Money laundering is a dark world and, despite all the technological advancements and AI transaction monitoring tools, remains a prevalent issue even for the biggest financial players out there. A notorious example would be the Danske Bank scandal, where at least €200 billion in suspicious transactions were laundered through the bank’s Estonian branch between 2007 and 2015.

While money laundering, hopefully, will not ever reach the heights of Pablo Ecobar, who had an empire of illegal cash so big he had to spend $1,000 a week on bands to wrap his money, it’s still a major issue. In fact, the estimated annual volume of laundered funds is nearly 5% of the global GDP, which is approximately $800 billion.

Criminals use various tactics, such as creating shell companies or using offshore accounts to launder money, which makes it a complex task to detect them. So, there’s no doubt that Anti-Money Laundering (AML) practices are here for a reason. For financial institutions especially, striking the right balance between complying with due diligence requirements and fostering trust with customers is a delicate challenge.

Below, we dive deeper into the key examples of money laundering and explain how to detect and prevent fraudsters from getting linked to your business.

What is Money Laundering?

Money laundering is the process used by criminals to hide the true source of funds. Typically, criminals mask the illegal money through complex bank transfers or other transactions, turning it into “legitimate,” clean funds. Once the money is clean, fraudsters can securely reintroduce the laundered funds into legitimate financial systems. Criminals resort to this tactic to evade detection and taxation on their illegal earnings.

For example, criminals, especially larger groups, get the cash from theft or trafficking. Since they can’t instantly use it or invest these funds, they must integrate the illegal money into the financial system. To achieve this, fraudsters use money laundering measures and clean the money by incorporating it into legitimate channels, like banks or businesses.

Here are some common money laundering scheme examples:

- Using “smurfs” to break down large amounts into smaller transactions and deposit them.

- Blending dirty cash into the legitimate cash flow of established businesses.

- Smuggling cash to deposit in a foreign financial institution.

- Creating shell companies and channeling money through business accounts.

- Purchasing high-value goods and reselling them to legitimize the profits.

Automate your identity verification

See how iDenfy helps 1,000+ companies verify customers in seconds with AI-powered KYC.

Explore iDenfyIs Money Laundering a Serious Crime?

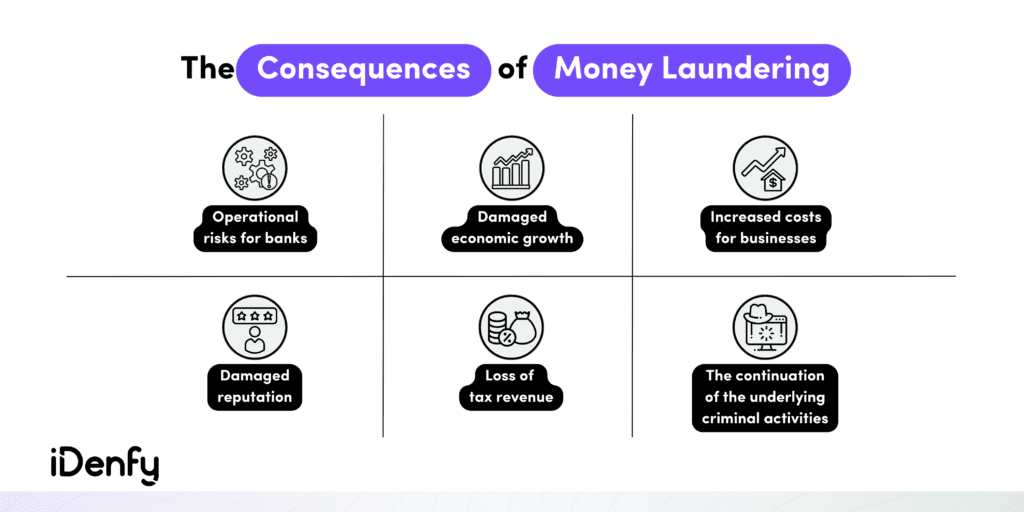

Money laundering is a severe criminal offense that has profound effects, even on the global financial system. Not to mention, money laundering serves as the main fuel that enables drug dealers, arms dealers, terrorists, and various other criminals to sustain and expand their illicit operations.

For instance, without money laundering, drug cartels would struggle to convert their illicit proceeds into legitimate assets and expand their operations, leading to less devastating consequences for society. Also, it’s important to note that money laundering is a serious crime that can be prosecuted both nationally and internationally.

When dirty money is allowed to infiltrate legal financial channels, it distorts market competition, threatens the reputation of financial institutions, and can even lead to economic instability. Some experts claim that money laundering, involving major international banks’ balance sheets, was a widespread issue during the 2008 financial crisis.

Key facts to remember:

- Money laundering is a serious criminal offense that can result in major consequences, including imprisonment.

- Today’s digital age makes it easier to launder money through cryptocurrencies or cyberattacks, which can unlawfully divert digital funds abroad.

Financial institutions and other obliged entities must implement AML measures and other policies, such as Know Your Customer (KYC) processes, to fight illicit activities.

Related: What is Anti-Money Laundering (AML)?

What are the Three Stages of Money Laundering?

There are three stages in money laundering – placement, layering, and integration. They represent a systematic approach to obscuring the illegal origins of funds. Each stage serves a distinct purpose:

1. Placement

In this initial stage, criminals introduce their illicit funds into the legitimate financial system. It’s often the riskiest phase because the goal is to distance the illegal money from its source. Placement means starting with cash and depositing it into a bank. However, making a large deposit all at once tends to trigger AML alerts. To avoid this, criminals use placement strategies, such as using a foreign currency exchange to change some of that cash into a different currency.

2. Layering

The purpose of the second stage, layering, is to add additional transactions to obscure the illicit money’s real source without leaving a paper trail. This process involves multiple placements and extractions so that criminals can generate a seemingly legitimate cover for their funds. Layering is crucial for evading AML checks and often involves the same placement techniques, such as investments in fine art or real estate. That’s why banks must verify customer identities and have a proper Customer Identification Program (CIP) to spot these activities.

3. Integration

In the last stage, the “cleaned” money returns to the criminal or the company and appears completely legitimate. It can then be invested or withdrawn and used by criminals for lawful transactions. Due to the prior layering, it becomes challenging to distinguish whether the wealth is illicit or not. Assets obtained during the layering stage, such as art, real estate, cars, etc., can now be used or sold. Moreover, tracking the criminals can be challenging, as they often employ tactics like sending sham invoices to shell companies for payment, even when no actual goods or services are involved.

Related: 3 Stages of Money Laundering Explained

What are the Examples of Money Laundering Offenses?

Before the implementation of the Proceeds of Crime Act 2002 (POCA), regulations concerning the proceeds of crime were under the authority of the Criminal Justice Act 1988 and the Drug Trafficking Act 1994. However, with the introduction of this legislation, all money laundering offenses committed on or after March 24, 2003, are now subject to the rules outlined in the POCA.

POCA is a UK law created to address and prevent the gains from criminal activities. It’s a crucial component of broader efforts aimed at combating criminal behavior and dismantling organized crime networks effectively.

The Proceeds of Crime Act 2002 consists of three categories that illustrate examples of money laundering offenses:

1. Concealing

Concealing is an act where an individual, with knowledge or suspicion of money laundering, tries to hide its occurrence. If a person makes efforts to mask, conceal, transfer, or withdraw illicit funds, they can face charges related to this offense. For example, an attempt to conceal laundered funds could involve depositing the money obtained through illegal activities into a gambling account or converting it by placing bets in a gambling establishment and later cashing in the winnings.

2. Arranging

In the context of money laundering, the arranging offense involves an individual facilitating money laundering activities on behalf of others. This facilitation can encompass various actions that benefit someone else in committing a money laundering crime, such as opening a bank account to deposit illegally obtained funds. For instance, arranging could be when a person working in a financial institution, such as an accountant, helps a criminal to launder their illicit money.

3. Acquisition, Use and Possession

The offense of acquisition, use, and possession is when individuals seek to profit from money laundering by acquiring, using, or having control over illegally gained assets. In other words, it happens whenever a person personally gains, utilizes, or possesses illegally obtained assets. An example of this would be making purchases with funds obtained through unlawful means.

Related: AML Fraud: Types and Detection Measures

What are the Common Examples of Money Laundering?

Money laundering has various methods and involves activities like trading commodities, investing in assets, or engaging in gambling and counterfeiting.

Understanding the most common money laundering examples is the first step toward building defenses against them. The examples of money laundering activities covered below are not theoretical, unfortunately. They are the exact schemes that regulators, law enforcement, and compliance teams encounter regularly across banking, real estate, gambling, and other strictly overviewed sector. Each one exploits a different vulnerability in the financial system, which is why no single control is sufficient on its own.

These examples of money laundering activities span industries and geographies, reflecting just how adaptable financial crime has become in the digital era.

Here are some common money laundering schemes, which include:

Structuring (Smurfing)

Also known as smurfing, structuring involves breaking down large cash sums into smaller portions on purpose and depositing them into numerous accounts. This technique makes it challenging to detect illegal funds. In general, structuring aims to bypass financial regulations necessitating reporting large transactions, usually surpassing a specified threshold, such as $10,000.

However, while criminals often use money orders and cashier’s checks for structuring, multiple deposits of these forms in a short time can raise suspicion at financial institutions, potentially triggering money-laundering investigations. Since financial institutions are vigilant for suspicious activities, suspected structuring can lead to heightened scrutiny of individual accounts.

Related: Smurfing in Money Laundering Explained

Real Estate Laundering

Real estate laundering is also a very common form of money laundering in which criminals use their illegal earnings in the property market, concealing the origin of their wealth. Often, organized crime groups launder money into real estate, effectively transforming illegal cash into a valuable asset that can be sold for legitimate money. This approach involves using ill-gotten funds to purchase, sell, or lease real estate properties, giving the illusion of lawful financial activities.

It’s worth mentioning that real estate laundering has been abused in the past because of the absence of proper AML regulations and oversight regarding cash transactions in the real estate market. For example, shell companies and transactions facilitated by third-party collaborators add an additional layer of false legitimacy to such laundering tactics. Despite that, in response to this issue, many countries have started to implement AML regulations in real estate to combat this rising issue.

Shell Companies and Trusts

Shell companies and trusts are sophisticated tools frequently used in money laundering schemes, providing a complex disguise for the laundered money. These entities are also known as ghost companies, which don’t have legitimate active business operations or substantial assets. Fraudsters often create these entities, often in offshore locations, to conceal the true source of their wealth.

Shell companies, typically lacking genuine business operations, act as a veil for the money’s trail. When multiple shell companies are interlinked, the financial web’s complexity increases, making it more challenging to trace the money to its origin. Trusts, similarly, establish a degree of separation between the beneficiary and the illicit funds. Operating as legal arrangements where a trustee holds assets on behalf of a beneficiary, trusts provide anonymity, particularly when established in jurisdictions with poor regulatory oversight.

Casino and Gambling Laundering

Casinos and gambling sites offer an attractive opportunity for money laundering, using the lively atmosphere to hide illicit funds. Criminals capitalize on the fluid nature and excitement of gambling to transform their ill-gotten gains into what appears as legitimate earnings. Today, money laundering can occur in both physical and online casinos. Typically, a fraudster uses illegitimate funds to purchase casino chips or credits, experiences both losses and wins, and then cashes out. This process effectively “cleanses” the money through the casino, establishing a seemingly legitimate transaction history.

Another favored method involves betting significant sums on low-risk games like roulette or blackjack. These savvy gamblers might intentionally lose some of their bets to make it seem like genuine gambling. They then exchange their chips for clean cash, eliminating any suspicion surrounding the origin of the money. However, engaging in such practices under different aliases or user names during transactions and visiting various locations to exchange chips can raise suspicions and serve as red flags for potential money laundering.

Trade-Based Laundering

Trade-based money laundering (TBL) is a money laundering tactic where criminals manipulate the value, quantity, or nature of traded goods to move money across borders, presenting it as legitimate business transactions. Criminals favor this approach for laundering illicit funds because it creates a convincing paper trail that’s challenging to detect. In the meantime, companies use TBL by falsifying the costs and quantities of their imports and exports, inflating their profits beyond reality.

For example, using this illicit tactic, criminals forge invoices and sales documents, which create an appearance of legitimacy to their actions. This strategy also includes practices like inflating or deflating goods’ prices, misrepresenting product quality, and forging customs declarations. Fraudsters often combine this method with other money-laundering techniques, further complicating the task of tracing the money’s source. They use shell companies, shelf companies, hidden intermediaries, and offshore hubs to add layers of complexity and distance themselves from illegal activities.

Related: Biggest Money Laundering Cases

What Legal Compliance Measures Help Prevent Money Laundering?

The Bank Secrecy Act of 1970 (BSA), also known as the Currency and Foreign Transactions Reporting Act, was established to help financial institutions detect money laundering activities by imposing reporting obligations. The BSA is also sometimes referred to as the anti-money laundering law.

This compliance measure mandates that financial institutions undertake specific measures, such as submitting currency transaction reports to regulatory authorities. For instance, when their clients engage in suspicious transactions exceeding $10,000, banks are obligated to file a suspicious activity report (SAR).

Another prevalent organization when it comes to AML compliance is the Financial Action Task Force (FATF). This international organization collaborates with over 200 member countries and organizations, such as the World Bank. FATF’s recommendations offer a standard framework to combat money laundering, but each jurisdiction should adapt these standards to its specific context based on national and international laws.

How Can Financial Institutions and Businesses Detect Money Laundering?

The evolving regulatory environment is driving a new trend, enabling financial institutions to share information and engage in collaborative investigations to combat money laundering. Existing legal frameworks support this change. For example, Article 6 of the UK GDPR creates a basis for data sharing driven by legitimate interests. Additionally, introducing the 6th AMLD in the EU has opened doors for information sharing. By the end of 2023, the European Parliament and the Council of the EU have agreed to establish an Anti-Money Laundering Authority (AMLA).

Other key steps that financial institutions and companies can take to identify money laundering include:

- Verifying the source of funds (SOF).

- Implementing Know Your Customer (KYC) protocols.

- Collecting and screening information on potential and established mule networks.

- Monitoring transactions that appear suspicious or are unusually high in volume.

In its report “Partnering in the fight against financial crime,” the FATF recommended that public and private sector financial institutions collaborate in sharing information. Such sharing enhances public-private partnerships, strengthening the bond between financial institutions and authorities. This collaboration can enhance the effectiveness of financial sanctions and lighten regulatory burdens. So, while more regulatory changes are coming, several information sharing tools, including Salv Bridge, are already benefiting financial institutions across the EU and the UK.

Companies should also learn to identify red flags that suggest the need for more extensive due diligence. For example:

- Complex business structures or difficulty in determining the true business owner.

- Purchasing high-value items, such as art, jewelry, and other items.

- Unusual transaction patterns, like the mentioned high-volume transactions or selling assets significantly below market value.

- A high volume of cash transactions, including cash salary payments to employees.

Various examples of money laundering illustrate why regulators take a risk-based approach rather than applying uniform rules across all transactions and customers. What counts as suspicious in one context (for instance, a large cash deposit at a casino) can be entirely routine in another. Banks have stricter requirements and typically larger customer and transaction volumes. Today, agentic AI and AI-powered AML software solutions are used to handle the screening and monitoring. However, regulated entities need to keep their eyes open in terms of setting up rules and including everyone in their monitoring systems. Otherwise, they are risking facilitating money laundering, even if it’s not a known fact to them.

That’s precisely why compliance teams must be familiar with the full spectrum of examples of money laundering activities, from the most obvious smurfing schemes to sophisticated trade-based manipulation. A useful anti money laundering example of this risk-based thinking in action is transaction monitoring calibrated to a customer’s profile: a fintech platform serving retail customers would flag a sudden $80,000 wire transfer to an offshore account, while a private bank serving high-net-worth clients (for example, in industries like aviation) would apply different thresholds for the same amount. The common thread across all money laundering examples is that the red flags only become visible when compliance teams know what they’re looking for.

Preventing Money Laundering Through Automated AML Tools

Money laundering prevention can be a challenging task for various businesses, including crypto players, fintechs, e-commerce companies, legal service providers, etc. Compliance officers play a pivotal role in ensuring AML compliance within companies. Yet, handling tasks like creating and executing the AML compliance program, reporting suspicious transactions, and staying current with evolving compliance regulations without automated software can be nearly impossible, especially with the high number of customers and their transactions.

Thankfully, third-party AI-powered KYC/AML software providers can simplify the process.

At iDenfy, we help businesses ensure KYC compliance by providing biometric verification with built-in liveness detection, document verification services, and manual real-time identity verification checks with our dedicated in-house KYC team. To protect businesses from money laundering and assist them in ensuring ongoing due diligence, we offer automated AML screening and ongoing monitoring checks, including global watchlist checks, PEP and sanctions screening, as well as adverse media checks.

Get started today, and don’t forget to check out our customer success stories.