KYC is a crucial element in the fight against financial crime and money laundering. This makes identity verification the first line of defense in better assessing customer risk levels. So, even though the series of KYC checks helps banks identify them at the start of their relationship, KYC obligations continue throughout the whole customer journey.

KYC procedures are not only a security measure but also a legal requirement for banks to comply with anti-money laundering (AML) and counter-terrorist financing (CTF) laws. Regulators and governments set out these preventative measures as a way to provide a standardized framework for banks all over the world.

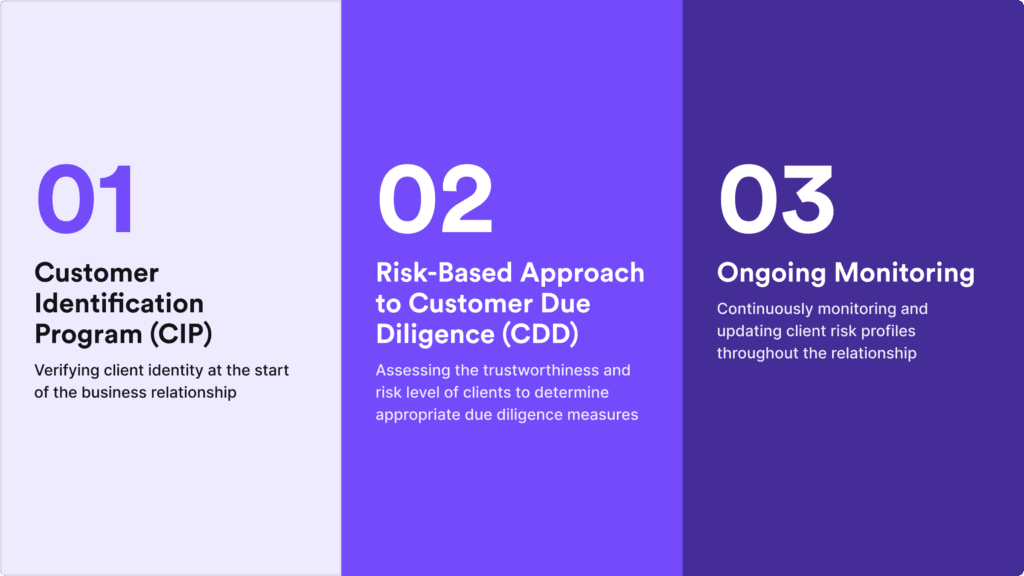

At the most basic level, a robust KYC process in banking must follow three essential elements:

- Establish the customer’s identity.

- Gain insight into their background and transactional activity, ensuring the legitimacy of their behavior.

- Continuously assess the customer’s money laundering risks through ongoing monitoring.

In this blog post, we gain a deeper understanding of identity verification and what it takes to build an effective and compliant KYC program, particularly focusing on banking industry specifics.

The Definition of the KYC Process in Banking

The KYC process in banking refers to Know Your Customer, also known as Know Your Client, a mandatory requirement for financial institutions to identify and verify a client’s identity. Banks conduct KYC checks during the account opening process and periodically over time.

If the client fails to complete the KYC process, for example, if they provide an altered document or their biometric information doesn’t match the photo on their identity document, the financial institution must refuse to open their account or start the business relationship.

KYC in banking can be applied to both individual users and businesses. For companies, the verification process is known as Know Your Business (KYB) or corporate KYC.

Verification built for fintech

From neobanks to payment platforms — see how iDenfy helps fintech companies automate KYC and stay compliant.

Explore Fintech SolutionWhy is KYC in Banking Important?

Financial institutions are legally obligated to know their customers and identify their business counterparts. Not only banks but other entities such as fintech businesses or cryptocurrency exchanges are required to follow KYC/AML laws, for example, as outlined in the Bank Secrecy Act (BSA).

If a financial institution fails to verify a customer’s identity and that customer engages in financial crimes such as money laundering or terrorist financing, the institution can face:

- Major financial losses

- Damage to its reputation

- Sanctions

For example, back in 2017, Danske Bank received a fine of $425 million for its failure to uphold proper AML measures. Similarly, in 2023, Deutsche Bank faced a penalty of $186 million for also not adequately addressing issues related to AML controls and other deficiencies. To avoid this, banks must comply with KYC requirements and provide law enforcement authorities with the necessary information to prevent and address criminal behavior.

KYC processes for financial institutions aren’t an easy task because they require the establishment and maintenance of records for each client, as well as those operating on their behalf. However, the KYC framework ensures that the customers are safe, and the bank is aware of its clientele, enabling the reporting of any suspicious activities promptly. Simply put, KYC is extremely important because it helps banks understand their customer’s financial standings before they can get involved in any purchases or investments.

Related: KYC Verification [3 Main Components & More]

What are the Three Elements of KYC Compliance for Banks?

Banks conduct the KYC process based on three main elements:

These elements complete the basics of the whole KYC compliance framework. By following three crucial elements, banks can verify the customer’s identity (1), understand the nature of their activities (2), and assess the level of risk posed by each customer (3).

We analyze each step in more detail below.

1. An Effective Customer Identification Program (CIP)

A customer identification program (CIP) is a set of compliance procedures that banks must implement to verify the identity of their clients. CIP is a smaller portion of a bigger KYC landscape and is applicable to all customers. In the case of corporate clients, it extends to beneficial owners of the business. CIP programs play a crucial role in identifying and preventing cases of money laundering, identity theft, fraud, and other financial crimes.

In banking, CIP must collect four essential pieces of information from each new customer intending to engage in a business relationship. This includes the customer’s:

- Name

- Address

- Date of birth

- Identification number (such as Social Security Number, Tax Identification Number, government-issued identification numbers found in passports, etc.)

- Additional documentation in the case of corporate clients (such as articles of incorporation, financial statements, partnership agreements, and business licenses)

Banks ensure that this collected data is verified through a combination of document and database verifications. That’s because regulators mandate that banks demonstrate their ability to obtain and verify data through well-documented CIP programs.

Related: What is the Difference Between CIP and KYC?

2. A Risk-Based Approach to Customer Due Diligence (CDD)

Customer due diligence (CDD) in banking means that financial institutions must establish a risk profile for each customer and assess the level of trustworthiness associated with them. This risk-based approach helps banks apply the appropriate level of due diligence based on particular client profiles.

CDD processes include using identity verification, transaction records, and information about the customer’s source of wealth. These checks are continuous and can occur anytime during the customer’s cycle. Standard customer due diligence consists of the collection of data linked to:

- The identity of a customer, including their company address or the names of their individual executives.

- The customer’s risk profile, for example, the likelihood of their involvement in activities that pose potential money laundering risks.

- The activities in which a customer is involved and the markets they operate in.

- Other entities with which a customer conducts business.

Related: What is the Difference Between KYC and CDD?

Different Customer Due Diligence Levels

Often, a risk-based approach requires banks to have a CDD program based on three different due diligence levels:

Level 1: Simplified Due Diligence (SDD)

It’s the least extensive level of due diligence that banks use for low-risk clients. Simplified due diligence involves a concise ID verification process in cases where the risk of money laundering or terrorist financing is considered very low. However, banks must consistently monitor such customers as well because the client’s risk level can change throughout the whole duration of the relationship.

Level 2: Standard Due Diligence

Standard due diligence is applied universally to all clients in cases where the transaction or customer doesn’t meet the criteria for SDD. This process involves gathering and verifying fundamental customer details, like their names and addresses, as well as transaction patterns, to minimize potential risks. Standard due diligence helps banks identify and report suspicious activities. This risk-based approach to KYC/AML compliance also helps law enforcement agencies track and disrupt money laundering.

Level 3: Enhanced Due Diligence

The process of enhanced due diligence (EDD) in banking is used for clients identified as having a higher risk of engaging in criminal activities such as money laundering or terrorist financing. Banks use EDD for high-risk transactions, such as those involving significant monetary value or individuals with elevated risk profiles, for example, politically exposed persons (PEPs). EDD means that banks must apply heightened scrutiny and request extra identity documentation to verify the sources of assets before approving such clients’ transactions.

Related: What is the Difference Between CDD and EDD?

3. Continuous Screening and Ongoing Monitoring

The final element of KYC in banking is continuous screening and ongoing monitoring of all clients and scrutinizing transactions. This helps detect suspicious activity that can lead banks to potential financial crime. Ongoing monitoring also enables banks to assess whether the client’s risk profile needs to be adjusted.

Typically, financial institutions have the flexibility to determine the frequency of these checks. Despite that, ongoing monitoring isn’t a one-and-done matter. Banks show their dynamic effort to maintain a robust compliance program through such continuous screening processes.

To build an effective ongoing monitoring process, banks must:

- Track changes in the frequency, location, type, and pattern of their clients’ transactions.

- Monitor significant changes in a customer’s status, such as inclusion in PEPs and sanctions lists, as well as adverse media coverage, which may necessitate a risk level adjustment.

Key KYC Regulations in Banking

KYC compliance regulations vary based on each country and jurisdiction. Despite that, there are fundamental rules and steps that we’ve discussed earlier that serve as universal guidelines worldwide.

Here are a few key examples of KYC regulations in the banking industry:

- 🇺🇸 The US. The Financial Crimes Enforcement Network (FinCEN) enforces the Financial Industry Regulation Authority’s (FINRA) Rule 2090 on KYC requirements.

- 🇬🇧 The UK. The requirements are primarily outlined in key legislative acts, including the Proceeds of Crime Act of 2002, the Electronic Identification and Trust Services for Electronic Transactions Regulations (eIDAS), and the Money Laundering Regulations of 2017.

- 🇪🇺 Europe. The EU’s Anti-Money Laundering Directives govern all KYC and AML practices. It’s worth mentioning that the UK’s regulations align with these directives as well.

Common KYC Challenges for Banks

Banks, especially small and medium enterprises or startups that want to scale faster, face many issues, including challenges regarding KYC. Neglecting identity verification and other security measures isn’t the answer. Certain red flags, including if your KYC process involves demanding manual work or if you have a high false positive rate, mean your KYC process can be improved.

Here are the key universal challenges that banks face today in terms of efficient and secure KYC verification and financing:

- Low conversion rates

- Lengthy onboarding processes

- High KYC costs

- Monolith fintech tools with low alternative finance flexibility

The delay in a bank verifying a customer’s identity means unnecessary friction to the end user. That’s why banks should aim to enhance their ability to conduct KYC checks more efficiently. On top of that, modern core banking software plays a critical role in centralising KYC workflows, customer data, and ongoing monitoring across the entire customer lifecycle.

As a way to overcome these challenges in banking, companies should prioritize automating the KYC process to minimize manual ID verification reviews and unnecessary workload. This simplifies the management of KYC-related tasks, specific rules, documents, and questionnaires into a streamlined process.

Related: How to Improve KYC Verification?

Other Fintech Branches and Their Response to Automation Capabilities

In response to the monolithic fintech capabilities, alternative financing methods like crowdfunding and private equity have emerged as viable solutions. These platforms offer a more inclusive approach to funding, allowing businesses to access capital beyond traditional banking channels.

Banks, private equity companies and fintech organizations should stay alert for the more flexible tools and incorporate them seamlessly if that fits their business model and strategic vision.

This is where innovative solutions, similar to LenderKit white-label investment software, prove instrumental. By providing a comprehensive and customizable platform, solutions like LenderKit address the challenges faced by financial institutions, streamlining the fundraising process for businesses and investors alike.

A similar option is Crassula and their White Label Banking software, which offers fintech companies the opportunity to launch their own fully personalized and fully operational banks without the need to develop or manage complex underlying technology. Here, businesses can quickly bring their unique banking solutions to life through highly customizable, low-code/no-code tools, which simplify technical challenges. Their main focus is bridging the gap between the limited IT development and time resources while shortening the sales cycles for partners, including BaaS providers and financial institutions.

The automation and efficiency offered by both AI-powered KYC and investment solutions contribute to overcoming obstacles in the fundraising journey, making it an ideal choice for those seeking to optimize their crowdfunding or private equity initiatives in the banking sector.

Using the investment solution as the core infrastructure, fintech institutions can leverage various integrations to enhance operational workflows, including user onboarding and verification.

Related: KYB vs KYC — What is the Difference? [Explanation Guide]

How Can Banks Improve the KYC Verification Process?

Internal compliance teams in banking are responsible for maintaining a compliant KYC process. This includes assessing the customer’s risk and matching their risk profile to the appropriate KYC workflow, establishing the right level of due diligence, keeping all records, and setting up procedures for ongoing monitoring.

All this considered, banks can improve their KYC verification process through automation. AI and ML algorithms help the banking sector achieve three primary KYC goals, which include:

- Improved efficiency in the KYC process. Automated document verification and selfie verification solutions can extract data from uploaded ID documents and check whether the full name and address of the user match their selfie and government-issued ID.

- Reduction in manual operations, resulting in lower costs. For further data analytics, user behavior solutions can automatically detect suspicious patterns that potentially indicate fraudulent activity.

- Achieved complete KYC/AML compliance. AI-powered AML screening tools can check if the client appears on any PEPs and sanctions lists, blacklists, or adverse media.

Interested in enhancing your KYC verification process? Talk to iDefy’s experts for custom-tailored automated identity verification solutions, easy integration options, and unlimited support.