An Ultimate Beneficial Owner (UBO) is an individual who owns or has control over a company. Identifying UBOs is a crucial element in Know Your Business (KYB) and Know Your Customer (KYC) processes. UBO verification aims to prevent major financial crimes like money laundering and terrorist financing.

Regulatory authorities mandate all financial institutions, such as banks, insurance companies, or investment firms, to identify and verify the UBOs associated with their business transactions. That’s why when UBOs are undisclosed, companies open new possibilities for individuals to use the company for money laundering.

Key facts to remember:

- An Ultimate Beneficial Owner (UBO) is a person or entity with ultimate ownership or control of a company or organization, regardless of the legal owner.

- The UBO legislation has been designed to provide corporations with clarity regarding the individuals or entities with whom they are conducting business, reducing the chances of doing business with shell companies and other entities that are facilitating criminal activities.

- UBO verification is crucial for countries to address financial crimes effectively and take the necessary measures to reduce the risk of illegal activities and comply with regulatory standards.

- Identifying the UBO is crucial for anti-money laundering, anti-corruption, corporate governance, and risk management efforts.

Why is Ultimate Beneficial Ownership Important?

In recent years, regulators have strengthened their efforts to combat money laundering and terrorism financing. UBO legislation helps identify fraudulent entities that resort to using offshore accounts to conceal their activities.

The key reasons why companies must accurately identify beneficial ownership include:

- Ensured security. UBO verification acts as a deterrent against criminals using shell companies to conceal their identities, thereby preventing money laundering. When identifying UBOs, companies must frequently track suspicious transactions that might lead to PO boxes, private residences of unsuspecting residents, and other fictitious addresses.

- Compliance with AML regulations. Companies must identify and verify UBOs to comply with Anti-Money Laundering (AML) regulations. The definition of a UBO varies by jurisdiction, but typically, a UBO is considered an individual holding some sort of percentage of the capital or voting rights in the company.

The EU introduced the Fifth Anti-Money Laundering Directive (5AMLD) to enhance transparency in financial transactions. As per 5AMLD, UBO checks should extend to higher-ranking officials and senior managers. Additionally, under this directive, UBO lists must be accessible to the general public, and information regarding trusts must be available to authorities.

Related: What are the EU’s Anti-Money Laundering Directives (AMLDs)? Complete History Overview

Verify businesses, not just people

Automate company verification, UBO checks, and business due diligence with iDenfy KYB.

Explore KYB SolutionWho is Considered an Ultimate Beneficial Owner?

Customers are considered to be the Ultimate Beneficial Owner if they represent the legal owners or entities that ultimately exert control over a company.

In many jurisdictions, a person is considered a UBO if they are:

- A beneficiary of at least 25% of the capital of the legal entity.

- Holding a minimum of a 25% stake in the capital of the legal entity.

- Possessing at least 25% voting rights in the general assembly.

An ultimate beneficial owner is considered to be a natural person who owns or exercises control over a company, trust, or legal entity, deriving benefits from its assets and profits. A UBO is an actual person behind a legal entity, exerting control over it, whether through direct or indirect means.

How is an Ultimate Beneficial Owner (UBO) Identified?

To identify Ultimate Beneficial Owners (UBOs), companies typically follow these steps:

- Verify the company’s legitimacy. Using reliable documents and data sources, gather and verify key information about the company, such as its name, address, and list of top management.

- Assess the ownership chain. Identify all individuals who own or control the company by cross-checking the collected information with government registries and other legitimate sources. This helps reveal the entire ownership structure and detect the main controlling individuals, including UBOs.

- Review UBO data. List all UBOs linked to the company, determine their total percentage of shares, and check if they hold indirect control over the company to confirm if they meet the UBO criteria.

- Conduct KYC verification. Perform identity verification checks on all UBOs as part of the customer due diligence (CDD) process. Use a risk-based approach to Anti-Money Laundering (AML) compliance, applying enhanced due diligence (EDD) for higher-risk individuals and simplified due diligence (SDD) for low-risk customers.

When it comes to compliance, there are challenges in ensuring UBO norms:

- Corporate entities come from multiple geographies.

- Different jurisdictions have different methods of defining UBOs.

- Financial institutions are also required to proceed with ongoing monitoring.

Criminals have their base in one country while, at the same time, they conduct business from another location. Since structures and KYB laws vary, such circumstances create legal loopholes that allow criminals to successfully launder illicit funds.

Related: The Main KYB Risk Factors You Should Know

What is the UBO Legislation?

The UBO legislation differs by region. That means the criteria for identifying and verifying a UBO are not the same everywhere. For example:

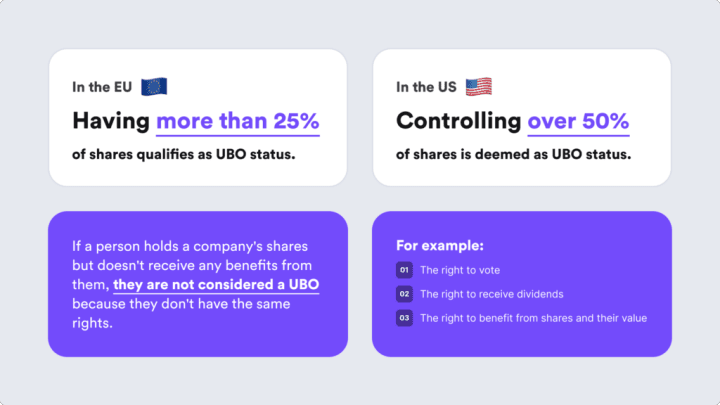

- In the United States, a UBO is someone who controls more than 50% of a company,

- In the European Union, a UBO is defined as someone who holds more than 25% of the shares.

However, most countries accept that an ultimate beneficial owner or UBO is someone who: owns more than 25% of a company’s shares (1), or has control over more than 25% of the voting rights (2).

Individuals who hold company shares but do not receive benefits like voting rights are not considered UBOs. An example is a parent holding shares on behalf of their child. In such instances, the individual is not considered a UBO because they do not have the privileges associated with:

✖️ Voting rights

✖️ Receiving dividends

✖️ Gaining advantages from the shares and their value

Additionally, UBO requirements can change over time, and UBOs may frequently move, making ownership identification challenging.

Related: Know Your Business (KYB) Service — Ultimate Compliance Guide

Is Ultimate Beneficial Owner Verification a Mandatory Process?

Any financial institution falling under the purview of AML/CTF obligations must verify the identity of the UBO for all of their business transactions.

According to the KYB framework, regulated entities must also submit the identities of their UBOs to the relevant registries. At the same time, they are required to consult these registries to identify UBOs before establishing a relationship with a customer entity.

According to the Financial Crimes Enforcement Network (FinCEN), there are exceptions to the requirement for reporting on beneficial ownership. These exemptions consist of publicly traded companies that meet specific criteria, numerous nonprofits, and specific large operating companies.

Typically, companies can check the directors of their counterparties through automated AML software and screen UBO data. This step is crucial for evaluating whether the owners or shareholders of the other company might pose potential threats. By rejecting high-risk entities, the company conducting the UBO screening avoids engaging in shady business transactions, this way safeguarding its reputation.

How Do Banks Verify UBOs?

Banks use different approaches to verify UBOs. One common approach involves requesting documentation such as government-issued identification, proof of address (PoA), and legal ownership records to validate the identity of individuals holding significant ownership stakes.

Typically, these are the actions banks take to conduct UBO verification:

1. Collect the Company’s Data

Gather comprehensive and current information, including the firm’s registration number, name, address, official status, and the names of top management employees for verification and accuracy.

2. Review Ownership Structure

Analyze the individuals or entities with a stake or interest in shares, specifying whether their ownership is direct or indirect. Seek information on shareholders, directors, and other intermediate entities that might be part of the hierarchy.

Related: How to Find Out Who Owns a Business [Guide]

3. Identify the Ultimate Beneficial Owner(s)

Detect shareholders holding substantial ownership stakes by recognizing specific percentage thresholds of shares or voting rights. Identify those individuals whose holdings meet the criteria defining Ultimate Beneficial Owners.

4. Verify UBO Data

Authenticate the provided UBO information by cross-referencing it with reliable sources, such as government databases, public records, or other trustworthy sources, to ensure its accuracy.

5. Conduct AML/KYC Checks

Ensure that all UBOs AML/KYC checks, maintaining consistency in the filing process. This involves verifying their identity through document verification, selfie verification, and proof of address. Additionally, financial institutions must cross-reference the UBOs against sanction databases and Politically Exposed Persons (PEP) lists to ensure that they aren’t associated with any financial crimes. Additionally, companies can perform adverse media checks to review negative mentions in the news automatically.

For example, sanctioned individuals pose a higher risk when it comes to illicit funds and various criminal activities. Customers who fall into international sanctions lists may also seek to conceal their identities and use shell companies. The same principle goes for PEPs. Some politicians and government officials are notorious for money laundering; therefore, the right move is to screen all of the customers, especially those who present financial crime dangers.

Related: PEPs and Sanctions Checks Explained

6. Proceed with Enhanced Due Diligence (EDD)

Move forward with additional due diligence measures for high-risk customers, such as PEPs, or when navigating through complex ownership structures that require enhanced due diligence (EDD). For companies, that means conducting more comprehensive research, enlisting third-party providers, or using automation to gather in-depth UBO information.

By identifying UBO and conducting due diligence, you can detect entities that have been previously flagged. This means that in case an established UBO poses a high-risk level, you would need to perform EDD to ensure that you’re proceeding with a secure business relationship.

Related: What is the Difference Between KYC and CDD?

What Risks Do Companies Face Regarding UBOs?

Infiltration of UBOs into a company that provides financial services can lead to serious risks, including consequences like:

- Money laundering. For example, there’s a risk if the UBOs remain undetected and their identities are concealed. They can manipulate the company to facilitate money laundering.

- Undetected financial crimes. By misusing the company’s digital platform and transactions, these hidden owners can obscure the origins of illicit funds. This makes it challenging for authorities to trace and prevent criminal activities.

For example, shell companies can serve as channels for money laundering. Usually, they store funds and engage in financial transactions without creating actual products and generating revenue (with a more favorable tax treatment). In the context of KYB compliace, shell companies allow entities to hide the true ownership structure and launder funds.

This level of exploitation not only jeopardizes the company’s integrity and compliance with regulatory standards but also exposes it to legal consequences and reputational damage. So, to fight this issue, the US Senate approved the Anti-Money Laundering Act of 2020 (AMLA) and banned anonymous shell companies, introducing new obligations — needing to disclose their Ultimate Beneficial Owner to the government.

Can RegTech Tools Help Mitigate UBO Risks?

Automated KYB software and various RegTech tools minimize UBO risks by streamlining the due diligence process. These AI-powered solutions use advanced algorithms and data analytics to efficiently verify UBO identities, cross-reference information against regulatory databases, and monitor for suspicious activities.

At iDenfy, we carry the complete AML/KYC/KYB toolkit to ensure a robust Ultimate Beneficial Owner verification process, including solutions for:

- PEPs and sanctions screening.

- Adverse media screening.

- KYC verification using document verification, selfie verification, and manual checks performed by in-house review specialists.

For more customized onboarding flows regarding both individual and business clients, book a free demo.