At first glance, most clients show typical behavior and present a normal risk level. However, in practice, risk factors like the customer’s location, type, transaction patterns, or industry can elevate the risk or, more importantly, change over time. That’s why it’s clear — you need to understand certain nuances if you want to build an effective anti-money laundering (AML) strategy that works. For that, we have the AML risk assessment process, which helps companies understand unique customer profiles first-hand while identifying risks that could potentially lead to money laundering.

AML risk assessment is crucial for using a risk-based approach and documenting each client’s risk level through an optimized and compliant AML workflow. Despite everyone knowing the importance of AML compliance, risk assessments raise questions, leaving this complex topic a common discussion in the “non-compliance” section. Of course, navigating different AML requirements across various jurisdictions doesn’t help, either.

So, what does it really mean for a company to address and mitigate potential risks? How do AML risk assessment requirements differ for corporate and individual clients? What kind of due diligence measures are required for this process? We answer these and other questions below.

What is an AML Risk Assessment?

An AML risk assessment is a process designed to determine the likelihood of a customer using the company’s products, services, or the platform itself for money laundering and other criminal activities, such as terrorism financing and tax evasion. In other words, this process measures the risk of each client as a way to minimize chances of being involved in any fraudulent schemes.

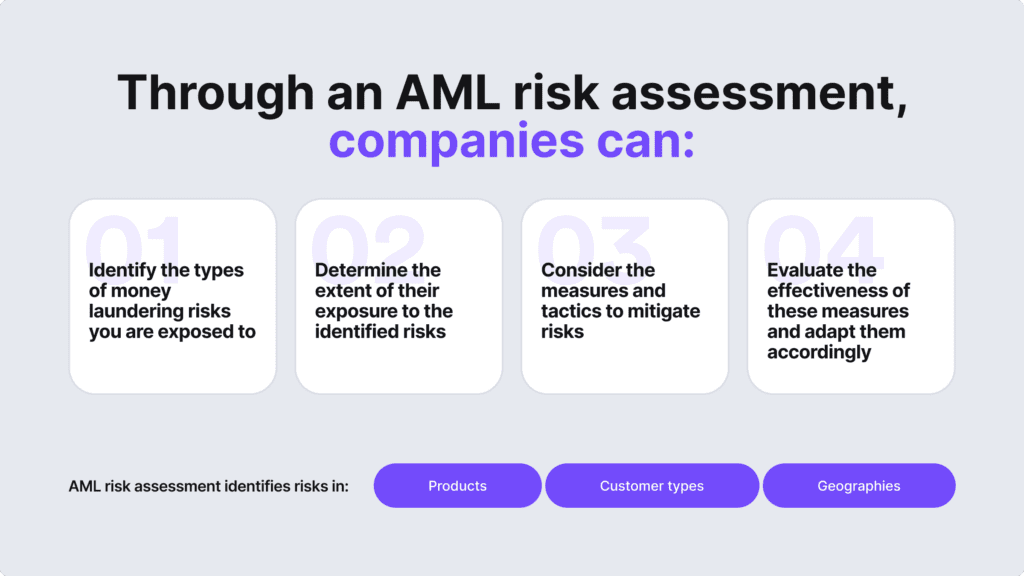

Any company involved in financial transactions should use AML risk assessment to comply with AML laws and regulations, as well as ensure a secure environment by:

- Identifying different types of money laundering risks.

- Assessing the level of exposure to such risks.

- Implementing effective measures to manage these risks.

- Evaluating and enhancing these measures to improve AML risk management.

Companies use AML risk assessment to understand how different types of risks are related. Since there’s no one-size-fits-all approach to risk management, risk factors differ based on the company’s industry. However, common risks that need to be assessed are service risk, customer risk, geographic risk, transaction risk, and product risk.

Automate your AML checks

Screen customers against global sanctions, PEPs, and watchlists in real time with iDenfy AML Screening.

Explore AML ScreeningWho Sets Out AML Regulations?

It depends on the country, however, there are several standards that work like a unified AML approach globally. For example, a known regulatory watchdog, the Financial Action Task Force (FATF), is one of the key players that sets standards for countries to develop and update their AML laws, such as its 40 recommendations.

Other AML compliance requirements worldwide include:

- 🇺🇸The Bank Secrecy Act (BSA)

- 🇪🇺Anti-Money Laundering Directives (AMLDs)

- 🇬🇧The Proceeds of Crime Act (POCA)

- 🇨🇦The Proceeds of Crime (Money Laundering) and Terrorist Financing Act

Related: AML Automation — Streamlined Compliance 101 for Businesses

What are the Key Compliance Processes of an AML Risk Assessment?

Many regulated entities are required to have AML programs in place, which are often based on the five key pillars of AML.

Naturally, a proper AML risk assessment can be broken down into different measures, which your businesses should consider:

- Identity verification. Verifying customer identity during the onboarding process and throughout the whole business relationship to comply with customer identification program (CIP) and Know Your Customer (KYC) requirements.

- Customer due diligence (CDD). Selecting simplified due diligence (SDD) measures for low-risk customers and using enhanced due diligence (EDD) for high-risk clients.

- AML screening. Conducting screening of different AML databases, such as global watchlists, adverse media, as well as politically exposed persons (PEPs) and sanctions screening.

- Transaction monitoring. Tracking and screening client transactions, including keeping data records for reporting suspicious transactions.

- Testing and auditing. Checking, auditing and updating all AML processes in order to keep up with changing regulations.

Related: What is an AML Compliance Program?

What is the Difference Between AML Risk Assessment and Customer Risk Assessment?

The main difference is that the business undergoes a company-wide risk assessment (in this case, an AML risk assessment) while individual clients are specifically obliged to go through a customer risk assessment. Customer risk assessments evaluate their risk of involvement in money laundering and they are a key component of the general firm-wide AML risk assessment, guiding how you evaluate the risk associated with each customer.

Customer risk assessments include the mentioned processes, such as KYC, CDD, AML screening, and transaction monitoring. Analyzing this information is essential for identifying potential risks and implementing a risk-based approach. Through an internal company’s risk assessment, you can better understand your money laundering risks and then finalize your profile through an AML risk assessment in order to address the identified risks.

Related: KYC Risk Assessment: Automation Rules & Key Risk Factors to Consider

What are the Main Risk Factors to Consider When Performing an AML Risk Assessment?

There are different types of money laundering risks, which require you to establish clear policies and procedures to make the AML risk assessment clear and efficient. Some financial institutions share templates on this matter, but you should generally focus on tailoring this process based on your specific risk profiles.

The common risk factors that can help you indicate money laundering when conducting risk assessments include:

- The types of customers (for example, B2C or B2B) you target based on the kind of industry you operate in.

- The size and complexity of your business, including factors like how many employees and customers you have and what jurisdictions (perhaps, high-risk) you operate in.

- The channels you use for distributing your products or services, including KYC processes for your third-party vendors/suppliers.

- The size of the transactions that you handle, as larger transactions tend to be used for evading reporting requirements.

- The results of your most recent AML audit, which should be taken into account when conducting your risk assessment.

In practice, this can be a lengthy process, especially if some of the AML processes aren’t automated through some sort of AML software. There are other complications, especially when it comes to the factor that regulations and requirements change. For example, companies can now accept crypto payments instead of standard transactions, increasing the money laundering risk. Additionally, large-scale corporations have many partners, providers, and suppliers, which should all be assessed since some might have operations in high-risk countries and be based overseas where the money laundering risk is higher.

3 Tips to Perform an AML Risk Assessment

Like with any AML process, you need to know all the processes and strategies that can be used to properly identify the risks within your business. This also means understanding the level of risk when it comes to all clients and their transactions.

Here are the key steps that are vital when performing an AML risk assessment:

1. Identify Risk Indicators

You should support your risk analysis by documenting the main risks, including how they relate to your business (the overall thought process). In general, this starts with identifying the type of clients you work with. For example, PEPs are considered to be higher-risk, as well as professional service providers, who should be verified and screened to ensure that these individuals or entities are not on any sanction lists.

For corporate clients, Business Verification is required. This includes determining beneficial ownership and who are the people that control or benefit from the company’s business activities. Multiple individuals can share beneficial ownership, and cross-checking such information with records from government agencies and other official databases is a must to ensure accuracy. Some shell companies can only exist on paper and can hide a client’s true identity. Assessing your delivery channels and whether the items are delivered remotely, in person, or through another party is important.

Additional risk indicators you should consider in your AML risk assessment:

- Clients seeking anonymity.

- Clients acting through a third party.

- Clients involved in cash-based businesses.

- Clients outside your typical customer base.

- Clients with high net worth or acting for high-net-worth individuals.

Additionally, you should identify higher-risk countries and regions. For example, if a client is registered abroad and chooses your services over those closer to them, it could be a red flag. Also, when conducting an AML risk assessment, it’s crucial to consider countries with high corruption and money laundering rates as well as screen and monitor all the transactions that your company handles, focusing on certain red flags and the types of transactions, like cross-border transactions, loan transactions, etc.

2. Assess High-Risk Activities

Based on current trends in money laundering and terrorist financing, you should examine high-risk activities during an AML risk assessment. This helps prioritize high-risk activities and follow the risk-based approach. You can evaluate each identified risk factor to determine its risk level, considering the likelihood of money laundering or other financial crime linked to each factor.

In practice, this can be done by using a risk scoring system (from low to high risk) and collecting relevant data from both internal and external sources, such as customer onboarding data, transaction records, industry reports, and other external risk indicators. You should also assess whether your AML compliance framework works effectively to address these risks.

For example, the use of crypto assets and virtual currencies, as well as trusts or financial technology services are also considered to be higher-risk activities. This is especially important when dealing with transactions or customers involving high-risk jurisdictions. For this reason, you should be aware of the money laundering warning signs and adjust your controls accordingly over time.

3. Use Automated AML Solutions

If you made it this far, you probably understand now how complex risk management is. Without any sort of automation in AML compliance, collecting, verifying and monitoring documentation is a lengthy process, not to mention keeping up with risk profile changes due to sanctions lists updates, PEP status changes, etc.

Automated solutions, like iDenfy’s AML screening and monitoring services, including our new automated customer risk management tool, help streamline your AML program, including AML risk assessment and other AML-related tasks to effectively ensure that all controls match the risk level and meet regulatory requirements. This is vital when you need to update risk assessments to reflect changes in your company’s risk profile and keep a compliant reporting and monitoring system in place.

Learn more about different ways of automating your AML risk assessment, or get started right away.