:

- Navigating limited resources

- Determining the frequency of updates and checks

- Building an overly complex KYC process that adds unnecessary friction

Here are some industry-specific examples of traditional KYC and the challenges it brings:

#1: Financial Institutions

Financial institutions, such as banks, often implement KYC processes to comply with AML regulations. This mandates them to regularly update customer information, including address, source of funds, and business relationships, to identify any unusual or suspicious activities.

Challenges:

- Scalability. For large financial institutions with millions of customers, scaling the standard KYC process becomes a significant challenge. The sheer volume of data to be monitored, verified, and updated regularly can strain resources, requiring sophisticated technology solutions for efficient and timely processing.

- Data accuracy. Financial institutions face challenges in ensuring the accuracy and completeness of customer data. Customers tend to forget to update their information, provide inaccurate details, or deliberately withhold information, making it difficult to have a comprehensive and accurate customer profile.

#2: Cryptocurrency Exchanges

Cryptocurrency exchanges also use KYC processes to comply with regulations and prevent fraudulent activities. Here, users must submit government-issued ID documents at sign-up. For ongoing monitoring, crypto exchanges must track transaction patterns, assess risk factors, and be vigilant for regulatory changes.

Challenges:

- Rapid regulatory changes. The cryptocurrency industry is subject to rapid regulatory changes. Ongoing monitoring processes must adapt quickly to new requirements, which can be challenging for exchanges to keep up with. Failure to comply with the latest regulations can result in legal and financial consequences.

- Privacy concerns. Cryptocurrency users often value privacy and may be resistant to providing extensive personal information. Striking a balance between regulatory compliance and respecting user privacy is a challenge for exchanges. Some users can even choose platforms with less stringent KYC requirements, potentially exposing the exchange to higher risks.

Related: How to Choose the Right KYC Provider for Crypto Companies?

What are the Benefits of Perpetual KYC?

Adopting ongoing KYC processes that are the key component of a modern, streamlined approach to pKYC, offers a range of benefits, including:

- Enhanced AML compliance. Implementing perpetua KYC strengthens your risk-based approach (RBA) AML compliance, providing a proactive strategy for identifying and mitigating risks.

- Accurate real-time risk detection. pKYC minimizes the risk of involvement in financial crimes by ensuring that your company promptly receives alerts about any potential red flags.

- Ensured operational efficiency. Compared to traditional periodic KYC checks or manual processes, pKYC requires fewer resources. This efficiency is attributed to its continuous nature and automation, streamlining the verification process. Perpetual KYC helps boost operational efficiencies by reducing dropoffs, as well as streamlining internal compliance processes for a more cost-effective approach.

- Up-to-date data facilitation. Perpetual KYC eliminates the issue of outdated records, ensuring that you always have the most recent and accurate information readily available for your customers or clients. This approach enhances decision-making processes and overall customer relationships.

- Better end-user experience. Perpetual KYC can boost the user experience by ensuring smoother interactions and reducing customer frustration through accurate and up-to-date information.

- Reduced compliance costs. With automated triggers, pKYC has the potential to drive down operating costs. It may even result in an overall reduction in the cost of your compliance efforts, offering a cost-effective solution for businesses.

Keep in mind that for pKYC to be successful, the process requires high-quality data that is well-integrated and meets high compliance standards. This involves dedicating the necessary automated KYC/AML tools, your internal compliance team, and your overall commitment to navigating the change from traditional KYC practices to a perpetual KYC framework.

How to Transition to pKYC?

Before transitioning to pKYC, companies should establish a clear roadmap based on their industry specifics as well as local and global compliance regulations. Despite that, this modern approach to continuous customer due diligence has already shown to be a much-needed upgrade not only for the financial industry but also for other spheres like crypto or e-commerce.

To switch from traditional to perpetual KYC, companies must integrate information from various public and private databases, such as government databases, electoral rolls, and utility bill companies, into their screening processes. This expanded dataset empowers businesses to identify potential discrepancies in customer details, significantly reducing the risk of money laundering.

iDenfy’s Approach to Perpetual KYC

At iDenfy, we provide a comprehensive suite of services designed to alleviate the challenges posed by inconvenient and complex KYC processes. Ourfully automated KYC/AML and KYB tools utilize dependable global data sources, making it seamless for you to transition to a perpetual KYC framework.

PEP and sanctions screening, watchlist screening, adverse media checks, address verification based on utility bill checks, and more — you name it, we can custom-tailor it and ensure that you receive timely alerts regarding any AML changes in customer status on both individual and business clients.

Get started today.