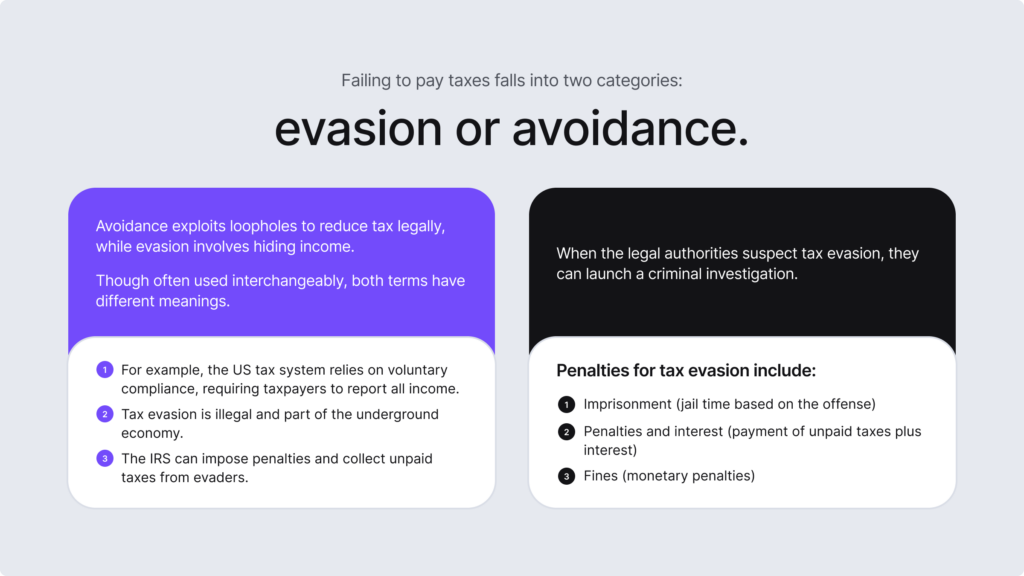

While both — tax avoidance and tax evasion — sound familiar, there are details that make these terms very different, especially when it comes to law. The tax system relies on voluntary compliance, meaning all taxpayers need to report their income. But complications like hiding income overseas or not reporting income gained from activities like garage sales help evaders reduce their tax bills. To this day, the US remains the leading country for tax evasion.

So, while there are legitimate ways to reduce tax bills by claiming special deductions, people can receive penalties for their unreported earnings, which, unfortunately, also contribute to the success of the underground economy. So, while avoidance is legal and evasion isn’t, both processes have their own complex issues, key differences, and legal factors, which we’ll review in this blog post.

What is Tax Avoidance?

Tax avoidance is the process of exploiting the tax system, either by a person or a company, to reduce tax liabilities. This is a legal practice that consists of various strategies, such as establishing an offshore company in a tax haven or taking advantage of credits and similar tax deductions. In simple words, it means that you’re paying as little as possible while still staying in line with mandatory legal requirements.

For example, if a family overpaid their taxes and received a refund after filing their return, and the next year, they claimed a deduction for home mortgage interest or credit for childcare expenses to avoid overpaying again, this means this process is tax avoidance, and it’s a lawful practice, which is acceptable. In this case, the family is making a smart financial decision to lower their tax bill legally.

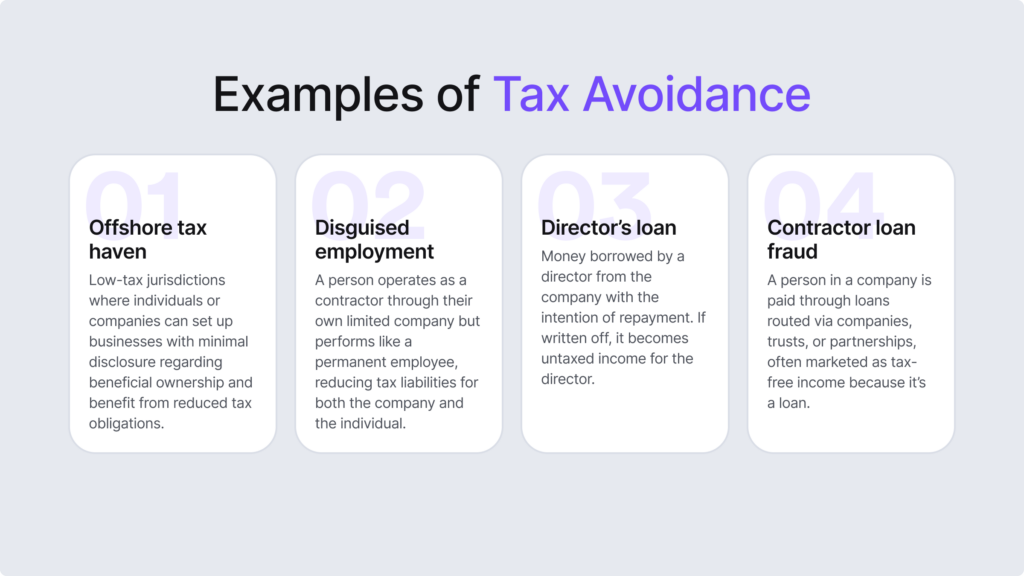

Tax Avoidance Examples

Some people exploit tax rules and their loopholes by using techniques that benefit them but go against the law’s intent. These are technicalities in the tax code that legally reduce tax liability. Keep in mind that misusing such loopholes or claiming tax benefits that you’re not eligible for can be considered a crime.

These are the common ways individuals and businesses lower their tax bills:

- Choosing a certain tax structure. For example, a limited liability corporation (LLC) which allows you to gain tax benefits and avoid double taxation.

- Using a tax-deferred account. This means investing in accounts where there isn’t a requirement to pay taxes until you withdraw the funds. For example, retirement accounts can delay taxes on earnings.

- Benefitting from credits and deductions. Reducing tax income by taking advantage of tax laws that allow you to claim eligible deductions and credits, such as paying a certain amount in mortgage interest and then deducting that amount later from your taxable income.

- Using tax-free investments. This means investing in certain types of accounts or securities that are exempt from taxes on their earnings. For example, investing in municipal bonds, earning a certain amount in interest, and not needing to pay taxes on that income.

- Disguising employment. For example, when someone works the same as a permanent, full-time employee but is hired as a contractor via their own limited company. This reduces taxes for both parties.

If taxpayers don’t pay the required amount, the Internal Revenue Service (IRS) can collect unpaid taxes and impose penalties. It’s also important to know the requirements because there are cases when people misunderstand the tax rules and overpay or fail to keep proper records which are required when proving they qualify for certain tax benefits. For example, parents in the US can receive deductions based on family size or claim child-care credits.

Related: AML Fraud — Types and Detection Measures

What is Tax Evasion?

Tax evasion is the process of intentionally failing to pay taxes or file tax returns. This is an illegal practice and a form of tax fraud. Similar to tax avoidance, both individuals and companies can be guilty of misrepresenting their income. This involves hiding information from tax authorities, falsifying tax returns, and not reporting some or all of the income, sometimes to an extent where illegal funds from selling stolen goods are collected. So, in this sense, using fraud to reduce tax liability is also tax evasion.

Hiding documents, deliberately lowering profits to avoid taxes, overstating tax credits, altering certain documents, or claiming personal expenses as business costs are all activities that count as tax evasion. That means they can lead to legal punishment. In other words, tax evasion happens when a business, its owners, advisors, staff, or individuals commit a crime to avoid paying taxes.

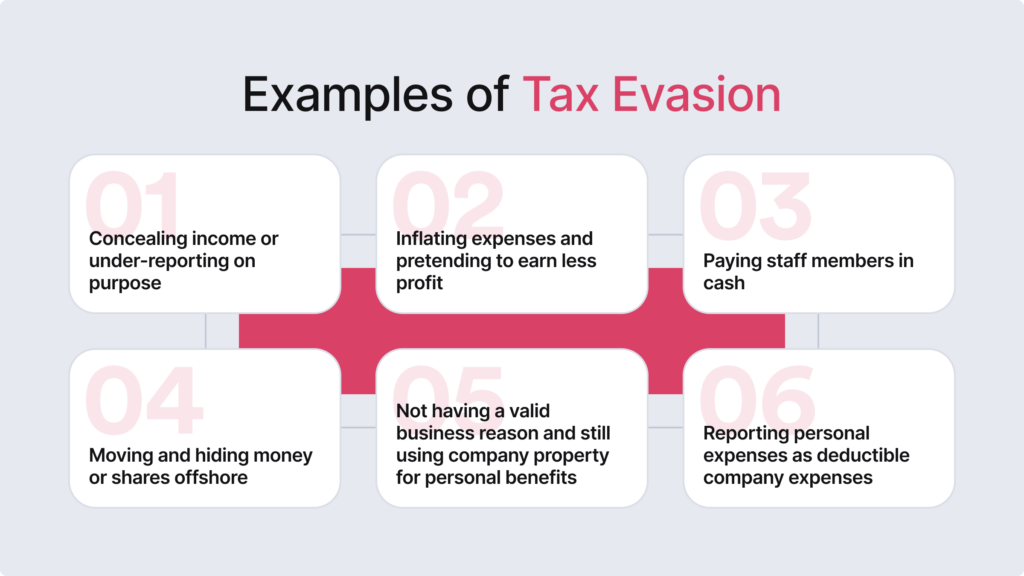

Tax Evasion Examples

Tax evasion involves different illegal methods used to reduce tax liability, often falsely showing lower income to minimize taxes owed. It is a serious crime, and penalties for tax evasion vary based on the method used and the amount of tax avoided.

Some common methods that are used to evade taxes include:

- Falsifying records. Activities like submitting fake invoices for services that weren’t actually provided or using altered and forged documents to understate expenses, lowering taxable income.

- Failing to report income. For example, hiding funds like cash payments and other assets, including shares as a way to ensure that the wealth is hidden and authorities are unaware of its existence.

- Using offshore accounts. Earning huge amounts from investments and then transferring the funds to an offshore account to hide this income, especially in countries where there are less stringent banking and Anti-Money Laundering (AML) requirements.

- Employing company property for personal use. This includes cases when a valid business reason can’t be provided. For example, taking company property, like a car, and using it for personal trips without declaring it as a taxable expense.

- Claiming fraudulent deductions. Falsely reporting expenses to reduce taxable income, often taking deductions for illegitimate expenses or those that exceed the allowable limit. This works as a technique to reduce taxable income and lower the taxes owed.

Illegally avoiding or underpaying taxes is considered to be tax evasion. In general, tax evasion is only charged if the failure to pay is intentional or, in other words, with a fraudulent intent. For example, tax avoidance is when someone hides their assets by linking them to another person. This is often achieved by reporting income under a different name, such as using a family member or a stolen/synthetic identity.

Related: AML Fraud — Types and Detection Measures

What is the Difference Between Tax Avoidance and Tax Evasion?

The key difference between both terms is that tax avoidance is legal, while tax evasion is a crime.

Here’s a more detailed explanation:

- Tax avoidance, though ethically questionable at times, involves using legal ways to reduce taxes. It is generally accepted and is considered to be fine as long as it stays within the legal system.

- Tax evasion, on the other hand, is the process of intentionally misreporting income or expenses to avoid taxes using various fraudulent techniques, such as falsifying records or claiming false deductions. While the line between the two terms is thin, evasion is illegal. Some jurisdictions treat avoidance as abuse, considering some schemes linked to hiding income as evasion.

All things considered, while tax avoidance is legal, it can still have unwanted consequences, such as adverse media or severely harming a company’s reputation, including building a bad image for the brand. Excessive abuse can strain public finances and shrink the tax base, which is used to fund public services. In general, this practice is similar to tax evasion and is treated with strict penalties.

How are Tax Avoidance and Tax Evasion Linked to Money Laundering?

Fraud, in general, is a scheme used to avoid or reduce legitimate tax payments. In this sense, all terms — tax avoidance, tax evasion, and money laundering — are linked to fraud and financial crime. Even though it’s legal, tax avoidance remains a controversial subject because it’s based on exploiting regulatory loopholes to reduce taxes, often obscuring wealth origins in ways that resemble money laundering.

Money laundering disguises illegally earned funds to make them seem legitimate, enabling criminals to infiltrate such dirty money into the general financial system and remain undetected. In the meantime, tax evasion, also an illegal act, uses deceptive methods to hide money from tax authorities, such as the mentioned offshore accounts or How to Spot Fake ID.

All three practices can harm economies and disrupt the general taxation system, further funding illicit activities. In cases like this, authorities, such as the IRS, must prove that the person or business intentionally engaged in illegal practices. That means further investigation is required, which is either a criminal tax inquiry or a civil audit.

Related: 3 Stages of Money Laundering Explained

What is Tax Planning?

Tax planning is the process of reviewing a person’s or a company’s finances to optimize them by maintaining the taxpayer in a certain tax bracket. This method helps maximize the benefits and reduce the amount of taxes needed to be paid. Various ways can be used, including manipulating the timing of income or selecting specific retirement plans.

So, simply put, tax planning is about:

- Analyzing the tax system to ensure that the lowest possible tax is paid.

- Focusing on managing payment arrangements to minimize their financial impact.

Unlike tax evasion, tax planning is legal when it’s done within the law.

How Can You Detect the Facilitation of Tax Evasion?

High-risk businesses, especially those that are regulated and must stick to AML laws, need to implement proper AML programs that are designed to detect financial crime. This is also important when establishing new business relationships. For example, banks and other financial institutions conduct thorough background checks and use Know Your Business (KYB) verification to check other companies (third-party service providers, suppliers, etc.).

This also involves checking the company’s corporate structure and verifying key details like address information or beneficial ownership data. So, using automated AML and KYB solutions helps prevent partnering with companies that facilitate tax evasion or are involved in shady business structures where the true ownership is hidden for fraudulent purposes, such as money laundering.

Apart from implementing tools, other essential steps help ensure compliance and detect tax evasion, such as:

1. Regularly Train Staff

This means knowing how tax evasion works and recognizing suspicious activity, including knowing how to report it to regulatory authorities. In other words, the right actions help staff members to prevent and combat the crime at the same time. This process is vital to safeguard the company from being exploited for fraud. All staff members should know the main AML red flags and understand their responsibilities.

Often, these include conducting due diligence and documenting various compliance procedures, including documenting the training and updating it regularly to meet changing regulatory requirements.

2. Conduct AML Risk Assessment

A robust AML risk assessment consists of various processes that assist the company in evaluating different risks based on the general AML framework. For example, this helps assess the likelihood of customers using a company’s products, services, or platform for money laundering, tax evasion, or other serious crimes like terrorism financing. Once again, for entities that pose a higher risk of tax evasion or money laundering, risk assessments are vital.

That’s because such companies often have unclear beneficial ownership structures, offshore locations, or unverified sources of funds (SOF) with complex tax planning structures. So, by conducting risk assessments, you can measure each client’s risk and reduce the chances of your company being involved in fraudulent activities. This process also identifies risks across different business areas and uncovers compliance loopholes that can be resolved by addressing challenges in real-time.

Keep in mind that non-regulated entities (from various industries) also often perform internal risk assessments voluntarily to identify high-risk clients or business partners and prevent potential threats to the company.

3. Use Automated KYB Verification

Under the Bank Secrecy Act (BSA), or a similar equivalent in the EU, the 6th Anti-Money Laundering Directive (AMLD), companies must conduct due diligence, which also includes KYB verification — authenticating another business to ensure it is not involved in criminal activities, such as tax evasion. KYB helps assess third parties and potential business partners to avoid partnering with individuals or entities involved in tax evasion.

With the previously mentioned risk assessment, companies identify different risk factors and categorize them by setting high-risk clients apart because they require stricter due diligence measures. The level of due diligence should match the associated risks. Higher risks demand additional checks and enhanced due diligence (EDD) measures. In this sense, KYB is required before the start of a new business relationship (including verifying UBOs, establishing risk scores, conducting AML screening, etc.), but doesn’t end here as it’s conducted further through ongoing monitoring practices.

If you suspect tax evasion or similar crimes, such suspicious activity should be reported.

Related: How to Choose the Best KYC Compliance Software?

iDenfy’s Approach to Detecting Tax Evasion and Ensuring Compliance

At iDenfy, we automate AML, KYB and KYC compliance processes for individual and corporate clients, providing all sorts of additional features, such as automated risk assessment, AI cross-matching, utility bill/address verification, bank verification and more — all required to assess risk factors, verify your clients and detect tax evasion and fraud while staying in line with regulatory requirements.

Get started right away or read our partners’ success stories to see our solutions in action.