What can an effective merchant onboarding do for your business? Well, for starters, it can be used as a tool to reduce fraud and improve user experience. For this reason, to have a secure and simple payment processing system, you also need to optimize your merchant onboarding, which is crucial for your scaling and a channel to attract more merchants and more transactions.

If you’re a payment service provider (PSP), onboarding new merchants means carefully designing and executing their onboarding process according to specific needs. However, the key challenge is finding the right balance between a simple, straightforward onboarding process and a more thorough approach that prevents fraudulent activities. This balance is crucial because fraudulent merchants can lead to problems like chargebacks and revenue loss.

We explore how you can efficiently onboard legitimate merchants while preventing fraud from impacting your business, as well as other nuances that you need to know about merchant onboarding.

What is Merchant Onboarding?

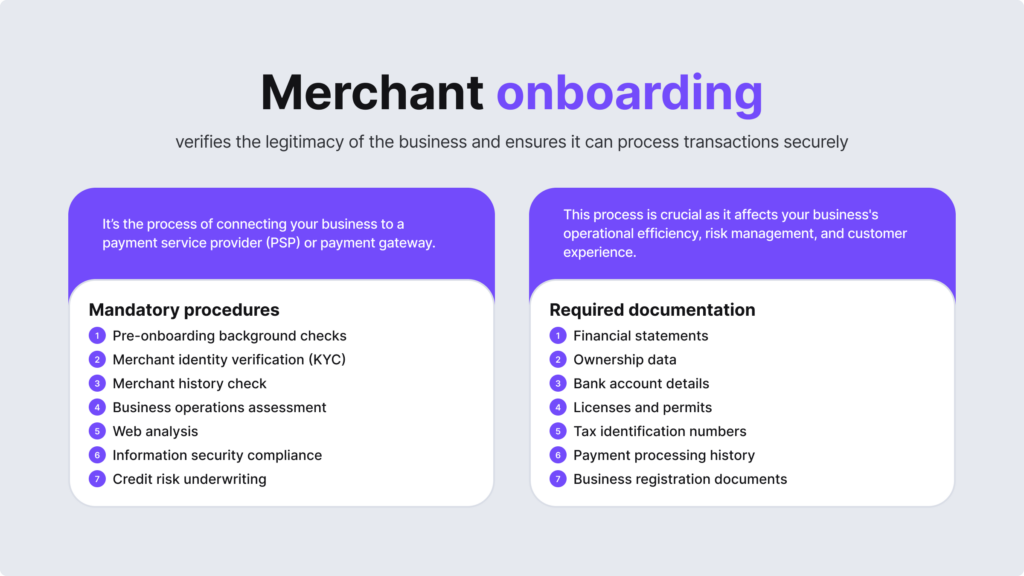

Merchant onboarding is a security process when payment processors and payment service providers (PSPs) sign up new customers (merchants) to handle their payments. This works as a fraud prevention measure because, if not done properly, non-compliant merchant onboarding can result in transaction failures, fines, and improper risk management.

Typically, this process involves verifying client identities, submitting documents, conducting background checks, performing financial assessments, and implementing other compliance measures, depending on the business and industry. A well-managed merchant onboarding needs to be swift and simple, which is one of the top priorities for businesses to both stay compliant and attract new customers in this highly competitive market.

The merchant onboarding process aims to ensure that the business is legitimate and capable of handling transactions securely and efficiently. That’s why it affects user experience and operational efficiency — both factors that need to be balanced out.

Related: KYC Onboarding — How to Achieve Complete Compliance?

Automate your KYC process

iDenfy verifies customers from 200+ countries in seconds. AI-powered, compliant, and trusted by 1,000+ companies.

Explore KYC SolutionThe Key Figures in the Merchant Onboarding Process

There are several important figures that complete the merchant onboarding process. To balance out a smooth end-user experience, compliance and security, you should know all of the key players.

These typically include:

- Payment service providers (PSPs). These are the businesses that offer payment processing services to other companies, including transaction processing, authorization, and settlement, and at the same time, ensure compliance with regulatory requirements.

- Merchants. These are the companies that accept payments from users. Merchants partner with PSPs to facilitate transactions online, but their services also include in-person and mobile payments.

- Acquiring banks. These are financial institutions (also known as merchant acquirers) that partner with PSPs to process transactions for businesses and handle the underwriting of merchant accounts.

- Payment gateways. This is the front-end technology that transfers the transaction data to another business system. For example, it can be a company’s app or a point-of-sale (POS) system. Payment gateways read card data and transfer customer information to the acquiring bank for processing.

- Issuing banks. They provide users with payment cards that are branded by card companies, such as contactless devices, prepaid cards, and debit/credit cards. They “issue” the cards and, as a result, have this title.

- Card companies. These are the organizations, such as Mastercard, Visa or Amex, that set the standards for card transactions and enable the settlement of transactions between the acquiring bank and the issuing bank.

Therefore, every participant in the merchant onboarding process plays a crucial role. PSPs collect detailed information about potential new merchants to perform a thorough risk assessment. For high-risk merchants, extra measures are applied to prevent non-compliance fines and to avoid losing new merchants.

The Main Documentation for Merchant Onboarding

Collecting and verifying documents is an important part of the merchant onboarding process, which means that companies should review the following documentation:

- Registration documents (certificates of incorporation, copies of articles of association, or other documents showing the company’s legal status).

- Tax identification numbers (such as the Employer Identification Number (EIN)).

- Licenses and permits (business licenses or certifications).

- Ownership details (a full breakdown of the company’s structure and key shareholders).

- Proof of identity (passports, driver’s licenses, ID cards — and that applies to all people associated with the company).

- Proof of address (bank statements, utility bills, tax bills, and other PoA documents that are required to verify their address).

- Financial statements (cash flow statements, income statements, and balance sheets).

- Payment history (chargeback rates and transaction volumes).

- Online presence (business website, URLs and descriptions, app details, social media profiles, terms and conditions, etc.).

These documents are a part of the risk management process, as companies need to identify certain risks during merchant onboarding. They can be categorized into a few types: general risk signals, beneficial ownership risk signals, financial history risk signals, and online presence risk signals. So, overall, collecting documents and verifying this information should help you assess the risk of working with another merchant.

What is KYC, or Know Your Customer?

Know Your Customer (KYC) is an identity verification process that is required for companies like payment providers, e-commerce platforms, financial institutions, crypto firms, and other entities, to ensure the customer is legitimate as a way to reduce fraud, including money laundering and unauthorized payments.

KYC is also a part of the merchant onboarding process. This requires:

- Performing KYC verification before approving a new merchant (for example, for payment service providers and acquiring banks)

- Evaluating the business’s risk level and deciding whether to accept or reject the merchant application (based on collected KYC data)

Related: KYC Verification [3 Main Components & More]

How Does Merchant KYC Verification Work?

Merchant KYC verification, or the merchant verification process, is the actions that a company takes to confirm a merchant’s identity while ensuring they’re legitimate and that can start accepting payments. This process consists of various KYC measures. The information required for KYC verification varies by jurisdiction, but typically includes the company name, tax identification number, and business address, which we mentioned when talking about the required documentation.

The merchant verification process is often called the Know Your Business (KYB) process, established after KYC, and focuses on ensuring the verifying company knows a legal entity’s representatives and identifies the ultimate beneficial owners (UBOs) — the individuals who directly benefit from the company’s profits. Another term for this process, especially when talking about online marketplaces and the e-commerce industry, is Know Your Merchant (KYM), which aims to make merchant risk management more efficient.

In general, merchant verification helps prevent fraud and protect both the payment processor and customers. This ensures the business is real and is currently operational, genuine, and not involved in any sort of criminal activities.

What is Merchant Risk Management?

Not only iGaming but also forex platforms, online brokers, and other high-risk entities attract more money launderers and are prone to financial crime due to a large volume of transactions, among other risk factors, which are crucial when assessing various risk factors during the merchant risk management process. It helps to determine the level of scrutiny when onboarding merchants because not all merchants are the same, and the required level of due diligence differs.

In general, there are three levels of due diligence checks: simplified, standard, and enhanced. The level of scrutiny applied depends on the risk associated with the customer and their transactions. Despite the different risks, all merchants should be verified and assessed during onboarding.

This can be completed when asking standard questions to follow a risk-based approach. For example:

- What channels will the merchant use?

- What are the transaction amounts?

- What is the transaction volume of the merchant’s network?

- What industries does the merchant operate in?

- In which countries does the merchant work?

Related: What is the Difference Between CDD and EDD?

What Steps Complete the Merchant Onboarding Process?

Here’s a structured breakdown of what kind of steps you should take to successfully onboard a merchant:

1. Prescreening

In this first stage, companies should collect the required documents from the merchant to verify the company’s data in order to check that it’s genuine and running in a compliant manner based on industry standards. This is the part where you can eliminate scammers and fraudsters, as well as non-existent businesses. When researching and assessing the company, you can also find the best PSP or payment gateway that is suitable for your business model.

2. Merchant Verification

Here, the merchant provides additional background information, which often makes this step more time-consuming, especially if no KYC/KYB automation solution is used. By verifying the details about the business, its ownership structure, or expected transaction volumes, you can decide if further due diligence is required. Data can be cross-checked against government databases to ensure that the collected information matches reputable records. This step often helps identify suspicious accounts, particularly after reviewing documentation like proof of identity, address, bank details, and business setup information.

3. Ultimate Beneficial Owner (UBO) Verification

At this stage, PSPs should verify the merchant’s UBOs to comply with AML requirements. UBO verification ensures that the company’s ownership structure is clear and all identities are revealed. This can be achieved by assessing the ownership chain by cross-checking with government registries to reveal the entire ownership structure. More importantly, UBO verification mandates KYC checks on all UBOs, applying EDD measures for high-risk individuals and SDD for low-risk ones.

4. Risk Assessment

When performing due diligence, you need to evaluate the internal risks linked to your business based on different risk signals, such as business type, transaction volume, and chargeback history. This is an AML compliance requirement for regulated entities. Additionally, when it comes to potential clients, after performing EDD on merchants, PSPs should also conduct risk assessments based on the results. This means categorizing entities and their risk levels (from low to high). These risk assessments help guide companies in deciding the necessary steps before onboarding a merchant.

5. Merchant Credit History Check

PSPs need to ensure that merchants are operating legally. This step is designed to help evaluate another company for a merchant account. This means the business reviews the company’s complete financial track record, including the personal credit history of all linked individuals. This also helps detect AML red flags and sometimes, the company is asked to provide extra documents to verify their credit history. Sometimes, there can be signs of fraud or high chargeback rates, which can negatively impact the business and signal non-compliance with regulations.

6. Operational Model and Web Analysis

If due diligence uncovers any risk signals, an operational model analysis is typically conducted for high-risk merchants. This process helps ensure security and prevent fraud by analyzing the businesses’ internal operations to prevent money laundering activities. This can be done through adverse media screening, which helps automatically find links to crime and other offenses. On top of that, web analysis is crucial to check if the company’s uploaded content online is legitimate, secure, and matches regulatory compliance standards.

7. Ongoing Monitoring

This is the last step. However, it doesn’t stop here. PSPs and merchant acquirers need to continue their risk management after the merchant onboarding process. Monitoring means continuously reviewing compliance procedures, updating them to meet the newest regulatory standards, as well as optimizing payment processing systems to maintain maximum efficiency.

To ensure effective monitoring practices, payment service providers use different fraud prevention measures, such as transaction monitoring that help automatically screen and monitor, set transaction limits and see suspicious activity in real-time. Monitoring is crucial because it can be done efficiently through automation, allowing businesses to quickly detect changes such as updates to sanctions lists, unusual cross-border transactions, spikes in activity, or modifications to a merchant’s website. This ongoing monitoring is essential for maintaining accurate and up-to-date risk profiles.

Related: AML Fraud — Types and Detection Measures

What Challenges Do Companies Face in Merchant Onboarding?

Financial institutions, including payment service providers, need to conduct internal risk assessments to determine their company’s and related clients’ risks. However, some companies aim to onboard new merchants quickly, but those classified as higher-risk need to undergo additional checks and stricter risk management procedures. That’s why the biggest challenge in the merchant onboarding process remains balancing a smooth experience with a proper risk assessment process. Consider implementing automated call recording software to get further insights by evaluating merchants’ qualifications, existing experience, future business projections, etc.

For example, iGaming platforms are known to have many risks, such as bonus abuse, a higher chargeback rate, and a higher risk of money laundering, so they are deemed as “high-risk.” As a result, PSPs conduct a more rigorous review when onboarding merchants from high-risk industries. This becomes a huge hassle with manual tasks when compliance officers need to do repetitive tasks that often introduce human error, increasing costs and slowing down the overall onboarding process.

However, automated KYC/KYB solutions, including risk assessment tools, can improve this process, optimizing various compliance tasks and improving accuracy rates, which are the top priorities for robust merchant onboarding.

Related: What is a Transaction Dispute? [Challenges for Merchants]

Use Cases of Automation in Merchant Onboarding

Higher-risk markets that handle large volumes of transactions need some sort of automated solution to ensure an effective fraud prevention strategy, including swift yet fully secure and compliant merchant onboarding.

Collecting, verifying and assessing documentation in different languages or formats is a hassle for compliance teams, and, at the same time, ensuring ongoing due diligence can be a challenging task when risk evolves and changes after the initial onboarding stage.

To ensure a fraud-free ecosystem, iDenfy’s team has developed a multi-functional KYC/KYB and AML compliance hub for:

- Automated risk management.

- Business client onboarding (KYB).

- Individual customer verification (KYC).

- Streamlined AML compliance (PEPs and sanctions, watchlists/adverse media).

- Other fraud prevention tools, like IP scoring or phone verification.

Let’s chat so you can get a proper hands-on experience and learn how to improve your merchant onboarding experience.